Powering Maritime Dominance: A Conversation with ADM William Houston, USN

April 22, 2026 • 10:00 – 11:00 am EDT

Hosted by Defense and Security

Photo: UPI/Bettmann/Getty Images

The founders of NATO understood that durable security requires durable economic ties. Article 2 of the North Atlantic Treaty—rarely quoted in today’s burden-sharing debates—commits members to “promote conditions of stability and well-being” and to “encourage economic collaboration.” The alliance was designed as an integrated political, economic, and security architecture from the outset.

That founding logic matters now because the burden-sharing framing that dominates current debates captures only one side of the ledger: tallying what members spend and ignoring what large economies such as the United States gain. Today, with Washington seemingly sleepwalking toward a divorce with NATO, it is risking billions in trade, supply chain integration, and institutional trust built around U.S. platforms and standards, around which NATO’s standards are based. This is a cost too large to ignore.

In “Beyond Security: The Trade Implications of Joining NATO,” Karen Jackson and Oleksandr Shepotylo combine structural gravity methods with staggered difference-in-differences estimation to identify the causal effect of NATO membership on bilateral trade flows. The data covers 75 years (1948–2022) and over 5,500 products at the Harmonized System 6 level of disaggregation.

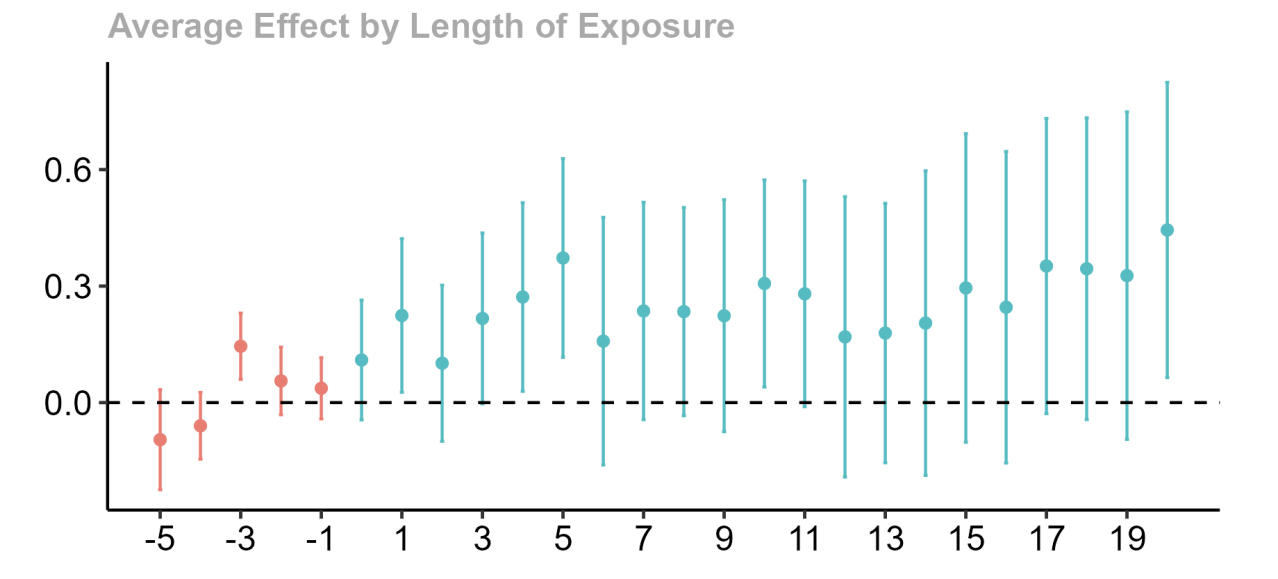

The headline result is striking: NATO membership raises bilateral trade between members by 12–27 percent in the long run, even after accounting for EU membership, preferential trade agreements, and other defense pacts. The gains are not immediate; they build over five-to-ten years and compound further, often exceeding 0.5 log points (roughly a 65 percent trade increase) at 15–20 years of membership as is shown in Figure 1.

Figure 1: Changes in Trade Following NATO Enlargement

Source: Karen Jackson and Oleksandr Shepotylo, “Beyond Security: The Trade Implications of Joining Nato” (April 2026), https://papers.ssrn.com/sol3/papers.cfm?abstract_id=6613399.

Figure Note: NATO enlargement is associated with higher trade, and the gains tend to grow over time. The figure shows estimated changes in trade following NATO enlargement. Points show the estimated effect, and vertical lines show the uncertainty range around each estimate. Overall, the results suggest that NATO enlargement was followed by rising trade among member countries, with effects that build gradually rather than appearing all at once.

A companion paper, “Political Alliances and Trade: Europe in a Polarized World,” extends the analysis to scenario modelling. It shows that NATO expansion generates trade and welfare gains large enough to offset the cost of additional defense spending, and that U.S. withdrawal or broader NATO disintegration imposes meaningful economic losses on all members, including the United States itself.

The trade premium is not simply a correlation with Western prosperity. Three mutually reinforcing mechanisms explain why the institutional architecture of the alliance generates real economic returns.

