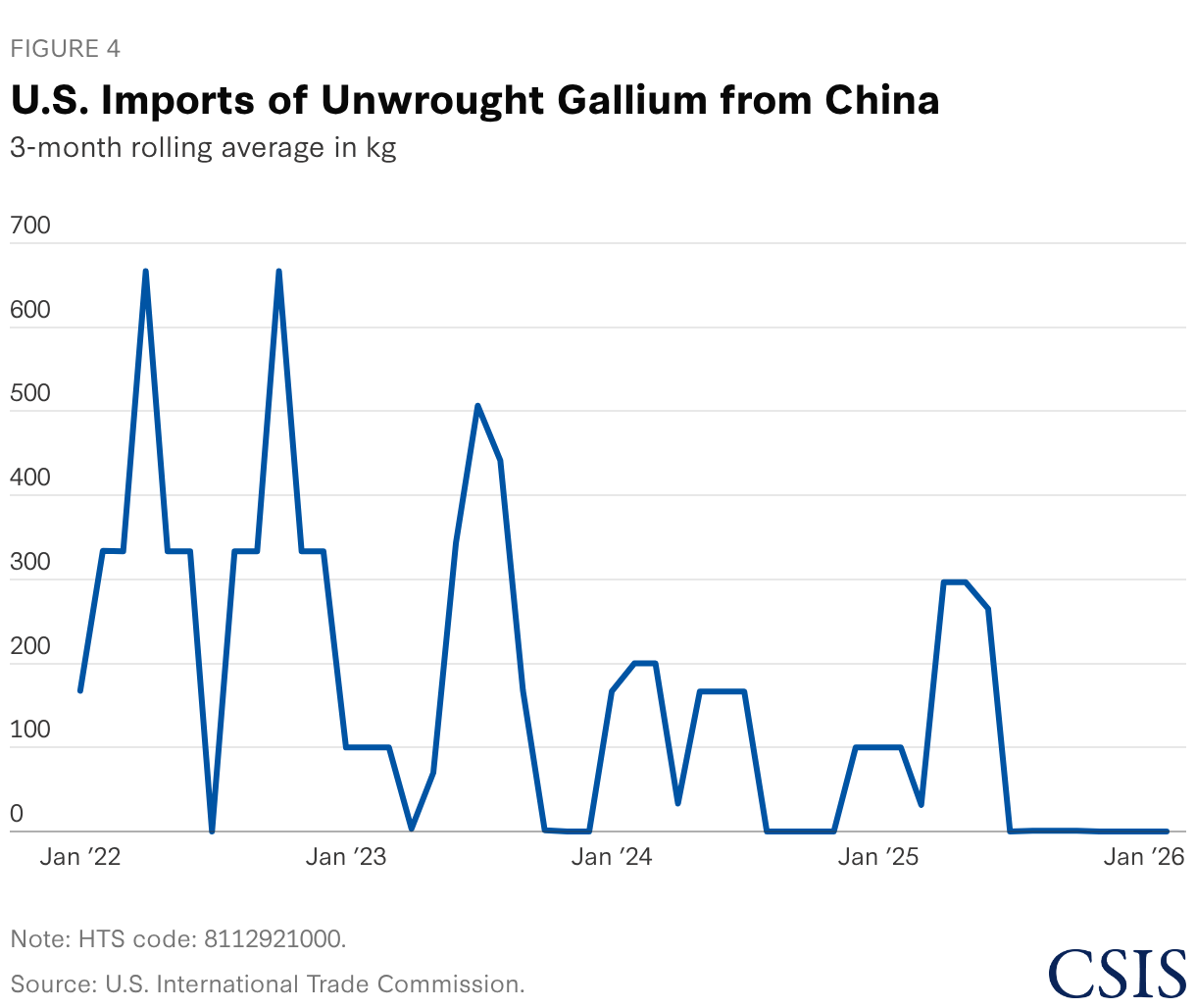

Trade data should be interpreted cautiously given gallium’s opaque and relatively small market. Customs and trade agencies around the world do not record gallium trade in uniform ways, making direct comparison difficult.

Additionally, companies often move material between their affiliated facilities in different countries, inflating the appearance of cross-border trade. For example, Neo Performance Materials, one of the main suppliers serving North American customers, operates facilities in both Canada and the United States, and likely frequently transports material across the border between its facilities.

There is also evidence of attempts to circumvent China’s restrictions. In July 2025, a U.S. company reported that Chinese suppliers were successfully shipping gallium by intentionally mislabeling it as other materials and routing it through third countries in order to evade export controls. Given the rapidly rising price of gallium in global markets, incentives for Chinese suppliers to smuggle their product will continue to grow.

