The Dawn of AI Warfare: A Conversation with Katrina Manson

May 21, 2026 • 11:30 am – 12:30 pm EDT

Photo: Adobe Stock

A group of senior members of the Trump administration, led by Treasury Secretary Steven Mnuchin, met with Chinese counterparts recently to discuss ways to defuse the current tension over the bilateral trade imbalance. Energy—along with agriculture—was identified as one of the areas for greater U.S. exports to China that could defuse the tension by helping to address the administration’s concern over the nation’s bilateral trade deficit with China.

The administration seeks to reduce the total bilateral deficit with China by at least $200 billion. Last year, the United States ran a $375 billion deficit in goods trade with China, up from $295 billion in 2011. (Meanwhile, the United States ran a trade surplus of $38.5 billion in services in 2017, up from $16.5 billion in 2011.)

Bilateral trade relations have become strained in recent months. In March, the administration announced a decision to levy tariffs on Chinese imports worth as much as $50 billion over the issue of forced technology transfer. Following China’s pledge to retaliate in kind, the administration announced additional tariffs worth $100 billion. These announcements followed the imposition earlier this year of solar panel tariffs and steel and aluminum tariffs that affect Chinese imports, albeit at varying degrees.

While the United States and China have multiple disputes across various areas of trade and investment, energy commodity trade is one of the bright spots and, as Secretary Mnuchin outlined, may be the one that helps quell the conflict. U.S. hydrocarbon exports continue to rise, while China’s strong appetite for them is showing no signs of letting up.

