Unlocking Development Capital Through Insurance | The Futures Summit

April 16, 2026 • 9:00 – 9:30 am EDT

Hosted by Global Development

Photo: ALEXANDER NEMENOV/AFP/Getty Images

The prospect of conflict between Ukraine and Russia has the oil market on edge. In a tight market, any significant disruptions could send prices well above $100 per barrel. Already concerned about high energy prices, the White House seems unlikely to impose sanctions that would directly target Russian exports of crude or petroleum products.

Q1: What is Russia’s role in the global oil market?

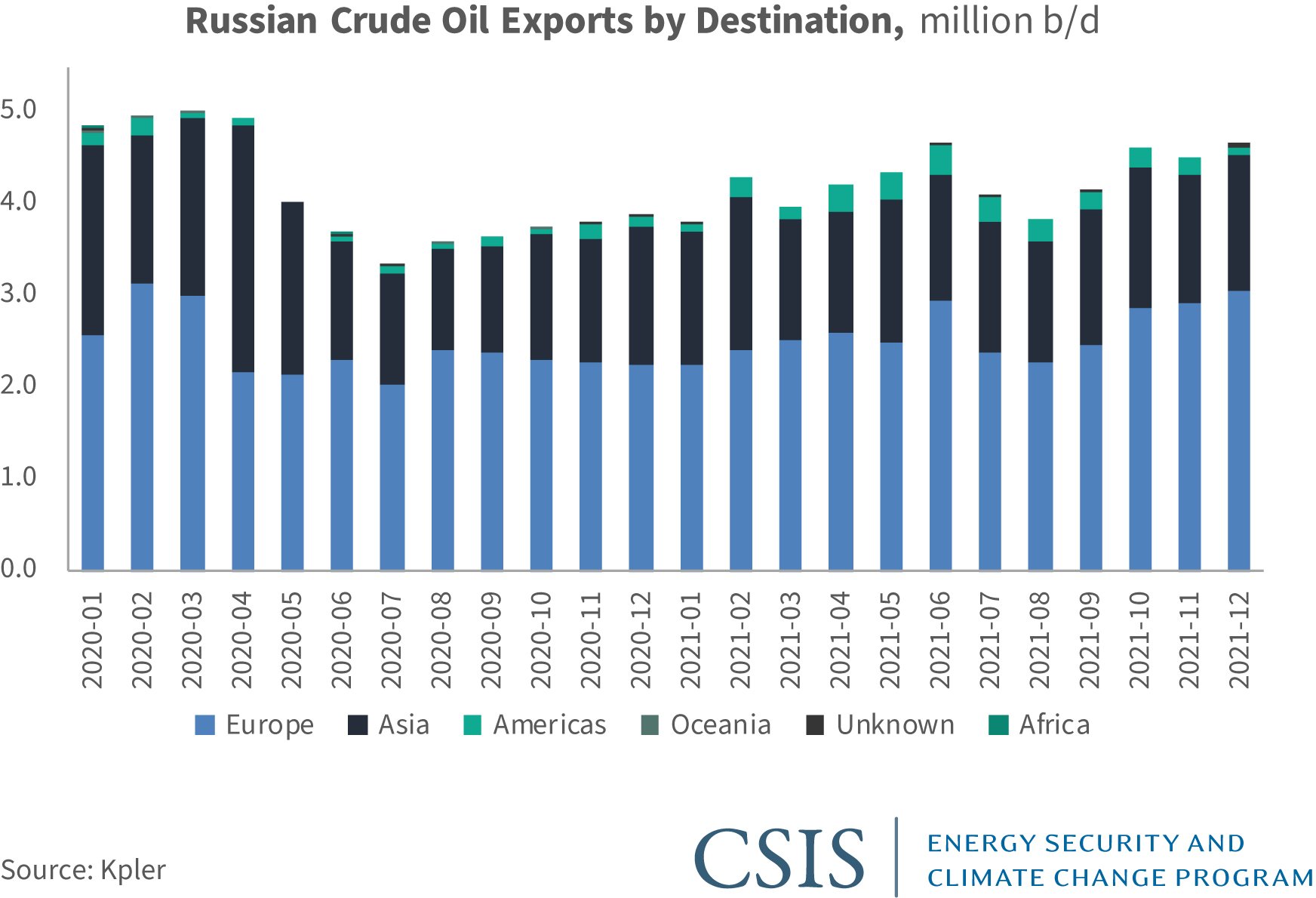

A1: Russia is one of the world’s three largest oil producers, along with the United States and Saudi Arabia, and plays a central role in OPEC+ (the Organization of the Petroleum Exporting Countries and allied producers). Russia’s December crude output was about 10 million barrels per day (b/d), and its total liquids production (including condensate, which is exempt from OPEC quotas) was nearly 10.9 million b/d. Russia exported about 4.3 million b/d in crude last year, equivalent to 4.5 percent of global demand, including 2.6 million b/d to Europe via pipeline and seaborne exports. It also exported about 1.6 million b/d in refined products to Europe. The Druzhba pipeline sends crude supplies to Belarus, Poland, and Germany through a northern arm and Slovakia, Hungary, and the Czech Republic through a southern arm that transits Ukraine. Russia also exported about 1.4 million b/d of crude oil to Asia in 2021, via the East Siberia Pacific Ocean (ESPO) pipeline system and waterborne exports. Russia’s exports to the United States have grown in the past three years, with crude and product exports reaching a monthly average of 705,000 b/d in the first 10 months of 2021. U.S. refineries import Russian crudes including Urals and ESPO blend as well as fuel oil and feedstocks for blending purposes.