Chinese authorities have attempted to clamp down on these practices, but enforcement is difficult. Gallium is traded in small quantities and required only in modest volumes for many applications, which makes illicit shipments harder to detect.

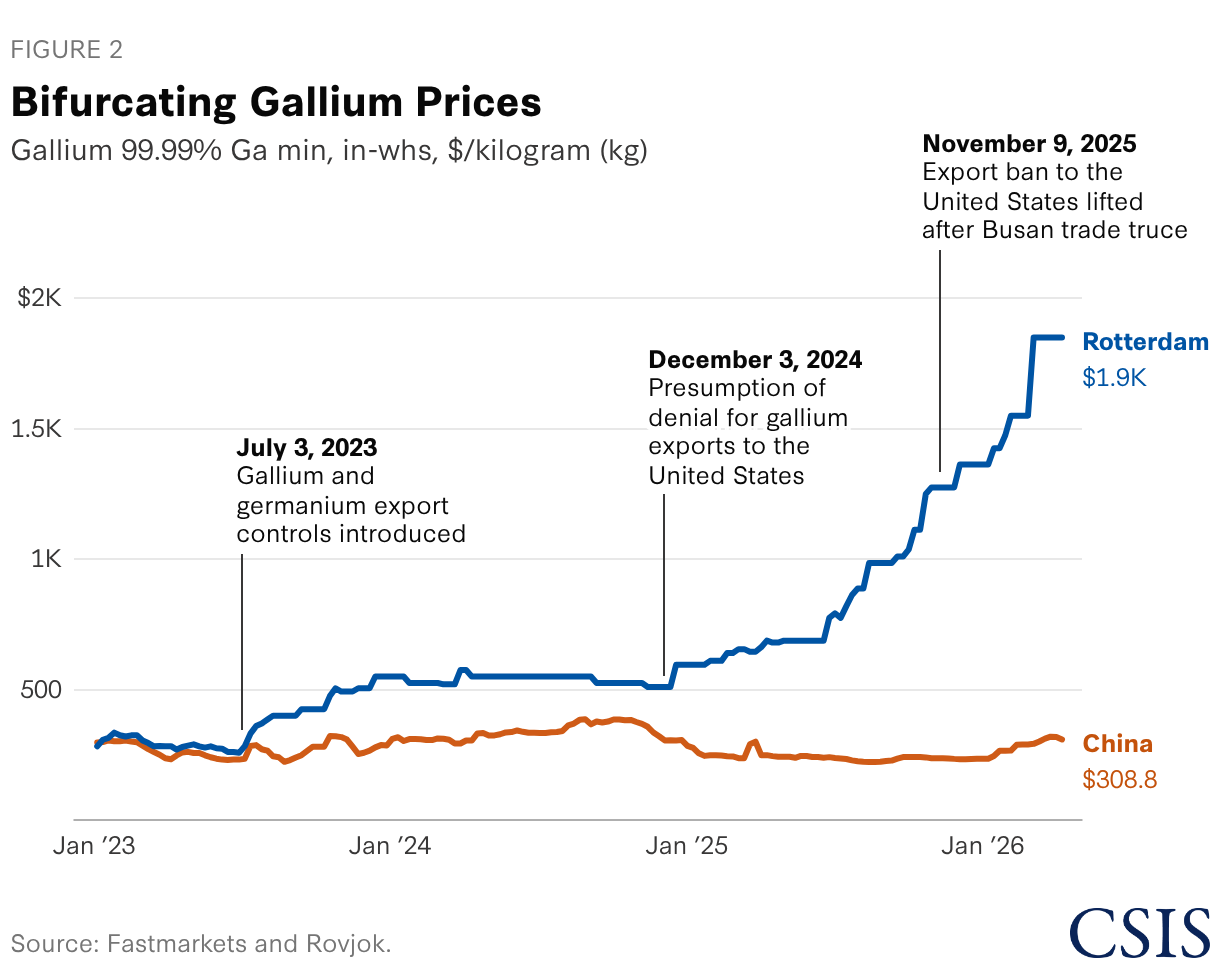

Even accounting for these complexities, the price surge and trade data both point to the same conclusion: Little Chinese gallium is reaching global markets.

Public statements from global companies provide additional insight. AXT, a major producer of gallium arsenide semiconductor substrates with operations in both China and the United States, acknowledged in its Q4 2025 earnings report that while it “has generally received the required permits for exports to countries in Asia and Europe, our U.S. gallium arsenide customers are considered ‘dual use’ customers. . . . As such, no permits for the export of gallium arsenide to the U.S. have yet been approved.”

