EST Rapid Roundup: Unpacking the National AI Framework

March 30, 2026 • 1:00 – 2:00 pm EDT

Hosted by Economic Security and Technology

Photo: the House Committee on Natural Resources

Gracelin Baskaran testified before the House Natural Resources Committee about the critical minerals commodity supply chain, specifically addressing U.S. vulnerabilities in mineral sourcing, the history of American minerals policy, and recommendations for building more resilient supply chains to reduce dependence on China.

Chairman Gosar, Ranking Member Dexter, and distinguished Members of the Committee, I am honored to share my views with you on this important topic. CSIS does not take policy positions, so the views represented in this testimony are my own and not those of my employer.

My name is Dr. Gracelin Baskaran. I am a mining economist and the founding director of the Critical Minerals Security Program at the Center for Strategic and International Studies (CSIS), where I lead research and policy engagement focused on strengthening resilient mineral supply chains critical to U.S. national security, economic competitiveness, and energy resilience. Over the past 13 years, I have worked extensively on critical minerals policy in the United States and internationally, with a focus on the geopolitical, economic, and security dynamics shaping this strategically vital sector.

The United States faces a pivotal moment in critical minerals security. Decades of policy drift, post-Cold War complacency, and misplaced confidence in globalized markets have left America deeply exposed in the minerals and materials that underpin its industrial economy, defense capabilities, and emerging technology sectors. The costs of strategic neglect are now being paid on the factory floor and in the defense industrial base.

The question before this Committee is not whether China has weaponized its minerals dominance.

That case has been settled, and the evidence is now extensive. The question is what the United States does about it. Specifically, how do we build a fully functioning, economically viable market for critical minerals, and how does it do so with sufficient speed and scale to protect American manufacturing, defense production, and long-term economic competitiveness? That is the challenge this testimony addresses. It is a challenge that cannot be solved by any single intervention. It requires a coordinated, systems-level response across industrial policy, trade, diplomacy, and investment, and it requires this Committee to press for policy that addresses the full supply chain from mine to manufactured good, not just the stages that are easiest to act on.

My testimony makes three principal arguments. First, America’s current vulnerability is not inevitable. Rather it is the product of specific, historically traceable policy choices. The United States was once the world’s dominant mineral producer and had sophisticated mechanisms for managing strategic resource risks; it systematically dismantled those mechanisms in the 1990s following the Cold War. Second, while supply-side interventions, including mining permits, domestic production incentives are important, they are insufficient without parallel attention to demand-side anchors across the mine-to-manufactured-goods supply chain. A mine without a refinery, a refinery without a manufacturer, and a manufacturer without a customer are each stranded assets. Third, even as the United States builds more resilient supply chains over the long term, it must strengthen its ability to withstand acute supply shocks in the near term. Building resilient markets takes years. China can impose export restrictions in days. Project Vault is a serious and structurally innovative attempt to close that gap. But its long-term value depends on whether it is given the statutory foundation that makes it durable across administrations.

Across every major conflict of the twentieth century, the United States mobilized extraordinary state intervention to overcome minerals supply shocks: strategic stockpiles, price controls, public financing, and foreign procurement. The historical toolkit for minerals security is broader and more creative than the current policy debate suggests. In 1918, the War Minerals Stimulation Law authorized the president to take over undeveloped mineral deposits, mines, and smelters deemed vital to the war effort, backed by a $50 million fund and the authority to create government corporations to manage production and distribution. In 1942, the federal government directly financed a nickel mine in Cuba because private markets were not delivering a material the defense industrial base required. In 1948, the Atomic Energy Commission established guaranteed minimum prices for uranium ore and committed to purchasing all domestically produced supply, effectively creating a guaranteed market that unlocked private investment in domestic production. In 1951, the National Production Authority banned copper use in more than 300 consumer products to ensure sufficient supply was available for defense applications.

The United States has also used trade instruments creatively to secure mineral access. Under the Agricultural Trade Development and Assistance Act of 1954, the government exchanged surplus agricultural commodities for strategic minerals. In 1982, the United States secured roughly 1.6 million tons of bauxite from Jamaica in exchange for dairy products. In 1981, President Reagan launched the first major stockpile purchase program in over two decades, warning explicitly of U.S. vulnerability to sudden raw material shortages affecting defense production. These examples are not historical curiosities. They are evidence that the United States has the authority, the precedent, and the institutional capacity to act decisively on mineral supply chains when the political will exists to do so.