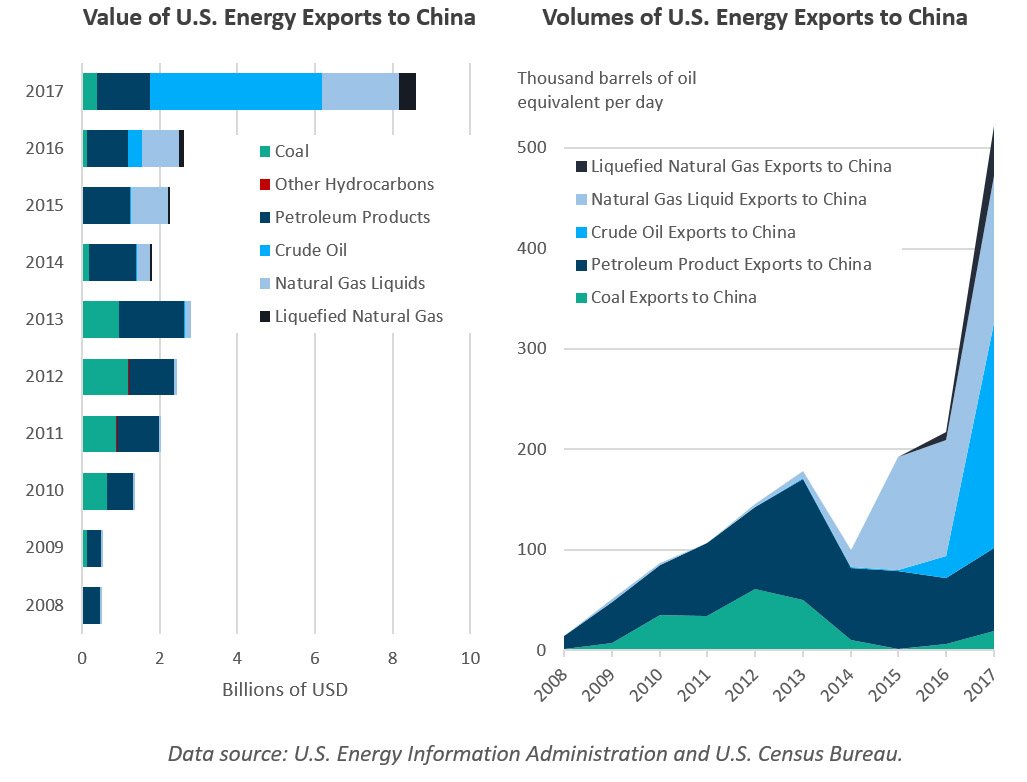

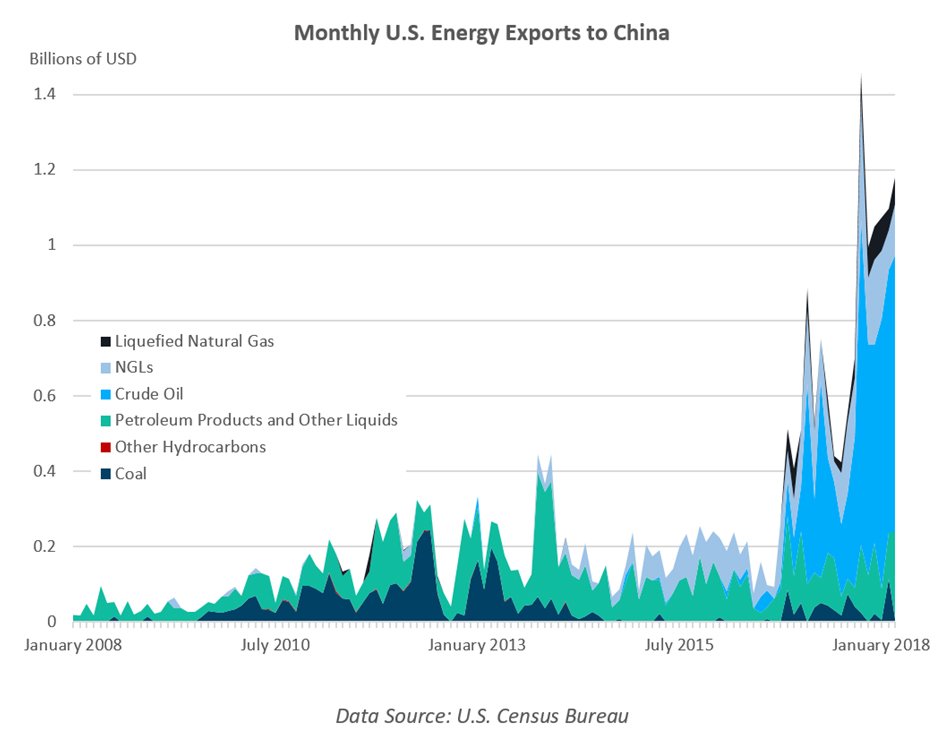

According to the latest U.S. Census Bureau data, U.S. energy exports to China amounted to $8.6 billion in 2017, a massive increase from the $2.6 billion worth of energy commodities sold in 2016. Secretary Mnuchin has stated that the United States could “easily get about $40 or $50 billion of energy” exports to China. Will energy trade help alleviate the bilateral trade imbalance? Will this affect the overall U.S. trade deficit? And who gains from the increased flows of U.S. energy to China?

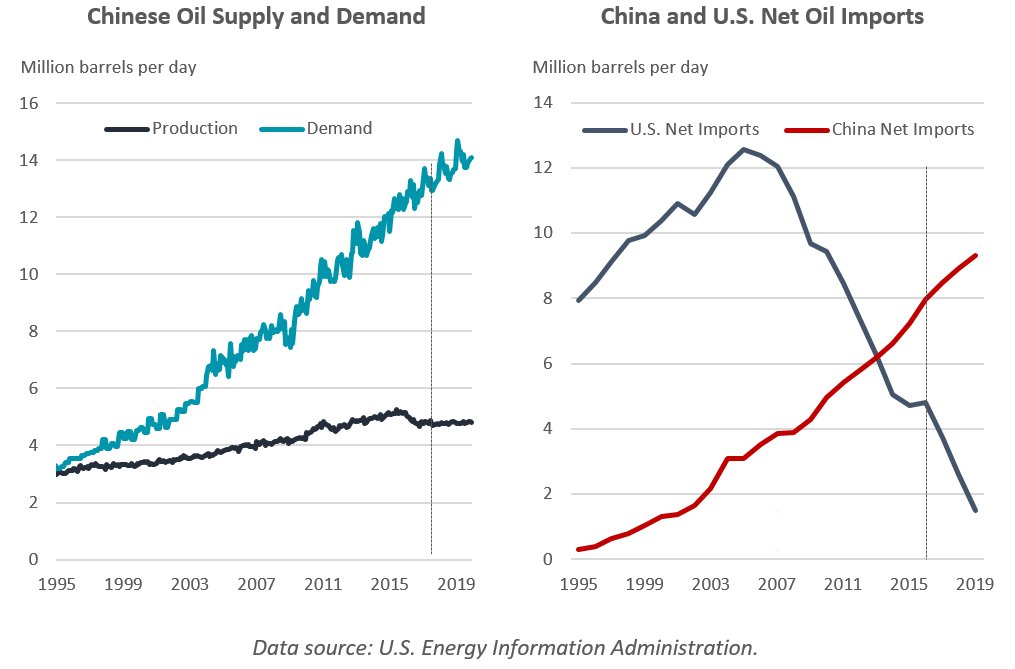

The short answer as to whether energy trade with China will alleviate the bilateral trade imbalance is a “yes,” as there is room for China-bound U.S. energy exports to grow for several reasons. First, despite China entering a “new normal,” characterized by slower economic growth and a slowdown of primary energy demand growth, oil demand has continued to increase. At the same time, domestic production has faltered creating a net oil import problem for the country. Chinese import dependence is also growing for natural gas, as the government has pledged to reduce coal dependence. Last year saw a 27 percent jump in China’s gas imports, including a 46 percent increase in liquified natural gas (LNG) import volumes year-on-year.

