Warfighting and War Winning in Space

May 26, 2026 • 1:00 – 1:45 pm EDT

Hosted by HTK Series

Photo: GREG BAKER/AFP/Getty Images

As China comes under increased scrutiny over its global energy investments, Chinese authorities have announced a series of multilateral initiatives to “green” its Belt and Road initiative (BRI). Of these, the BRI International Green Development Coalition and the Green Investment Principles for the Belt and Road Development show the most promise, yet they are in danger of failing to deliver on their stated goals. As long as investors on the ground only need to follow host countries’ environmental standards and Belt and Road members can free ride on Chinese “green” initiatives, investment along the Belt and Road—particularly in new fossil fuel energy infrastructure—will undermine China’s political rhetoric and climate targets. While just recognizing the problem is a positive step for China, these initiatives are generally too voluntary to be effective, too duplicative to be adding value, and too opaque to be adequately assessed.

For the last decade and a half, China has taken a prominent role in investing in and developing infrastructure projects around the world, particularly in the energy sector. These investments, which since 2013 have been loosely connected under the banner of the Belt and Road Initiative (BRI), have garnered a great deal of attention and criticism for their geopolitical, financial, and environmental implications. In response, China has launched a wide array of multilateral initiatives of varying scope and ambition to “green” the BRI. While just recognizing the problem is a positive step for China,

these initiatives are generally too voluntary to be effective, too duplicative to be adding value, and too opaque to be adequately assessed.

Though exact figures are hard to come by, China’s overseas investments reached a peak of $183 billion in 2016, and its $38-45 billion in overseas development finance is estimated to represent approximately a third of global official development assistance (ODA) each year. China’s two largest policy banks—the China Development Bank (CDB) and the China Export-Import Bank (EXIM)—now provide as much energy finance to foreign governments as all multilateral development banks (MDBs) combined. With more than a fifth of this money going toward coal since 2001 and fully three-quarters to some sort of fossil-fuel investment, the climate change implications of the BRI are highly problematic.

The development of these energy sector projects is framed by two fundamental strategic issues: (1) the need to provide adequate supplies of affordable energy to sustain growth, and (2) the imperative to reduce emissions to tackle global climate change. Luckily, marrying these two objectives to achieve sustainable energy-fueled growth is more possible now than at any time in the past. The task is to figure out which strategies for engaging the BRI will be most effective in delivering these outcomes. This brief explores the BRI and some of China’s recent attempts to turn the BRI “green,” particularly through the BRI International Green Development Coalition and the Green Investment Principles for the Belt and Road Development.

China would like the world to see its so-called “Belt and Road 2.0” underpin a grand new era of Chinese leadership, replete with sustainable development, economic growth, and continental interconnectivity. However, it remains unclear whether these new initiatives will deliver on the values they were created to uphold. Ultimately, this will depend on China’s ability (and willingness) to truly transition the BRI from opaque bilateral deals to inclusive, results-driven multilateralism and whether it can add teeth to its voluntary guidelines and standards.

While just recognizing the problem is a positive step for China, these initiatives are generally too voluntary to be effective, too duplicative to be adding value, and too opaque to be adequately assessed.

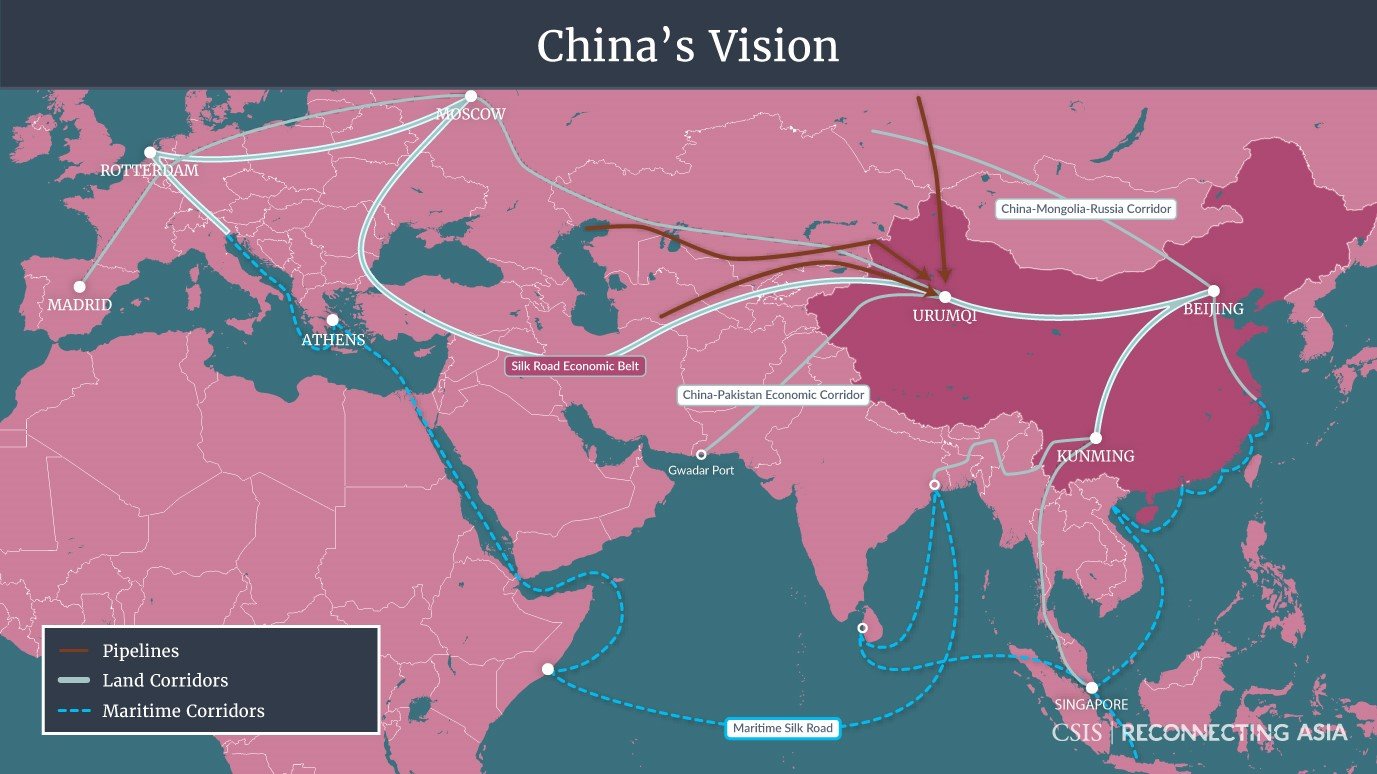

Since it was first announced in 2013, the BRI has grown to cover nearly every aspect of China’s foreign and economic policy. As much an “all-encompassing slogan” as a centralized grand strategy, the BRI reflects both the best and worst of China’s foreign policy. On the one hand, there is little doubt that Central and Southeast Asia—not to mention the African, Latin American, and Eastern European countries that now also form part of the Belt and Road—are suffering from a growing infrastructure gap and that China has the surplus capital to help fill it. On the other, provincial governments and private companies have been able to use the BRI slogan to engage in infrastructure projects of varying quality and environmental sustainability, and without consideration for host countries’ debt repayment capabilities, which has led to growing criticism of the BRI and hurt China’s reputation.