However, after major conflict, the U.S. government dismantled those systems, only to confront the same vulnerabilities at greater cost the next time. The historical record reveals a recurring pattern of failure: overreliance on stockpiles in the absence of industrial capacity, neglect of processing and refining, erosion of domestic expertise, and complacent assumptions about the reliability of markets and allies. The post-Cold War drawdown was the most severe rupture in that pattern, hollowing out U.S. minerals capabilities precisely during the period when China was building its own, and amplifying American dependence on foreign and eventually adversarial supply chains in ways that are now structurally embedded and difficult to reverse.

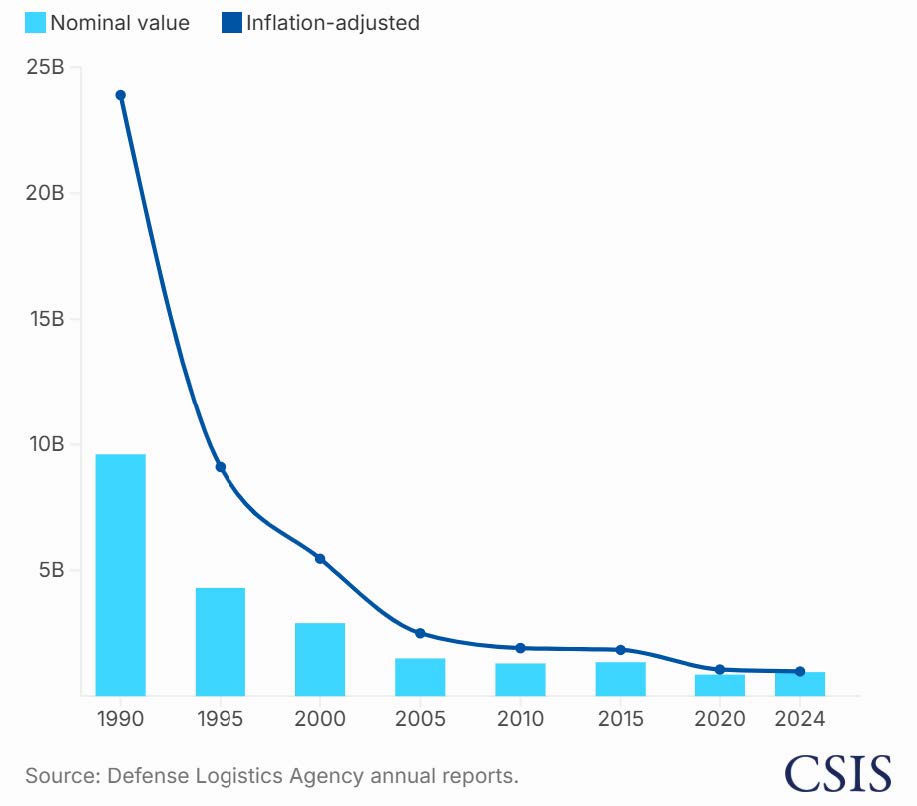

As the figure below shows, in 1990, the National Defense Stockpile held materials with an inflation-adjusted value of approximately $24 billion. By 2024, that figure had fallen to under $2 billion - a decline of more than 90 percent in real terms. Nominal values tell the same story: from nearly $10 billion in 1990 to under $2 billion today, with the steepest drawdown occurring in the 1990s when the United States was liquidating Cold War-era reserves on the assumption that globalized markets had rendered strategic stockpiling obsolete.

Figure 1: Value of U.S. National Defense Stockpile Inventory, 1990–2024

That assumption proved catastrophically wrong. The stockpile the United States spent decades building to buffer supply shocks was sold off precisely during the period when China was constructing its own minerals dominance. This was not fiscal prudence. It was a strategic miscalculation. The consequences are now being measured in halted production lines, delayed defense programs, and dependence on an adversary for materials the United States once held in reserve.

The central lesson of that history is clear. Critical minerals security is not a problem that gets solved and stays solved. It is a permanent national and economic security challenge that requires continuous stewardship, integrated industrial policy, and durable engagement with allies. Episodic crisis response and faith in market self-correction have been tried. The consequences are visible in the Ford plant that shut down in Chicago. This Committee has an opportunity to help ensure that the current moment of policy seriousness does not become another chapter in a familiar story of investment followed by neglect.