Under the OPEC+ agreement, Russia is slated to raise crude output by about 100,000 b/d each month until it reaches 10.5 million b/d in May, equivalent to its pre-Covid output. But its production increases seem to be running out of steam. In December the country produced below its OPEC+ target for the first time since last spring, and there are doubts that Russia can raise output much beyond 10.5 million b/d. Its February OPEC+ allocation is 10.23 million b/d.

Q2: How is the market reacting to Russia-Ukraine tensions?

A2: The prospect of supply disruptions—however unlikely—is fueling bullish sentiment. The oil demand recovery from Covid-19 has been stronger than many expected. Supplies have not kept pace as OPEC+ is still unwinding its production cuts and U.S. shale companies continue to take a cautious approach to spending. The market is focusing on concerns about low spare capacity and inventories, as well as depressed investment by the global oil and gas industry since 2015. The market is also in steep backwardation, with prompt prices exceeding prices for future delivery, which indicates strong demand from refiners and encourages inventory draws. Brent crude surpassed $90 per barrel last week for the first time since 2014, and many banks and traders believe $100 per barrel prices are in sight. OPEC+ continues to fall short of its production targets, with countries such as Nigeria, Angola, and Malaysia producing below their allocations each month. Rather than adding 400,000 b/d to the market each month, recent OPEC+ increases have been in the range of 250,000 b/d. The market is worried that few countries—including Russia—have spare capacity that can help absorb shocks. It is always difficult to separate signal from noise in terms of geopolitical risk in the oil market. But after the extreme gas and electricity price increases in Europe in recent months and recent oil outages in Libya and Kazakhstan, the market is attuned to supply disruptions. Low-probability, high-risk events like war in Ukraine or sanctions on Russian exports have an outsized impact in a tight market.

Q3: Could the oil market adjust to a big disruption of Russian exports?

A3: Any sizeable disruption would have a severe impact. Oil volumes transported through Ukraine fell from 585,000 b/d in 2009 to just 255,000 b/d last year, after the construction of several new pipelines and bypass pipelines, placing fewer barrels directly at risk. But in the event of a pipeline supply cut, sabotage, or sanctions that limit exports, European refiners would have to scramble for alternatives to Urals, a medium sour crude blend. It is possible that Middle Eastern exporters of sour crude such as Saudi Arabia, Iraq, and Kuwait could export more volumes, although most of their capacity is locked up in term cargoes. Some refiners may be able to substitute lighter barrels from Norway, the United States, or West Africa, perhaps blending them with sour crude. Refiners in Asia looking for alternatives to ESPO blend could also look to the Middle East for medium sour or light sour barrels. But the bottom line is that alternatives are scarce in a tight market, and prices would have to increase. OPEC+ is scheduled to hold its next monthly meeting on February 2, but for now the group seems unlikely to alter its plan to keep adding 400,000 b/d to the market each month.

Q4: Are sanctions on Russian oil exports on the table?

A4: In a media briefing last week, White House senior officials suggested that in the event of a Russian invasion of Ukraine, “the gradualism of the past is out, and this time we’ll start at the top of the escalation ladder and stay there.” Still, they focused on potential financial sector sanctions and export controls, mentioning artificial intelligence and quantum computing, as well as defense and aerospace technology. It is possible that future sanctions or export controls could target the oilfield services sector in Russia, preventing domestic producers and their joint venture partners from accessing equipment and services. The White House could also try to freeze international assets of oil companies or their executives. But at this stage, it seems unlikely that sanctions will directly target crude or petroleum product exports, given the risks to European energy security and the global economy. Instead, energy-related measures are more likely to target future gas projects and longer-term investment priorities and growth areas. This strategy would have some parallels with the last major round of financial sector and energy sanctions on Russia in 2014, which sought to prevent Russia from developing its shale oil, Arctic, and deepwater resources.

Q5: In the event of a major supply disruption, what could the United States do?

A5: The United States would likely respond by releasing oil from the Strategic Petroleum Reserve (SPR), perhaps in a coordinated emergency release with other countries. Last November the Biden administration announced it would make 50 million barrels of the SPR available through exchanges (32 million barrels) and accelerated sales of reserves (18 million barrels). It has now released almost 40 million barrels via a December sale and several exchanges, announcing the most recent awards last week. The SPR announcement last fall arguably cooled the market after a rapid run-up in in prices, but the impact of future SPR sales or exchanges may be limited. The White House will probably continue to urge other oil producers to maximize output, including OPEC+. But any sizeable disruptions from Russia would underscore the need for continued investment in exploration and production in the United States as well. Renewed concerns over energy security suggest it is time to recalibrate the White House’s message to better balance long-term climate and energy objectives with short-term needs.

Ben Cahill is a senior fellow with the Energy Security and Climate Change Program at the Center for Strategic and International Studies in Washington, D.C.

Critical Questions is produced by the Center for Strategic and International Studies (CSIS), a private, tax-exempt institution focusing on international public policy issues. Its research is nonpartisan and nonproprietary. CSIS does not take specific policy positions. Accordingly, all views, positions, and conclusions expressed in this publication should be understood to be solely those of the author(s).

© 2022 by the Center for Strategic and International Studies. All rights reserved.