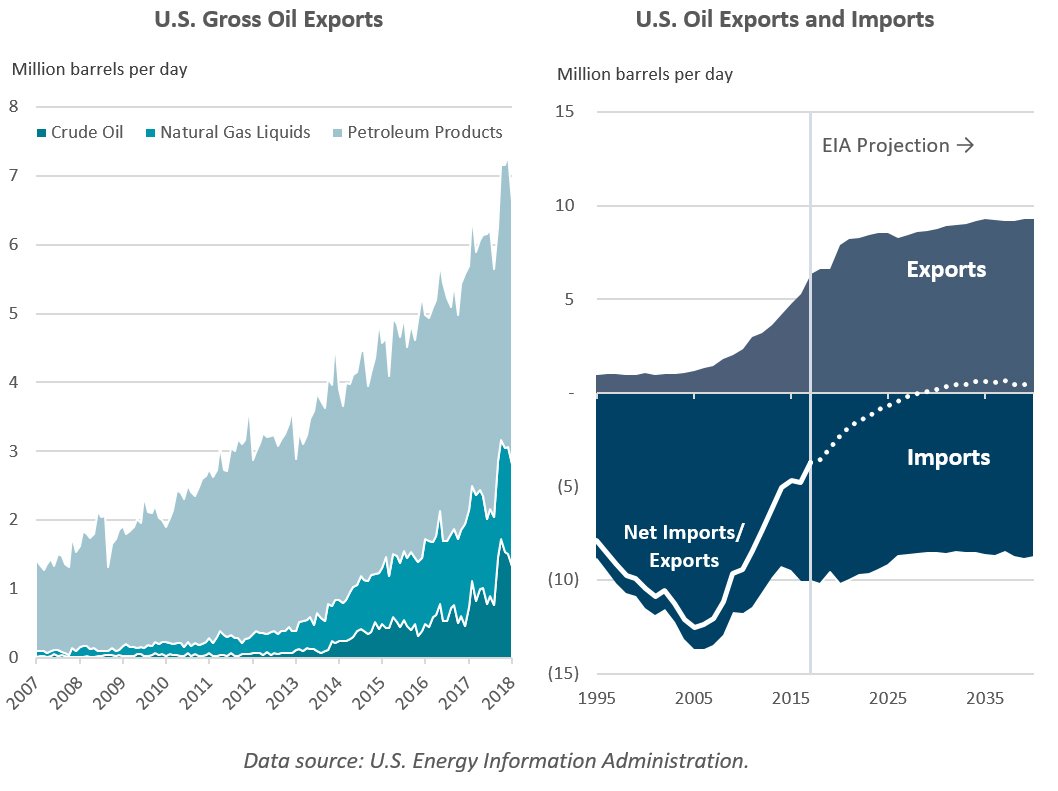

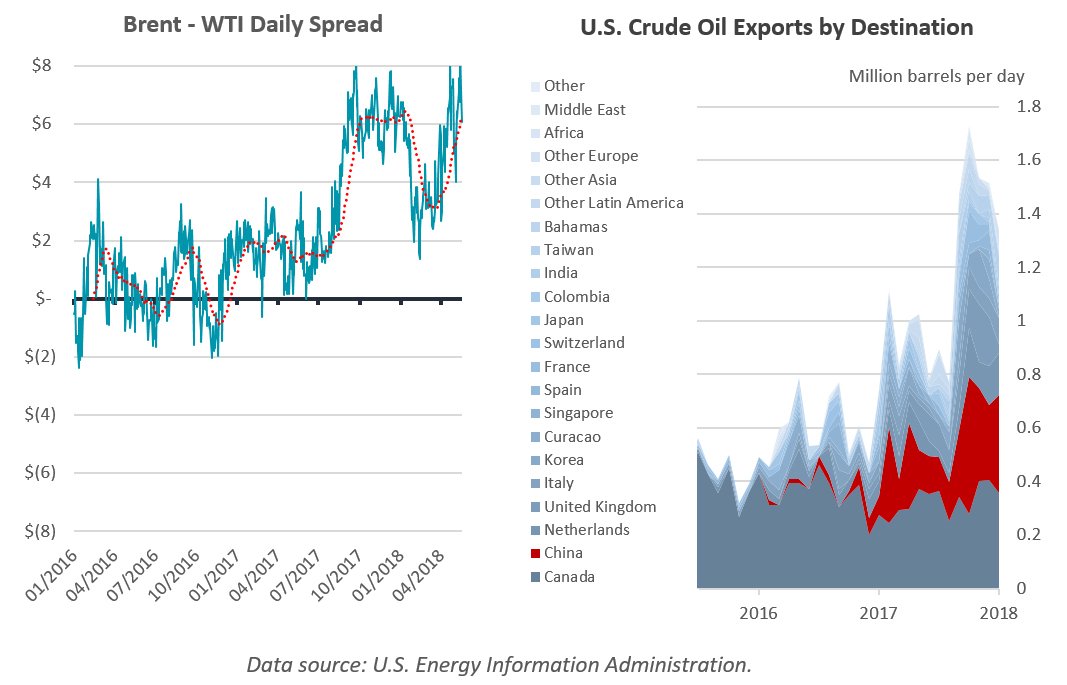

Second, the U.S. oil and gas renaissance has caused a dramatic fall in U.S. energy import dependence. The United States will become a net exporter of natural gas this year and a net exporter of oil by the end of the next decade. While the United States has yet to become a net exporter of oil, gross exports of crude oil and petroleum products are rising rapidly. Since the crude oil export ban was lifted in 2015, U.S. exports have more than doubled and exceeded 1 million barrels per day (mb/d) in 2017, averaging more than 1.5 mb/d in the last quarter of the year. China emerged as a major market for U.S. crude in 2017, importing 234 thousand barrels per day (kb/d). The primary driver of this has been the Brent–West Texas Intermediate (WTI) spread, which significantly widened in the last quarter of 2017, bringing the discount of U.S. exports to over $6 per barrel and a subsequent surge in Chinese imports. Natural gas liquids, of which the United States is already a net exporter, also grew significantly, with more than $1 billion worth of exports to China added to the ledger in 2017.