The historical record makes clear what sustained industrial policy looks like and what its absence costs. The challenge now is to apply those lessons to a competitive landscape that is in one important respect more difficult than anything the United States has faced before: an adversary that has deliberately engineered its dominance over global mineral supply chains and is actively using that dominance to undermine the commercial viability of alternatives.

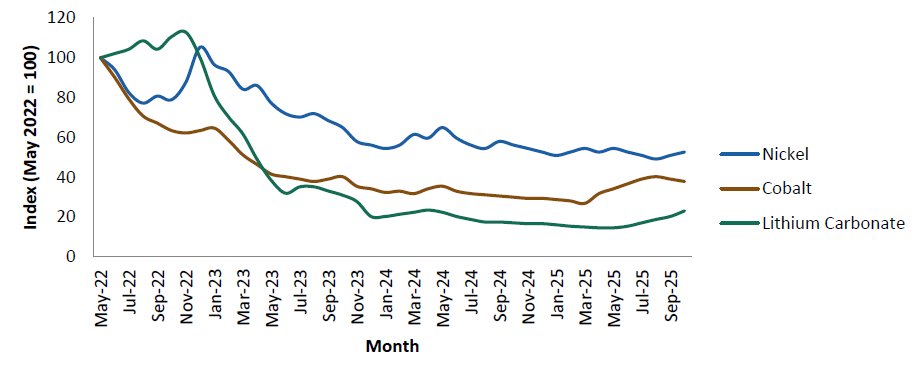

Chinese state-backed producers have repeatedly flooded markets with excess supply, driving prices to levels that make it economically unviable for mining and processing operations in the United States and allied countries to compete. This is not passive market behavior. It is a strategic instrument. By sustaining production well below the cost of extraction through state subsidy, China can force competing operations to close, consolidate its own market dominance, and then reassert pricing power once alternative supply has been eliminated. The price data in the figure below illustrates this dynamic directly. Lithium, cobalt, and nickel have all fallen by between 45 and 65 percent from their 2022 peaks, not because demand collapsed, but because Chinese supply expansion made it commercially irrational to invest in production anywhere else. During this time, Jervois opened the United States’ only cobalt mine in Idaho but was forced to close it within the same year due to collapsing prices. BHP closed its Nickel West operations and West Musgrave project in Australia, and Glencore shuttered its Koniambo Nickel SAS facility in New Caledonia. Albemarle delayed reopening its lithium mine in North Carolina.2

Figure 2: Critical Mineral Prices (May 2022 = 100)

Sources: LME, Fastmarkets, Argus

The United States has made meaningful progress on the supply side of the critical minerals challenge. Concessional financing, bilateral mineral cooperation agreements, and offtake arrangements have begun to shift the landscape of global mineral development. But supply-side interventions alone cannot solve a problem that is equally rooted in demand.

The United States needs demand-side mechanisms that create price certainty, reward sourcing from trusted suppliers, and generate the offtake commitments that make allied supply chains financially viable. Without them, markets will remain in structural disequilibrium, supply will continue to outpace bankable demand, prices will stay depressed, and the investment required to build resilient supply chains outside China will be slow to materialize. The supply side has begun to move. The demand side is where the policy gap remains largest.

Unfortunately, various policy interventions have not been vertically integrated from mine-to-manufactured goods. The CHIPS Act is the clearest example.3 The 2022 legislation committed over $280 billion to advanced chip manufacturing, packaging, and workforce development, directing significant funding to companies such as Intel and Micron to build and expand domestic fabrication facilities.4 It was a serious and necessary investment. But the CHIPS Act included no provisions to incentivize diversification of the critical mineral supply chains on which those fabrication facilities depend. You cannot build a semiconductor without gallium and germanium. The legislation funded the factory and ignored the feedstock.

The consequences were predictable and swift. In August 2023, China imposed export restrictions on gallium and germanium - two minerals for which the United States had made itself almost entirely dependent on an adversary. China accounts for 98 percent of the world's refined gallium production and 68 percent of germanium. The United States produces no gallium and less than 2 percent of refined germanium. The USGS has estimated that a 30 percent supply disruption of gallium alone could reduce U.S. economic output by $602 billion, equivalent to 2.1 percent of GDP. The bill funding America's semiconductor renaissance had not thought to ask where the semiconductors' raw materials would come from.5

This is not a criticism unique to the CHIPS Act. It reflects a structural blind spot in how the United States has approached industrial policy: building the end of the supply chain without securing the beginning. Correcting that pattern by ensuring that investments in downstream manufacturing are matched by enforceable commitments to diversify upstream mineral sourcing is crucial.