The research also identifies an anticipation effect: Trade begins rising approximately three years before formal accession, as candidate countries realign institutions and standards. This means that the benefits of membership are more than a signature on a piece of paper. Even if the United States does not formally withdraw, signaling potential withdrawal from or renunciation of the core obligations of the agreement likely imposes costs well before any formal exit.

This is not a diffuse story about marginally more trade across the board. The NATO premium is concentrated precisely in the sectors that define technological leadership and strategic competitiveness for the twenty-first century. Table 1 shows the estimated trade premium by sector, converted into approximate percentage terms for readability.

Computers, sensors, aerospace, and electronics sit at the intersection of military capability, advanced manufacturing, and the next generation of great power technological competition. If NATO weakens, the economic damage falls disproportionately on the very sectors Washington most wants to lead in, and on which U.S. technology has historically set the global standard.

The burden-sharing critique runs as follows: The United States contributes a disproportionate share of NATO’s defense costs, therefore it is subsidizing European security. The economics run the other way.

The United States, as the alliance’s central industrial node, has the most to lose economically from a dissolution of the alliance. As mentioned, U.S. platforms—including F-35s, Patriot systems, and command, control, communications, computers, intelligence, surveillance and reconnaissance architecture—provide the standards around which allied procurement, supply chains, and interoperability are organized. Allied defense spending, when directed at U.S. systems, generates demand for U.S. aerospace, electronics, and materials firms. The F-35 program illustrates the logic: A distributed manufacturing ecosystem spanning allied nations, centered on U.S. platforms, feeding components and capabilities back into U.S. production. Allied procurement augments demand for U.S. goods, produces jobs for American workers, and in many cases provides the scale necessary for some of the most advanced weapon systems in the world.

The scenario modelling in “Political Alliances and Trade: Europe in a Polarized World” explicitly spells out the cost of exit. A U.S. exit from NATO is predicted to generate a 16.1 percent fall in U.S. exports and a 0.41 percent decline in U.S. GDP, roughly $100 billion in lost annual output at current levels. These are model-based counterfactuals, not forecasts. But the inference is hard to avoid: if building into the alliance's institutional trust architecture takes 5–20 years to generate full trade benefits, then disrupting that architecture means losing those benefits, and rebuilding them would likely take a generation.

While formally leaving NATO would require an act of Congress, the trust necessary to support the alliance is already fraying and partners are responding in real time. The European Union’s €800 billion ReArm Europe plan explicitly prioritizes procurement from European manufacturers.

Denmark may provide the sharpest example. In 2025, facing the largest arms procurement decision in its history, Denmark chose the French-Italian SAMP/T air defense system over the U.S. Patriot. While the decision also included discussion of the likely delay in procurement of U.S. made systems, accompanying public comments from Danish officials speak volumes:

“Buying American weapons is a security risk that we cannot run.”

—SørenRasmus Jarlov, Chairman, Danish Parliamentary Defense Committee, March 2025

Denmark is shifting away from U.S. aerospace, sensors, and electronics—precisely the sectors the research identifies as enjoying the largest NATO trade premium. One could argue that the mechanism the research identifies is currently playing out in real procurement decisions.

For NATO’s frontline states, those with the most direct exposure to Russian aggression and the most acute interest in a credible U.S. commitment, the instinct remains to preserve the transatlantic relationship.

“We need to support our national and European defense industries, while also keeping and nourishing transatlantic bonds, which means buying American weapons.”

—Dovilė Šakaliėnė, Lithuanian Defence Minister, 2025

The above sentiment—shared by Poland, the Baltic states, and others on NATO’s eastern flank—is the alliance’s most important remaining asset. The demand is still there. The institutional memory is still there, and the research shows that trade and investment relationships, once established, are durable.

Yet the erosion of trust is real and substantial. In another frontline NATO member, Finland, trust in the U.S. has fallen to just 4 percent, approximately the same as Fins’ trust in Russia and China.

The same research also makes clear that rebuilding that lost trust and the economic gains it creates is a slow process. The benefits of membership compound over 15-to-20-year horizons. The costs of disruption compound in the same way. Each additional year of perceived unreliability pushes farther out the timeline for recovering the alliance’s full economic benefits.

NATO was designed to do more than provide security. It built deep economic integration that has become one of its least appreciated strengths. The economic gains are large, durable, and, in many cases, effectively self-financing relative to the costs of membership. As the alliance’s hub, the United States has benefited disproportionally from this economic integration and would see some of the steepest losses should the alliance dissolve.

Europe is already investing in alternatives and building stronger indigenous defense capacity. Once procurement networks, standards, and supplier relationships begin to reorient away from the United States, they will not be easy to win back. NATO is therefore not only a defense alliance to be preserved for security reasons. It is a long-built economic asset. And like any asset accumulated over 75 years, it can be lost much faster than it was created.

Philip A. Luck is director of the Economics Program and Scholl Chair in International Business at the Center for Strategic and International Studies (CSIS). Karen Jackson is a reader in economics at the University of Westminster. Oleksandr Shepotylo is a reader and senior lecturer at Aston Business School.