Part of the perceived problem with the BRI was that the scale of its ambition was not matched by the requisite governance infrastructure or institutions to support it. As such, the BRI has also become the focal point of China’s recent attempts to reshape the international order (and its reputation with it) by building new multilateral institutions, such as the Asian Infrastructure Investment Bank (AIIB) and the New Development Bank (NDB). While BRI projects continue largely to be bilateral exercises between governments—including, quite often, provincial-to-provincial agreements—Xi Jinping’s attempts to turn the Belt and Road Forum into an international summit reflect China’s increasingly sophisticated international statecraft and growing ambitions.

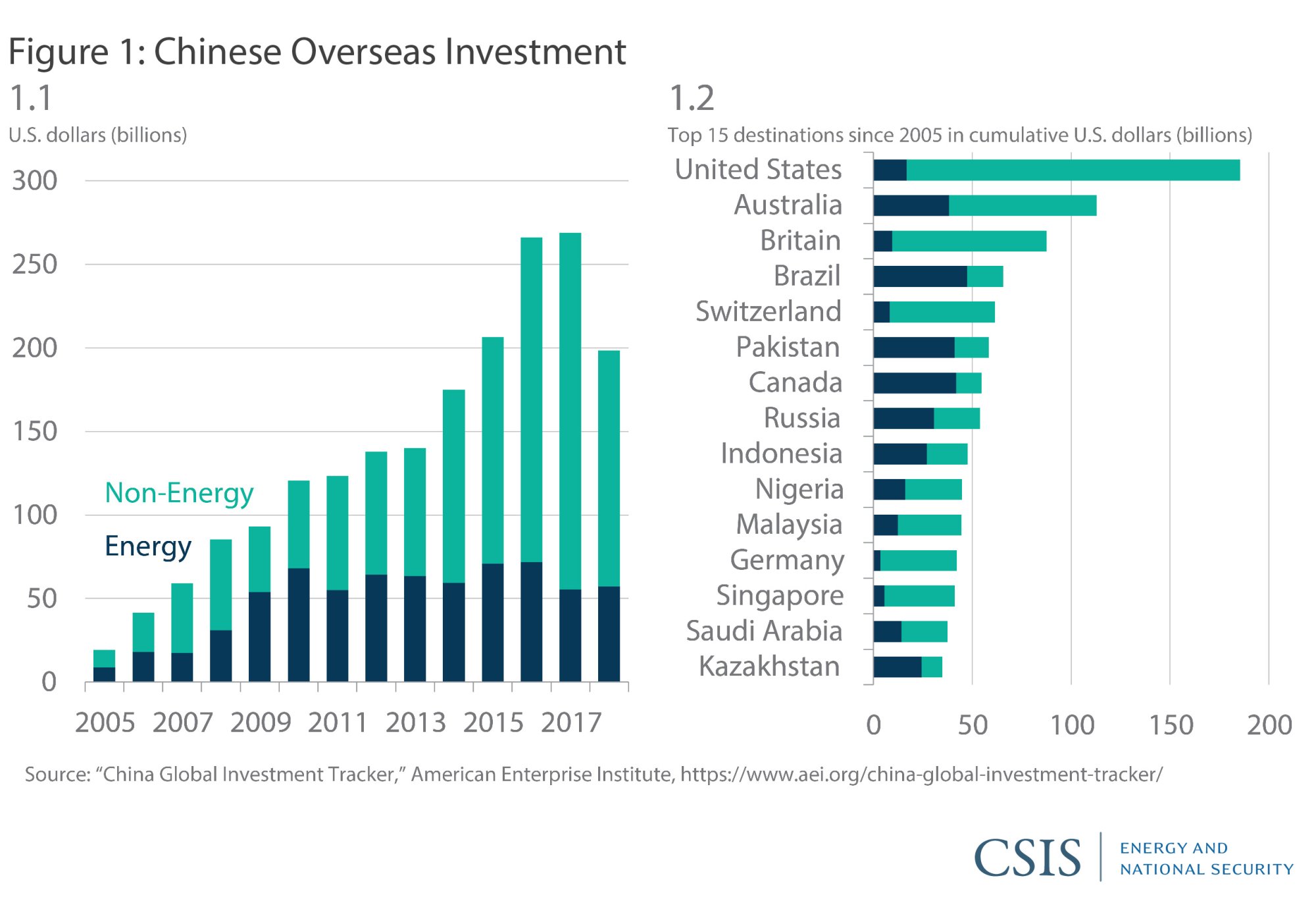

In the years since the global financial crisis disrupted China’s export-oriented growth model, China has grown to become the world’s largest source of foreign direct investment (FDI) and ODA. According to AEI’s China Global Investment Tracker, Chinese investment and construction since 2005 has exceeded $2 trillion, over a third of which has been in the energy sector.1 Figure 1.1 shows how Chinese investment steadily increased over the last 10-15 years, before starting to decline in 2018. This decline has been driven by a large fall in transactions by state-owned enterprises, who have had less support from Beijing for global activities, as well as by recent trade disputes with the United States. Developed countries, such as the United States, Australia, and the United Kingdom, have been the most popular destinations for investment, as have energy-intensive countries like Russia, Brazil, and Canada and countries with fast-growing energy demand like Indonesia and Pakistan (Figure 1.2)

Chinese authorities have promised to deliver trillions of dollars in investment throughout the Central and Southeast Asian regions to fill large and growing infrastructure gaps. Unsurprisingly, many countries initially welcomed Chinese investment with open arms, particularly those in desperate need of additional energy capacity to meet the demands of growing economies. Pakistan famously signed on in 2015 to establish a China-Pakistan Economic Corridor (CPEC) between Gwadar, a port in southern Pakistan, and the Xinjiang region in western China. Pakistan’s prime minister at the time, Nawaz Sharif, proclaimed that “friendship with China is the cornerstone of Pakistan’s foreign policy.” With the collection of projects now estimated to be worth some $62 billion, the economic corridor was meant to be a huge injection into Pakistan’s economy and an investment in its energy future for decades to come.

In the years since the global financial crisis disrupted China’s export-oriented growth model, China has grown to become the world’s largest source of foreign direct investment

Instead, CPEC has become emblematic of growing wariness of BRI projects, with environmentalists voicing increasing concerns over the type of energy projects being built and economists lamenting the conditions of Chinese lending. Even with only about a third of CPEC projects materializing so far, Pakistan has needed to go to the IMF to seek a financial bailout as its debts mount, foreign reserves dwindle, and international lenders balk at its economic outlook. Sri Lanka had a similar experience with the development of its port, Hambantota, which is now subject to a 99-year lease to China while Sri Lanka is mired debt from the project. The experience of countries like Pakistan and Sri Lanka have led several commentators to refer to the BRI as China’s “debt-trap diplomacy,” an image China is now desperately trying to avoid. Furthermore, China has come under fire for the environmental track record of BRI projects. Following these criticisms, at the first Belt and Road Forum in May 2017, President Xi Jinping noted in his keynote address the need to pursue a “new vision of green development and a way of life and work that is green, low-carbon, circular and sustainable.”