Neo Performance Materials, the primary North American supplier, has reported similar pressures. In its Q4 2025 earnings release, the company stated that Chinese export restrictions continued to limit gallium availability and push prices higher. While Neo has the ability to recycle gallium scrap, the company noted that “despite strong demand, rising prices, and expanding margins, business growth is restrained by limited gallium scrap supply.”

Taken together, these indicators suggest that China’s suspension of the presumption-of-denial rule has not translated into a meaningful increase in exports. Some gallium continues to circulate through recycling and indirect channels, but the total volume available to global markets has fallen sharply.

Possible Explanations

Without direct visibility into the policy process in Beijing, it is impossible to determine the precise reason for the continued delay in gallium export licensing. Still, it is worth considering several plausible explanations:

- Bureaucratic delay: The simplest explanation is that MOFCOM is struggling to keep up with a massive licensing backlog likely piling up since 2025. China’s export control system is relatively new and may lack the administrative capacity to manage a surge of applications, especially with more stringent requirements for verifying extensive details about end users. However, the longer export licenses remain in limbo, the less convincing this explanation becomes.

- Dual-use concerns: Beijing may have genuine concerns about the military end uses of gallium. Gallium compounds are widely used in defense electronics, particularly in radar systems and advanced communications equipment. Chinese authorities may be reluctant to approve exports that could ultimately support U.S. military capabilities, even if the formal restriction has been suspended.

- Industrial strategy: Limiting global gallium supply could provide an advantage to Chinese firms developing technologies based on emerging gallium compounds such as gallium nitride (GaN) or gallium oxide. These materials are increasingly important for power electronics and high-performance semiconductors, which drive strategic industries like AI, robotics, and aerospace. By restricting exports of raw materials, China could tilt the competitive landscape in favor of its domestic manufacturers.

- Maintaining strategic leverage: A final explanation is that Beijing intends to maintain strategic leverage in its negotiations with the Trump administration. Keeping tight control over gallium exports gives Beijing a low-cost source of bargaining power. Even without an explicit ban, the ability to restrict supply creates uncertainty that can influence diplomatic discussions and potentially help China extract concessions on technology export controls or other strategic issues.

Containing the Fallout

While policy attention in Washington has understandably focused on acute shortages of more high-profile minerals such as rare earths and tungsten, gallium should not be ignored. Gallium plays a critical role in several emerging technologies that are central to U.S. economic and national security interests. GaN semiconductors are widely used in power electronics for data centers, electric vehicles, and renewable energy systems. They also enable high-performance radar and electronic warfare systems used by modern militaries.

Demand for these technologies is expected to increase sharply in the coming decade. Planned investments in missile defense and advanced radar systems, such as the Golden Dome homeland defense system proposed by President Trump, will require substantial quantities of gallium to produce.

Ongoing conflicts are creating an even more urgent need to replace equipment made with gallium. Experts estimate that a single Terminal High-Altitude Area Defense (THAAD) missile defense battery, for example, requires roughly 77 kilograms of gallium. Public reporting suggests that Iranian strikes have damaged or destroyed several of these systems at military bases across the Middle East in its war with the United States and Israel in early 2026, meaning they will need to be replaced.

Unfortunately, the United States has few good options in the short term. Despite rapidly rising demand from strategic sectors, there is simply no immediate alternative to China for gallium. Under the Trump administration, the Pentagon and other agencies have committed millions in new investments in both domestic and overseas gallium production facilities to create stable substitute suppliers. However, these projects are still nascent and will likely not reach full operational capacity before mid-2027, at best. In the meantime, recycling can help offset some shortages, but recoverable gallium is limited to recycled feedstock from pre-consumer scrap—and is ultimately still reliant on Chinese-origin supply.

Stockpiling is another potential response, but it creates its own challenges. The United States has launched Project Vault, an ambitious $12 billion effort to create a stockpile for strategic minerals. However, the utility of stockpiling is diminished once a shortage has already materialized. Large new purchases by government buyers in an already tight market could push prices even higher and worsen the shortage.

Diplomacy can play a role in the immediate term. President Trump’s visit to China this week provides an opportunity to raise these issues. During the visit and in future U.S.-China trade talks, U.S. negotiators will need to keep critical minerals, including gallium, on the agenda and work to ensure that China abides by its commitments.

Aidan Powers-Riggs is an associate fellow with the iDeas Lab at the Center for Strategic and International Studies (CSIS) in Washington, D.C. Brian Hart is deputy director and fellow of the China Power Project at CSIS. Matthew P. Funaiole is vice president of the iDeas Lab, Andreas C. Dracopoulos Chair in Innovation, and senior fellow in the China Power Project at CSIS.