American manufacturing workers are on the frontline of mineral supply chain disruptions. In May 2025, Ford shut down production of the Explorer at its Chicago assembly plant for a week following China's April 2025 rare earth export restrictions.6 That was not a policy simulation or a war-game scenario. It was an American factory, employing American workers, that stopped because the United States lacked alternative sources for materials China chose to restrict.

The stakes are significant. The fifteen major automakers competing in the U.S. market directly employ approximately 388,000 American workers. FCA US, Ford, and General Motors alone account for 238,000 of them, nearly two out of every three U.S. autoworkers.7 When a rare earth shortage halts a Ford plant in Chicago, the consequences do not stay in the supply chain. They land on the factory floor, in the paychecks of workers in Illinois, and in the communities that depend on those jobs. The Ford Explorer shutdown was a warning, not an anomaly. Until the United States develops alternative sourcing and processing capacity for the minerals that run through its manufacturing economy, every major automaker and every worker employed by one remains exposed to decisions made in Beijing.

Beyond strengthening the supply and demand fundamentals that underpin the long-term economics of the mine-to-manufactured-good supply chain, the United States must also improve its ability to withstand acute supply chain shocks. Building resilient markets takes years. China can impose export restrictions in days. The gap between those two timescales is where American manufacturers, defense programs, and workers are most exposed, and it is the gap that strategic reserves and stockpiling mechanisms are designed to close.

Project Vault represents a structurally innovative departure from prior American approaches to strategic materials. Announced in February 2026, it created a U.S. Strategic Critical Minerals Reserve as an independently governed public-private partnership. Unlike the National Defense Stockpile, which was designed to support the defense industrial base, Project Vault is explicitly oriented toward civilian economic security by providing a strategic buffer of critical materials for commercial manufacturers against supply disruptions. It will cover all 60 minerals on the USGS 2025 Critical Minerals List, and has commanded the largest financing in EXIM's 92-year history.8

What makes Project Vault architecturally distinct is that it is demand-led rather than government-driven. Original equipment manufacturers identify which materials they need, at what grades and volumes, and commit financially to ensure those materials are available when disruptions occur. The financing model functions like a long-term insurance policy. EXIM provides a $10 billion loan, complemented by nearly $2 billion in private capital, to purchase and store critical minerals within the United States before shortages occur. Participating manufacturers pay a commitment fee in exchange for guaranteed access to specified materials during market disruptions, covering storage costs and interest over the life of their commitment. This structure gives manufacturers price certainty against the kind of spot-market volatility that China can and does weaponize, while generating a return for taxpayers through the premium structure. Rather than paying crisis prices when supply is disrupted, participants pre-fund supply certainty.9

However, Project Vault cannot be treated as a standalone solution to the challenge before us. History is instructive on this point. Across every major conflict of the twentieth century, stockpiles proved valuable as short-term shock absorbers and nothing more. They could cushion disruptions, stabilize markets, and buy time during crises. They could not replace resilient supply chains, domestic and allied processing capacity, skilled workforces, or well-functioning markets. Where those broader systems were weak or absent, stockpiles did not solve the underlying problem. They delayed its consequences. Project Vault is a necessary and well-designed buffer. The harder work of building the supply chains, processing capacity, and demand mechanisms that make that buffer unnecessary over time still remains largely ahead of us.

The United States must adopt a systems-level approach to minerals policymaking that addresses the full supply chain from mine to manufactured good. The United States has too often invested in one stage of the supply chain while leaving adjacent stages unaddressed, funding factories without securing feedstocks, opening mines without building refineries, and signing bilateral agreements without creating the downstream demand that makes those agreements commercially viable. While permitting reform is a necessary foundation for domestic production, it is not sufficient on its own. A mine that cannot find a buyer at a viable price will not stay open regardless of how quickly it receives its permit. This Committee should press for a comprehensive framework that treats extraction, processing, refining, component manufacturing, and demand anchors as interdependent stages of a single system rather than discrete policy problems. A mine without a refinery is a stranded asset. A refinery without a manufacturer is a stranded asset. Getting the architecture right means ensuring that investments at each stage of the chain are matched by commitments at the stages that follow.