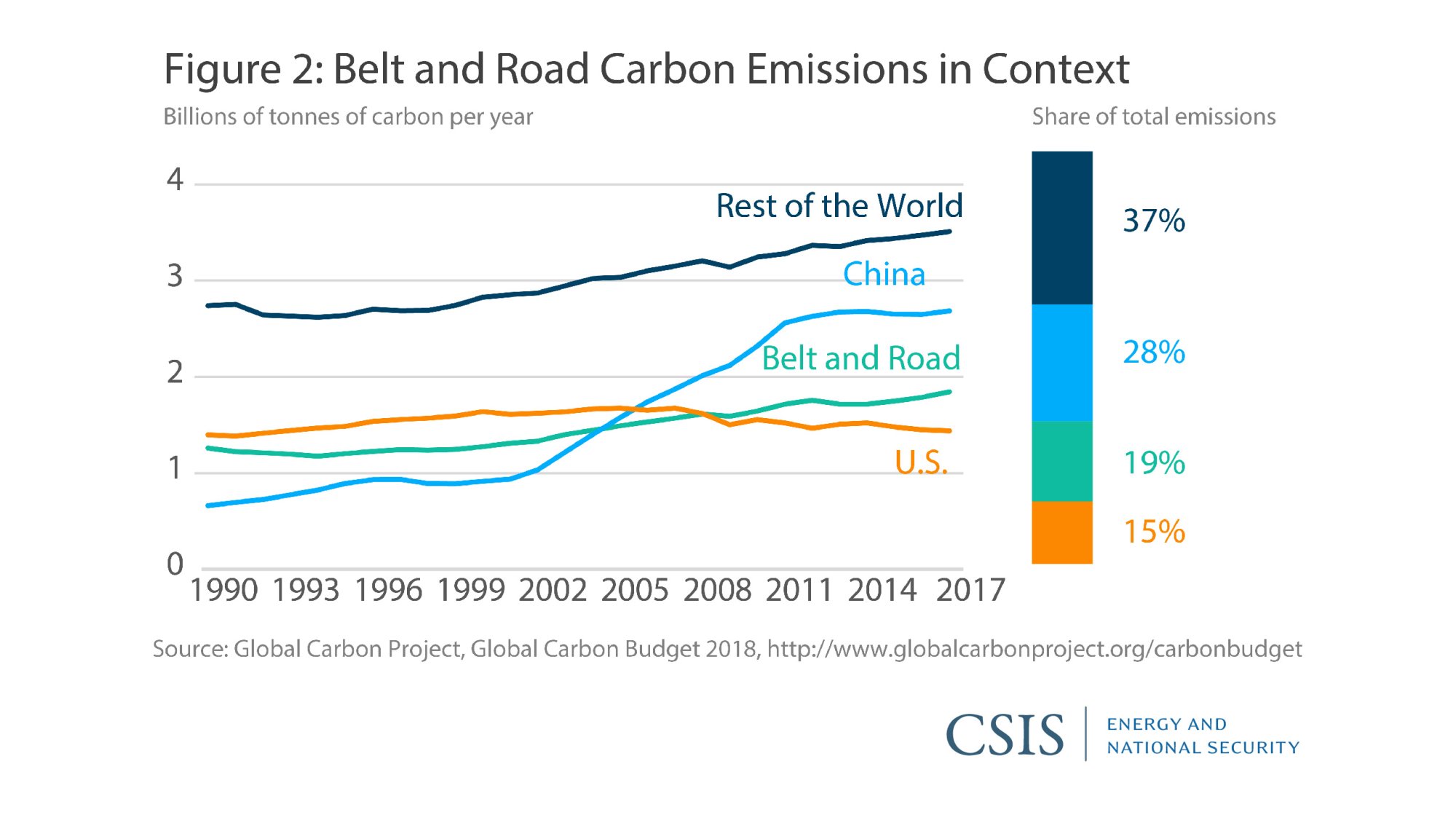

To a concerning degree, one simply must hope China will back up its rhetoric with action. BRI countries comprised approximately 19 percent of all CO2 emissions in 2014, still below low China’s 28 percent contribution (see Figure 2). At a combined 48 percent, China and BRI countries emit roughly as much CO2 as the rest of the world combined. China’s choices, therefore, with respect to what fuel sources it chooses to invest in and the environmental standards it imposes on its foreign investment, will be an important factor in how successfully the world deals with the climate crisis.

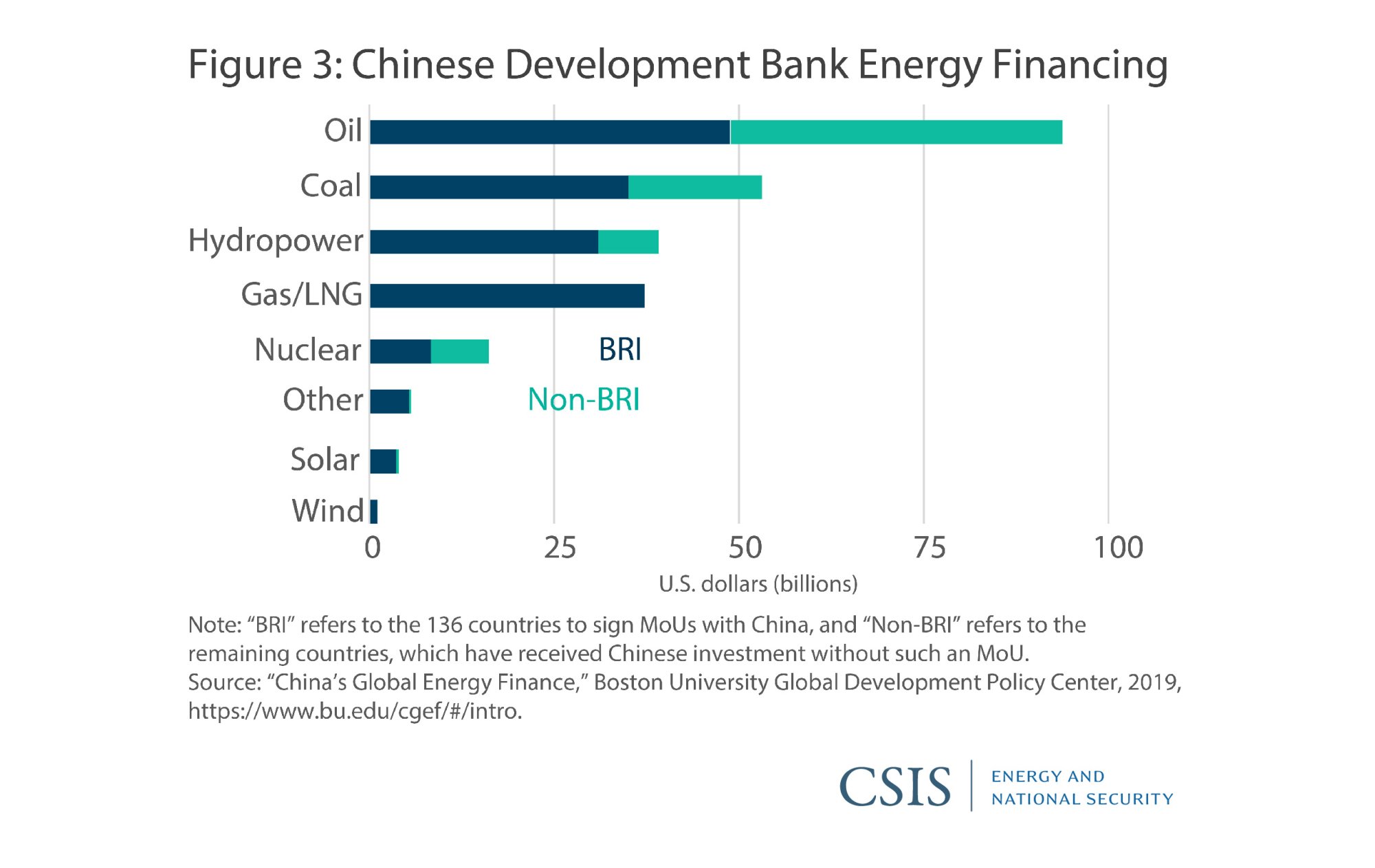

Unfortunately, of the $540 billion in energy investment made by Chinese development banks since 2005, 74 percent has gone towards hydrocarbon-related projects (see Figure 3).2 A World Resources Institute report similarly found that the vast majority of energy-sector investments made under the BRI were in fossil-fuel assets that will lock countries into carbon-emitting fuel sources for decades. They estimated that between 2001 and 2016, more than 50 coal-fired power plants were financed by Chinese institutions, the majority of which used the most carbon-intensive coal technologies. Another report estimates that Chinese financial institutions have committed or offered funding to over a third of all coal development taking place outside of China and India. Once again Pakistan is illustrative, with China having invested in 13 separate coal projects worth over $11 billion—25 percent of all Chinese investment in the country. However, with several of these projects already experiencing financial difficulties, it is uncertain how many will reach completion.