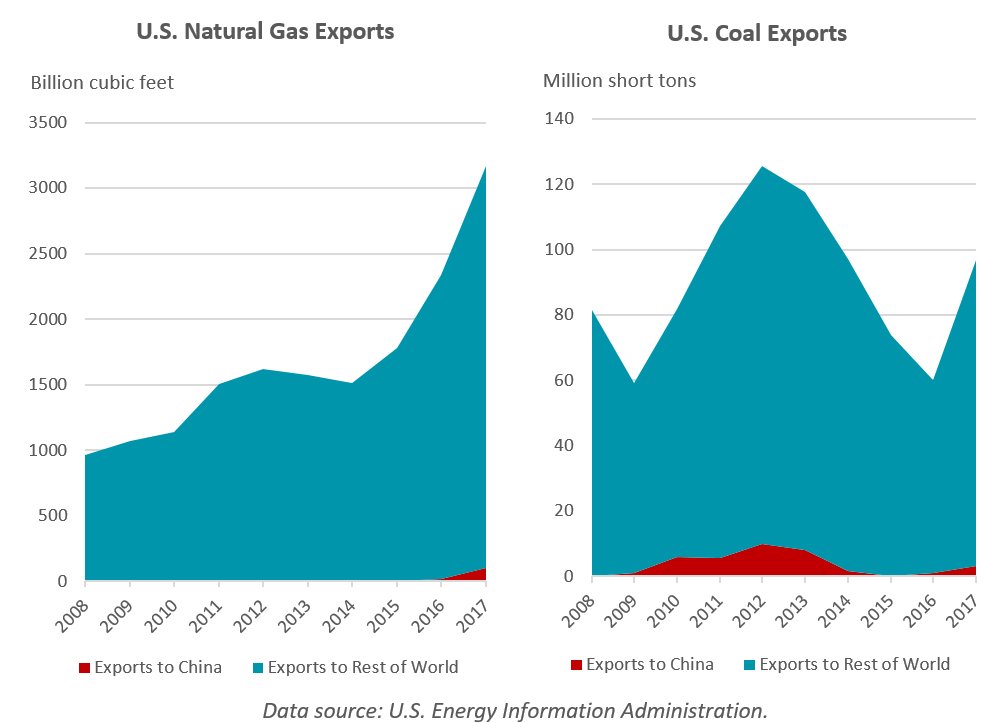

U.S. exports of LNG are also increasing, since Cheniere Energy’s Sabine Pass terminal in Louisiana came online in February 2016. Even with just one terminal online, U.S. LNG exports to China increased from 17.2 billion cubic feet (bcf) in 2016 to 103 bcf in 2017, making China the third-largest destination for U.S. LNG, behind Mexico and South Korea (the latter has been overtaken by China as the second-largest LNG importer in the world). With the start of Dominion Energy’s Cove Point LNG export terminal in Maryland in March, the United States is expanding its liquefaction capacity, clearing the way for potential midstream glitches for exporting LNG. At least four additional LNG terminals are scheduled to come online by the end of 2019, bringing the total capacity to 9.6 bcf per day. Given China’s growing appetite for LNG, many U.S. exporters appear eager to replicate Cheniere’s success in sealing a 25-year deal with the China National Petroleum Corp. in February. Moreover, the proposed Chinese investment in a joint development of an LNG export project in Alaska could expand bilateral gas trade ties if materialized.

Meanwhile, the growth margin for U.S. coal exports to China is less clear. When Cyclone Debbie devastated coal mines and a rail system in Australia and disrupted the supplies last year, China turned to the United States—among others—to help meet the shortfalls. In the same year, the United States saw its coal exports jump by about 60 percent and exports to Asia more than double. However, China is far from being a leading market for U.S. coal. In fact, China was the 10th-largest recipient of metallurgical and steam coal from the United States, accounting for 3.3 percent of total U.S. coal exports last year. Siting export terminals along the U.S. west coast would likely help increase the cost competitiveness of U.S. coal exports to China, but how robust bilateral coal trade can become is subject to China’s commitment to reducing coal dependence, as well as the fact that China has several coal suppliers in close proximity, including Australia, Indonesia, Mongolia, and Russia.

Oil and gas exports to China will contribute to reducing the U.S. bilateral trade deficit. Yet, how significant the contribution might be remains to be seen. As outlined earlier, the primary driver of the three-fold increase in the value of energy exports to China in 2017 was the increase in crude oil and natural gas liquids exports, which together contributed 85 percent of the growth in export revenues. The rate of growth of these export values is dependent on market dynamics including the Brent-WTI spread, the price of oil, and the extent to which U.S. producers can get their products to market in the face of export constraints. For example, even though crude oil exports increased 10-fold, the value of exports increased by a factor of 12, so the values also improved due to the higher price of oil but not as much as one might expect given the steep discount of when those exports tend to flow. Higher oil prices can also advantage U.S. LNG prices against oil price-linked LNG supplies from elsewhere and, as such, increase the volume of U.S. spot sales to China. However, Chinese imports of U.S. commodities may also be spurred on by the Chinese government, who now likely sees this as an easy opportunity to make the balance of trade more level, which the U.S. administration seems fixated on. This is corroborated by a news story from Reuters this week that the Chinese government has instructed Sinopec to boost crude oil imports from the United States.

In the first quarter of 2018, the United States sold $3.2 billion worth of energy commodities to China. While the volumes and values of U.S. exports to China will continue to grow this year, especially given the wide Brent-WTI spread and Chinese government pressure on state-owned enterprises to import U.S. crude specifically, $40–$50 billion is a still a very long way off. Booming U.S. energy exports in tandem with the fall in energy imports will of course help to reduce the overall U.S. trade deficit. However, it must be said that U.S. exports, particularly of oil (which would contribute the most significant portion of any growth) will flow to markets regardless of whether that is China specifically—that is, more U.S. barrels to China simply means fewer U.S. barrels to somewhere else. Additionally, Chinese efforts to take in more energy products from the United States that they would’ve been importing anyway from somewhere else represents an easy way to reduce their bilateral trade surplus with the United States with little to no cost.

Jane Nakano is a senior fellow with the Energy and National Security Program at the Center for Strategic and International Studies (CSIS) in Washington, D.C. Andrew Stanley is an associate fellow with the CSIS Energy and National Security Program.

Commentary is produced by the Center for Strategic and International Studies (CSIS), a private, tax-exempt institution focusing on international public policy issues. Its research is nonpartisan and nonproprietary. CSIS does not take specific policy positions. Accordingly, all views, positions, and conclusions expressed in this publication should be understood to be solely those of the author(s).

© 2018 by the Center for Strategic and International Studies. All rights reserved.