China understands this arithmetic. Its dominance in critical minerals is not solely a function of geology or even of state subsidy. It is a function of market scale. China consumes enough of its own processed minerals output to justify the infrastructure investments that sustain its processing dominance, and it uses that scale to set prices, crowd out competitors, and make it economically irrational for producers to develop alternative supply chains. The United States cannot replicate that scale alone.

The solution is to aggregate demand across allies. The United States has a population of 343 million people. Pooling demand with Australia, the United Kingdom, India the European Union, Canada, Japan, and South Korea expands the market to approximately 2.6 billion people, roughly increasing the demand base for minerals-intensive goods by 7.5-fold. That collective market will begin to provide the economies of scale that can make allied processing and refining facilities commercially viable. A smelter or separation facility that cannot survive on American offtake alone can survive if it can count on guaranteed demand from a coalition of allied buyers.

The United States must move beyond bilateral minerals frameworks toward a coordinated allied demand aggregation mechanism, one that pools procurement commitments, aligns offtake agreements across partner nations, and creates the market signal large enough to attract the private capital required to build the supply chains the United States cannot build on purchasing power alone. The vehicle for doing so already exists. The Forum on Resource Geostrategic Engagement, announced at the February 2026 Critical Minerals Ministerial, provides the diplomatic architecture for precisely this kind of coordinated allied engagement.11 FORGE's mandate should extend beyond supply-side coordination to include a formal allied demand aggregation mechanism with two concrete components.

First, a joint offtake commitment framework among FORGE member nations, modeled on the NATO defense spending commitment, under which participating governments agree to source specified percentages of critical mineral procurement from allied producers. This would give mining and processing companies the long-term demand certainty required to attract private financing for projects. The Serra Verde rare earth project in Brazil is a cautionary example of what happens without such a framework: despite receiving support through the Minerals Security Partnership, it contracted the majority of its output to China because China was the only buyer with sufficient and reliable demand at the time agreements were signed.12 A coordinated allied offtake commitment would change that calculus.

Second, a coordinated stockpiling commitment among FORGE members, under which allied governments agree to maintain strategic reserves of specified minerals and coordinate drawdown and replenishment decisions. Japan has maintained a commercial critical minerals stockpile since 1983.13 The United States has Project Vault. Coordinating them through FORGE would amplify their collective deterrent effect against Chinese market manipulation while reducing the cost of maintaining individual national reserves.

Taken together, these components would transform FORGE from a diplomatic forum into a functioning allied minerals market that is large enough to support the processing facilities, refining capacity, and supply chain investments that no single allied nation can justify on its own demand base alone.

Create an industry-agnostic incentives framework to source critical minerals from the United States and allied countries. Current policy incentives for mineral sourcing are fragmented by sector and application. Tax credits under the Inflation Reduction Act, for example, were structured around clean energy and electric vehicles, leaving defense manufacturers, semiconductor producers, and other advanced industries without equivalent tools to diversify their mineral supply chains. The result is a patchwork of incentives that rewards sourcing decisions in some industries while providing no comparable mechanism in others. China's rare earth export controls did not discriminate by end use. American policy should not either.

An industry-agnostic framework would extend sourcing incentives to any manufacturer that sources critical minerals from domestic producers or from allied and partner countries with which the United States has a qualifying minerals agreement. This could take the form of a production tax credit modeled on the Section 45X Advanced Manufacturing Production Tax Credit, extended upstream to reward verified sourcing from trusted suppliers regardless of the final product being manufactured. It would apply equally to an automaker sourcing rare earths for magnets, a defense contractor sourcing tungsten for munitions, and a chipmaker sourcing gallium for semiconductors.

The strategic logic is straightforward. Allied producers in Australia, Saudi Arabia, and across the Global South need long-term demand commitments to justify the capital-intensive investments required to bring new supply online. American manufacturers need price certainty and supply security to justify shifting procurement away from lower-cost Chinese suppliers. A well-designed sourcing incentive bridges both needs simultaneously, creating the demand signal that unlocks allied supply while reducing the cost differential that currently makes Chinese sourcing the default. Without that bridge, bilateral diplomatic frameworks and mining permits will continue to produce announcements without transforming the underlying structure of supply chains.