The vast majority of energy-sector investments made under the BRI were in fossil-fuel assets that will lock countries into carbon-emitting fuel sources for decades.

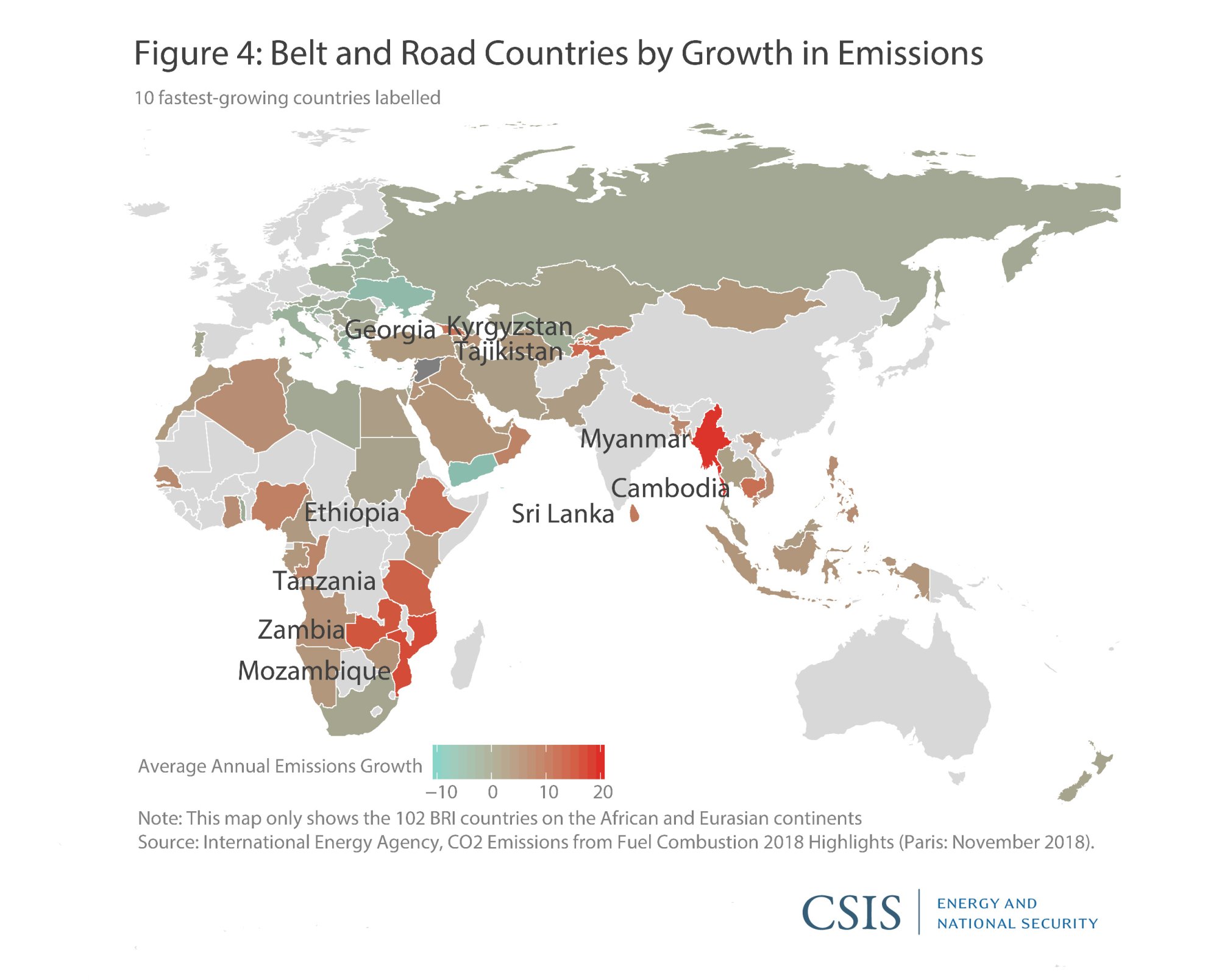

These trends are important in a region projected to grow significantly in its GDP, population, and greenhouse-gas emissions. Ten BRI countries are experiencing double-digit annual growth in CO2 emissions (Figure 4). In emerging Asia, for example, power capacity is expected to almost double between 2017 and 2030 with its share of global coal demand increasing from 20 to 29 percent. Furthermore, many BRI countries are projected to be some of the worst-affected by climate change and extreme weather events. Pakistan, for example, is estimated to be the eighth most at risk of climate change impacts and to have already suffered from 145 extreme weather events related to climate change, resulting in the loss of over 10,000 lives.

The vast majority of energy-sector investments made under the BRI were in fossil-fuel assets that will lock countries into carbon-emitting fuel sources for decades.

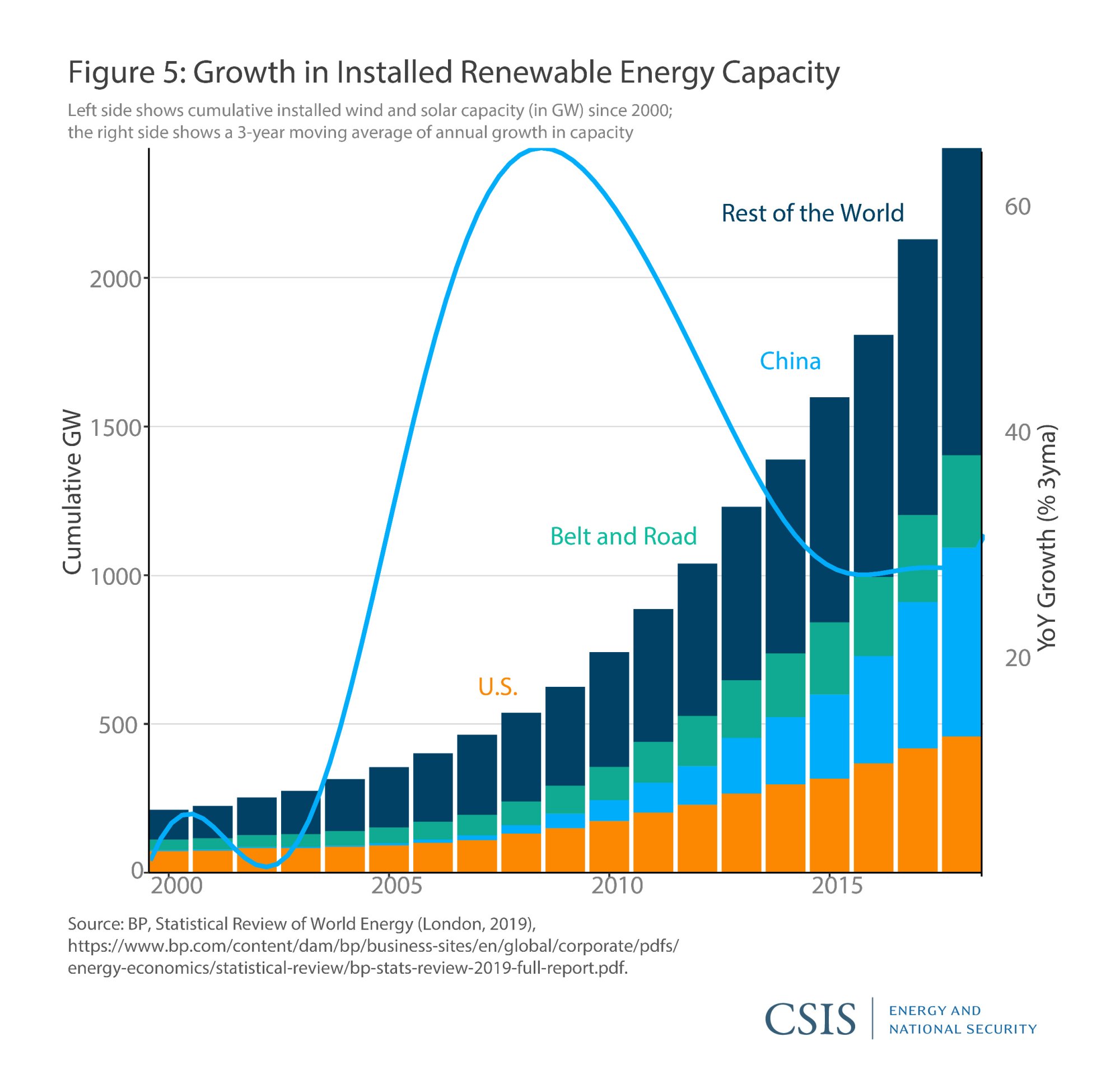

Of course, China is the world’s largest emitter, and the extent to which it focuses on environmental sustainability at home will determine its ability to create a green BRI. While China has had some success in recent years in moving toward a more environmentally sustainable energy sector, it still has a long way to go. China announced in an agreement with the United States that its emissions would peak by 2030, and according to its representative to the UNFCCC, met its 2020 carbon intensity target three years ahead of schedule. The Chinese government has also issued a series of policies over the last decade to spur investment in clean energy, leading to extraordinary growth in renewable energy capacity (Figure 5). China now has the world’s largest installed capacity of wind, solar, and hydropower, including approximately 30 percent of the world’s installed solar PV capacity, and is set to become the “world’s renewable energy superpower,” according to a recent report.

While China has had some success in recent years in moving toward a more environmentally sustainable energy sector, it still has a long way to go.

Unfortunately, despite success in meeting its own pledges, Climate Action Tracker rates these targets as “Highly insufficient” in limiting global warming below two degrees Celsius, let alone 1.5 degrees. Its emissions trajectory will ultimately depend on the speed at which it can restructure its economy, which continues to be delayed. In particular, with over 60 percent of energy demand still in coal, it remains unlikely that China will transition in time for the world to meet its Paris Agreement targets. According to the IEA, if China were to follow through on its proposed policies, it could switch from 60 percent coal-fired electricity capacity today to 60 percent low-carbon capacity by just 2040—an unprecedented shift. China’s investment profile will presumably reflect its changing economy and energy profile, however there are several policy options it could implement in the meantime to accelerate how fast its flagship initiative goes green.

While the commitment to ending perceptions of “debt-trap diplomacy” and environmental negligence appear credible enough at the highest level, Chinese authorities continue to face difficulties in reigning in the multitude of actors working within its Belt and Road framework. The Chinese have a famous proverb, “Shan gao, huangdi yuan (山高皇帝远),” which translates as “The mountains are high, and the emperor is far away.” In other words, central authorities are perceived to have little influence over local affairs.

In foreign investment especially, authority is fragmented among a wide array of overlapping agencies, ministries, bureaus, regulators, and state-linked economic actors, making it extremely difficult for central authorities to set clear goals or guarantee sustainable environmental outcomes. Numerous agencies have jurisdiction over different components of foreign investment, with the State Council being the highest authority, approving all overseas investments over $2 billion. Other important policymaking institutions include the People’s Bank of China (PBoC), the Ministry of Finance, the National Development and Reform Commission, the Ministry of Environmental Protection (MEP), and the China Banking Regulatory Commission.

Importantly, none of these agencies have issued a formal law regulating environmental protection in China’s overseas investments. The only requirement is that Chinese companies comply with the host country’s regulations. For example, prior to the more recent attempts at bringing environmental concerns into the BRI, the most comprehensive document was the 2013 Ministry of Commerce and MEP’s “Environmental Protection Guidelines for Overseas Investment Partnerships”—a set of voluntary guidelines with little demonstrable impact on investment. For example, in a 2017 interview, a Chinese environmental lawyer and now head of China Accountability Watch stated that:

“There’s currently no single law overseeing the environmental and social impact of Chinese companies working overseas, just regulations scattered amongst administrative regulations and ministerial rules . . .NGOs and communities in host nations have a confused understanding of this—they don’t see that these documents are distinct from Chinese law.”

In other words, Chinese authorities largely leave it up to local investors or recipient countries to determine their own environmental standards, entities who often do not have particularly positive track records, significant experience with environmental policy, or strong incentives to improve in the future.

In a recent article for the journal Climate Policy, several academics called on China to revise this “host country standard” principle such that China aligns its foreign investment policies with its stated adherence to the Paris Agreement. The authors note that existing voluntary commitments are insufficient, with no recorded instances of companies being penalized by Chinese authorities for failing to adhere to the standards. Instead, they argue, China’s State Council should follow the lead of MDBs and introduce a “best nation standard principle,” where the more stringent standard between China and the host country is adopted and enforced.

The extent to which China successfully manages to green the BRI will be based on its ability to either add teeth to its own foreign investment regime or facilitate improved environmental standards in host countries. While new multilateral institutions may help with the latter, these initiatives will only be successful if the lead to concrete changes in China’s actions like adopting a “best nation

standard” or adding additional enforcement mechanisms to its many voluntary guidelines.

At the second Belt and Road Forum in April 2019, China announced a series of initiatives designed to usher in a new phase of the BRI that would address these criticisms. Several of these are designed to improve both the environmental impact of overseas BRI investments and the international reputation of the BRI more generally.

The extent to which China successfully manages to green the BRI will be based on its ability to either add teeth to its own foreign investment regime or facilitate improved environmental standards in host countries.

Two initiatives that are both potentially significant and indicative of broader challenges facing Chinese authorities are the BRI International Green Development Coalition and the Green Investment Principles for the Belt and Road Development. The BRI International Green Development Coalition reflects a recent trend away from the bilateral deals that defined the BRI in its first phase and toward a multilateral approach that is consistent with China’s evolving institutional statecraft and global leadership ambitions—though it is also indicative of China’s preference for a form of shallow multilateralism that fails to place obligations on its participants, leading to both free riding and duplication of existing efforts. Meanwhile, although the Green Investment Principles for the Belt and Road Development are an important step for China’s increasingly global financial footprint, they are an example of yet more voluntary guidelines that help accelerate existing positive trends without inhibiting the negative ones.

The extent to which China successfully manages to green the BRI will be based on its ability to either add teeth to its own foreign investment regime or facilitate improved environmental standards in host countries.