Align tariff policy with strategic U.S. priorities around mineral processing. The administration has correctly identified mineral processing as the central vulnerability in American supply chains. The January 2026 Section 232 announcement was explicit on this point, stating that mining a mineral domestically does not safeguard the national security

of the United States if the country remains dependent on a foreign adversary for processing. That diagnosis is exactly right. The White House has shown that alignment between policy tools is key. At the Critical Minerals Ministerial hosted at the State Department February 4, 2026, Vice President JD Vance noted that it is important to “Align trade policy, development finance, and diplomatic engagement towards a shared strategic objective. And that objective is very simple: diversifying global supply in the critical minerals market while strengthening the partner countries who help all of us in this shared effort.”14

However, tariffs as currently structured, are undermining the very mine-to-manufactured-good supply chain the United States needs to build. Copper illustrates the problem directly. The United States currently produces more copper ore than it can process domestically and is a net copper exporter. That gap will widen significantly over the next three years as new domestic mining capacity comes online, including the Resolution Copper project in Arizona, which alone could meet approximately 25 percent of American copper demand. Yet no new copper smelters are being built in the United States, because the economics of smelter construction do not currently pencil out without substantial – and ongoing – capital support.

Japan presents an immediate solution. Japanese smelters have significant unutilized copper processing capacity and the technical expertise to handle American copper concentrate at scale. Under an effective allied supply chain strategy, the United States would export copper concentrate to Japan for smelting and refining, then import the processed copper back for domestic manufacturing. That is precisely the kind of mine-to-manufactured-good partnership within trusted allied nations that U.S. policy says it wants to build. Section 232 tariffs make it uneconomic to do so. The tariff barrier that was designed to protect American industry is instead preventing American copper from being processed by an ally and returned to American factories.

This is not an argument against tariffs as a tool. Tariffs have a legitimate role in protecting domestic industry and pressuring adversaries. It is an argument for tariff policy that is designed in coordination with minerals strategy rather than in isolation from it. The administration has the authority to structure Section 232 agreements with allied nations in ways that lower barriers for processing trade in strategic minerals while maintaining protective measures against adversarial suppliers. The most effective mechanism for doing so would be a preferential trade zone for critical minerals among trusted partners, one that allows materials to move freely from mine-to-manufactured good across allied supply chains without tariff penalties at each stage of processing. Copper mined in Arizona, smelted in Japan, and returned to an American factory for manufacturing should not face the same trade barriers as copper processed in China. A preferential zone that distinguishes between allied processing and adversarial processing would align tariff policy with the strategic objectives the administration has already articulated, and would give allied between allied processing and adversarial processing would align tariff policy with the strategic objectives the administration has already articulated, and would give allied partners the commercial incentive to invest in the processing relationships the United States needs.

The United States has been here before. It has built sophisticated mechanisms for managing strategic resource risk, dismantled them when the sense of urgency faded, and paid the price when the next crisis arrived. The post-Cold War liquidation of the National Defense Stockpile, the closure of Mountain Pass rare earths mine, and the abdication of domestic processing capacity were not acts of negligence. They were deliberate choices made by policymakers who believed that globalized markets had rendered strategic resource competition obsolete. That belief proved catastrophically wrong, and its consequences are now visible.

The current moment is different in one important respect: the political will to act is present, and it is bipartisan. Project Vault, the February 2026 Critical Minerals Ministerial, the Section 232 executive order, and the bilateral frameworks signed with more than twenty countries represent the most serious sustained investment in mineral security since the Korean War. That momentum is real and it matters.

But momentum is not the same as strategy. The United States has supply-side tools that are beginning to work, a stockpiling mechanism that is structurally well-designed, and diplomatic frameworks that are expanding allied engagement. What it does not yet have is a coherent demand-side architecture that makes allied supply chains commercially viable over the long term, a tariff policy aligned with rather than working against its minerals strategy, or the statutory foundation that would protect its most important new mechanisms from the peacetime political pressures that have eroded prior investments.

The recommendations in this testimony are the minimum set of interventions required to close the gap between the policy the United States says it wants and the market conditions that currently make that policy undeliverable.

Thank you for the opportunity to testify today. I look forward to your questions.

Please consult the PDF for references.