These initiatives join an explosion of multilateral institutions established under the BRI umbrella, many of which have focused explicitly on environmental issues. The sheer range of initiatives further indicates how seriously Chinese authorities are taking environmental issues in phase two of the BRI—or at least, how seriously they are taking its effects on China’s reputation. At the second BRI forum alone, China announced the:

These join a long list of existing environmental initiatives set up under the BRI, including the:

Unfortunately, the opaque or vague nature of many of these new institutions makes it very difficult to analyze their additional impact over existing actions. It seems likely that several of these initiatives suffer from a self-selection problem where only those countries already taking steps to improve sustainability are joining. Furthermore, these initiatives generally contain few, if any, provisions to deter free riding by participants and often duplicate, rather than complement, existing structures.

These institutions can still be useful additions to the global sustainability effort if they accelerate existing actions or provide coordination mechanisms for sharing best practices. However, to truly green the BRI, these institutions must also address the worst offenders and stamp out the poorest practices. So far, there is little evidence of this taking place.

Indeed, one of the opportunities presented to the international community by these new institutions is the potential to challenge Chinese authorities to prove or quantify their impact. As the BRI moves away from the opaque bilateral deals of its early years to more transparent multilateral forums, NGOs and motivated countries can place more pressure than ever on China to show both what is being done that otherwise would not be and which poor practices are being stamped out that would otherwise survive.

Though announced in May 2017, the BRI International Green Development Coalition only met for the first time at the second BRI forum, which reflects the slow pace at which it appears to be evolving and the extent to which its development is driven by outside actors. The coalition is co-initiated by the UN Environment Programme and the Chinese Ministry of Ecology and Environment. It now has more than 120 participating organizations from 60 countries and environment ministries from 25 BRI countries. According to the UN, it will “bring together the environmental expertise of all partners to ensure that the Belt and Road brings long-term green and sustainable development to all concerned countries in support of the 2030 Agenda for Sustainable Development.”

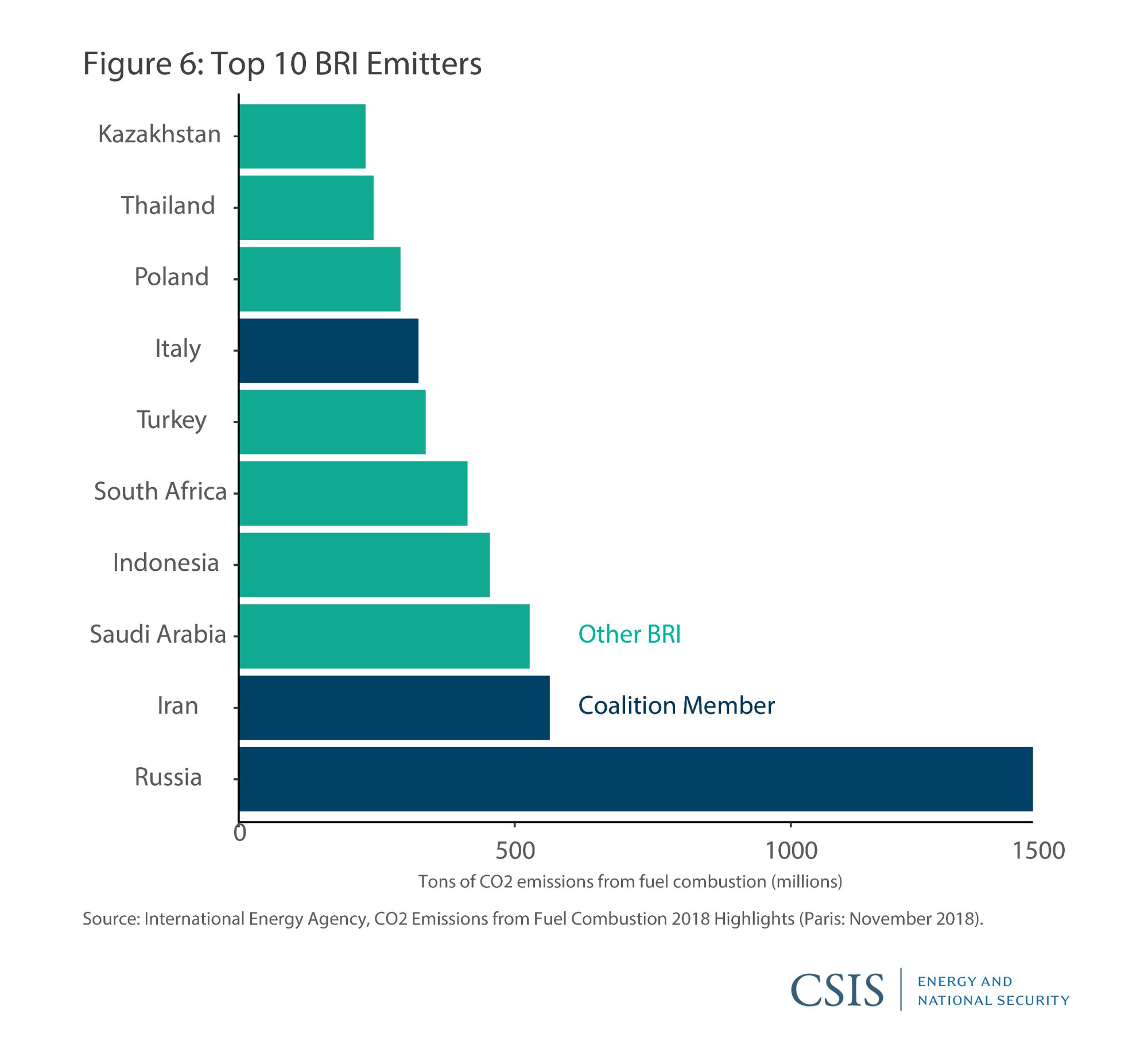

While the coalition includes several important players, only three of the top 10 greenhouse gas emitters in the BRI have so far opted to join (Figure 6). If the coalition is to seriously take on its ambitious goals, it will need to expand to include countries like Saudi Arabia and Indonesia without giving up what, if any, influence it has over members’ actions.

The coalition has three mandates—act as (1) a platform for policy dialogue, (2) a knowledge and information platform, and (3) a platform for green technology exchange—and nine Thematic Partnerships, which are each co-led by one Chinese and one foreign partner:

More recently, in June 2019, the first Coordination Meeting of the coalition was held in Hangzhou and chaired by the World Resources Institute. The coalition is working on two-year and five-year plans that will map out detailed measures and solutions and is planning to launch its pilot projects in the near future. The Thematic Partnership on Climate Change Governance and Green Transformation has also met twice this year and will be participating in upcoming UN Climate Summits.

One challenge for the coalition will be negotiating among its highly diverse members. The coalition includes some of the world’s fastest-growing CO2 emitters and countries with the worst environmental track records, as well as better performing countries like Finland, Italy, and Israel.

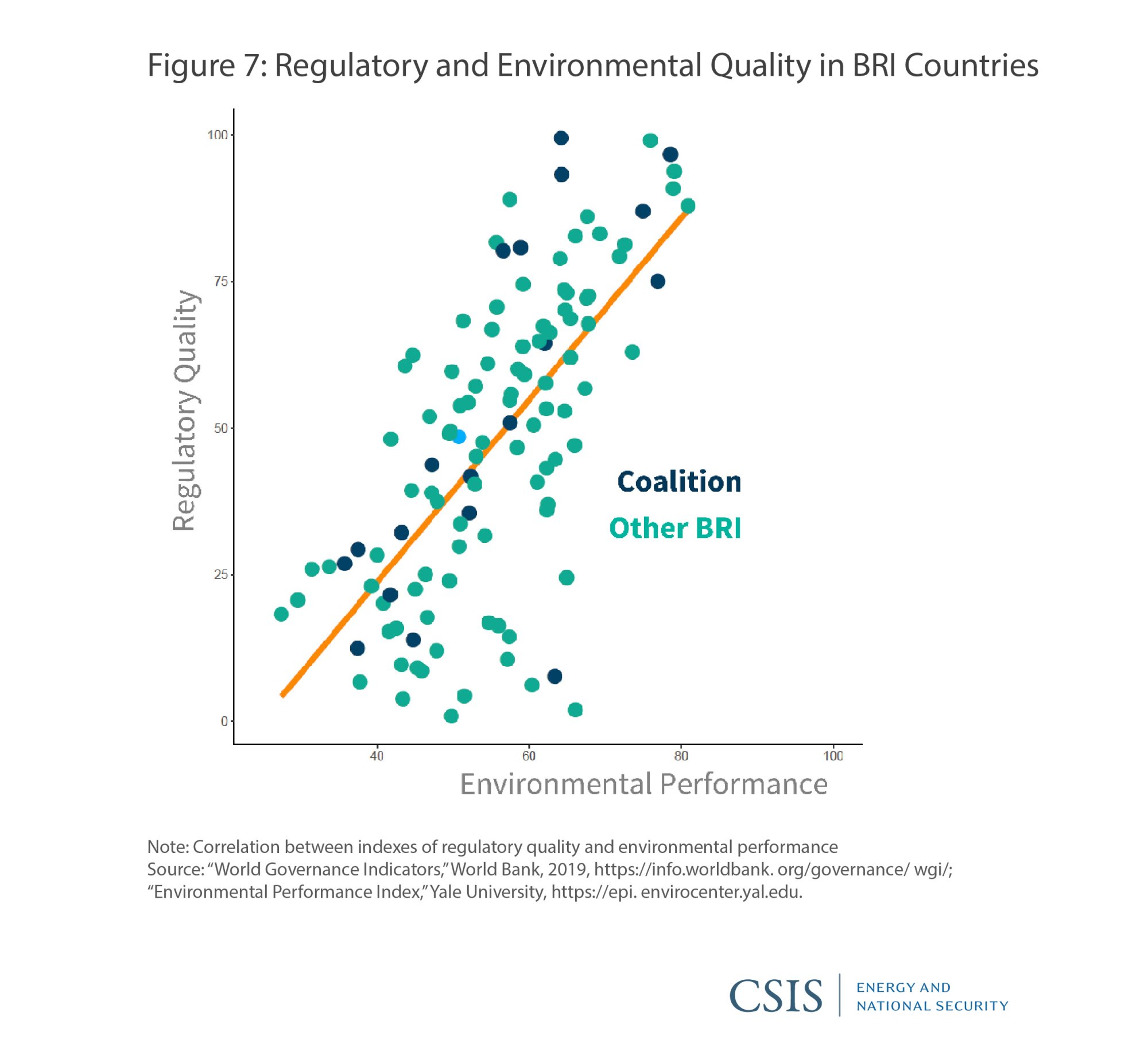

Given the way China’s foreign investment regime relies largely on host countries’ environmental standards to bring its public and private investors into line, the coalition will be most effective if it can improve its own members’ regulatory standards. Unsurprisingly, the correlation between regulatory quality and environmental performance is quite strong (Figure 7), and coalition members are just as diverse in the quality of their regulations as they are in their environmental performance. The few statements released by the coalition so far express a promising focus on sharing best practices that hopefully can enable some of its worst offenders to catch up.

The area in which China has demonstrated the strongest commitment and appears perhaps best poised to exert its influence is in green finance, as demonstrated by the Green Investment Principles for Belt and Road Development. Since China simply cannot afford to single-handedly finance all of Eurasia’s infrastructure; it needs to attract more outside investment to the BRI and now wants to share the financial and reputational risks. Classifying projects as green is one promising way to do this, prompting China to invest considerable resources into the effort.

Incorporating green finance into the BRI follows more than a decade of efforts by Chinese authorities to green its financial system and become a global leader in this space. In 2007, the CBRC and PBoC jointly issued a green credit policy which encouraged banks to give credit support to green industries. This was followed up with a set of Green Credit Guidelines in 2012. Other initiatives include a pilot carbon allowance trading program, launched by the NDRC in 2011, and the subsequent rollout of a national emissions trading system in 2017. The PBoC was the world’s first central bank to issue guidelines for establishing a green financial system in 2016 and was a founding member of the Central Banks and Supervisors Network for Greening the Financial System. The Chinese government also officially introduced green finance into the G20 agenda for the first time during its 2016 host year. Importantly, by 2020, all listed companies in China will have to annually disclose their environmental plans and spending—the only major economy with such requirements in place.

These policies have seen a rapid expansion of green finance in China, including large growth in the green bond market. The world’s first green bond was issued in 2007 by the European Investment Bank, and the green bond market has grown in the years since to become a $167 billion annual market by 2018. China is the world’s second largest issuer of green bonds, with its $31 billion issuance in 2018 comprising nearly 20 percent of the global market. Importantly for the future of this nascent asset class, Chinese green bonds have outperformed central government bonds and the aggregate overall bond market, bolstering a claim often made globally that green financing need not come at the expense of returns.

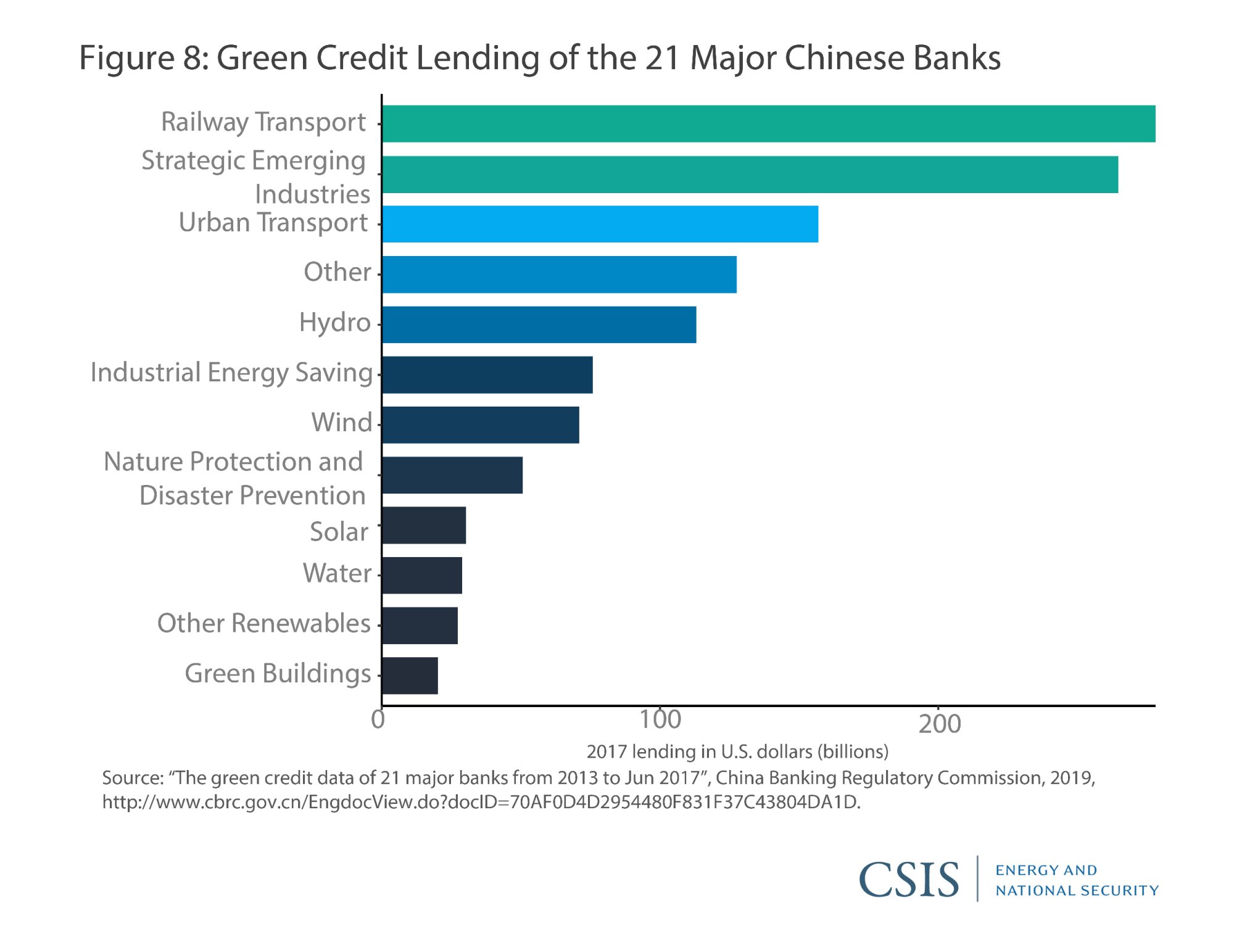

Green credit has also been an important component of the PBoC’s strategy for a green financial system, with almost 10 percent of outstanding loans in 2017 going toward green projects —which is significant given how much larger bank lending is than bond issuances. Additionally, there remains significant scope for this figure to increase, with the China Council for International Cooperation on Environment and Development recommending a target of 20 percent of total loan volume. The majority of green credit lending in China goes toward transport infrastructure and the “Strategic Emerging Industries” of new conservation, energy, and vehicle manufacturing (Figure 8), consistent with China’s strategy of state-led development in a green economy.

There are also reasons to be skeptical of the growth in Chinese green finance, however. For example, the definition of what counts as “green” or “sustainable” in these investments can be loose or vary from country to country.

For example, green bonds in China can be used to finance some types of coal investments and large hydro projects—it is estimated that roughly 23 percent of China’s green bond proceeds went to projects that would not meet international standards. A particularly controversial practice has been to use green bonds proceeds to replace small, inefficient coal plants with larger, more efficient ones. While this reduces short-term emissions, it can lock in a dirty emissions profile for decades. In the first half of 2019 alone, roughly $1.1 billion in green bonds was issued by 13 coal projects.

The Green Investment Principles for Belt and Road Development aim to address the problem of inconsistent standards and definitions of green financing across BRI countries and embed principles of sustainable development across all asset classes, financial products, and project phases. The principles were drafted by a number of organizations, including the World Economic Forum, UNPRI, Belt and Road Bankers Roundtable, and the Paulson Institute, and are based on existing principles, such as the Equator Principles, the Principles for Responsible Investment, and the Environmental Risk Management Initiative for China’s Overseas Investment.

The principles have been signed by 28 firms, are the culmination of a joint exercise between the City of London Corporation’s Green Finance Initiative and China’s Green Finance Committee, and are supported financially by the UK government through the China-UK PACT program (Partnering for Accelerated Climate Transitions). They were first published by the UK-China Green Finance Taskforce and are a voluntary commitment that the taskforce “believes will ensure climate considerations and green finance are embedded along the Belt and Road.”

The problem, as with most sustainable initiatives in China’s foreign investment regime, is that these principles remain just a voluntary commitment. There is no reason to believe, for example, that these principles will do anything to stop coal projects from issuing green bonds by operating outside of the principles. As such, they encounter the same difficulties as described above when encountering low standards of environmental regulation in host countries: there are few incentives for the worst offenders to eliminate their poor practices.

Chinese authorities need to back up their rhetoric with action. It is not enough to promote best practices without altering problematic behavior, nor is it enough to simply provide spaces for discussion without empowering members to act. China has laid out an ambitious series of initiatives that undoubtedly has the potential to improve the environmental footprint of the BRI, but more can be done. There are at least five areas where international actors can use the push for a “Belt and Road 2.0” to improve its social and environmental footprint:

China’s latest push to improve the quality of BRI projects stems largely out of concerns over its reputation on the global stage. Many countries are looking to China to be a global leader on environmental issues—particularly on the climate crisis—and these expectations should be laid out. For example, it should be made clear to China that it is no longer enough just to add more environmental forums or invest in more clean energy; it also needs to accept fewer damaging bilateral deals and invest in fewer fossil fuel projects.

Existing international financial institutions have already spent considerable time and resources on their environmental standards and best practices, which China should try to emulate within the BRI wherever possible. As early members of the AIIB pushed for the BRI to adhere to global norms and partner with well-established institutions, so too can members of the Green Development Coalition and other BRI multilateral forums. In particular, China should move to a “best nation standard principle,” like the MDBs, which would eliminate the excuse of lax host country regulations and export China’s domestic regulatory progress overseas. Chinese policy banks could even follow the lead of international financial institutions such as the World Bank and set up environmental departments to oversee environmental issues.

As long as China’s outbound investors are constrained only by host country regulations, there are few reasons for them to adhere to the lofty rhetoric of central authorities. For example, to prevent corruption in BRI projects, the Central Commission for Discipline Inspection recently announced it would embed officers in BRI countries, extending its mandate for the first time outside of China’s borders. While one could imagine a similar proposal for environmental concerns, there are options that do not include sending government agents into foreign countries, such as increasing the transparency of lending and terms of BRI deals. Another option could be expanding the Ministry of Commerce’s list of “encouraged sectors and negative list” to include green industries and exclude sectors with the largest carbon footprints, like coal.

As long as China’s investors only adhere to host country regulations, the most direct way of improving their practices would of course be for those countries to improve their environmental standards. MDBs, international financial institutions, and international allies should be providing technical assistance and incentives wherever possible. While it is easy to blame the Chinese government for investments with the BRI label, the reality is that there are simply too many projects for it to monitor, and at some point, countries have to be responsible for their decisions.

Currently, environmental concerns are only present at the highest level before they slowly filter out as parties with less and less interest in sustainability take over. Just as listed companies are going to be required to disclose environmental plans and spending, all BRI projects should require early-stage environmental assessment procedures to help inform future green investors. A recent World Bank working paper spells out in some detail how environmental assessments are particularly well-suited to reduce environmental risks. They go on to note how the insurance giant, Sinosure, which has to insure every BRI project, could require companies to provide environmental impact assessment studies as a prerequisite for insurance, effectively ensuring that no project can avoid considering its broader implications.

Lachlan Carey is an associate fellow with the Energy and National Security Program at the Center for Strategic and International Studies (CSIS) in Washington, D.C. Sarah Ladislaw is the senior vice president and director and senior fellow of the CSIS Energy and National Security Program.

This brief is made possible by the generous support of the Hewlett Foundation.

CSIS Briefs are produced by the Center for Strategic and International Studies (CSIS), a private, tax-exempt institution focusing on international public policy issues. Its research is nonpartisan and nonproprietary. CSIS does not take specific policy positions. Accordingly, all views, positions, and conclusions expressed in this publication should be understood to be solely those of the author(s).

© 2019 by the Center for Strategic and International Studies. All rights reserved.

Please consult the PDF for references.