U.S. Navy Fighting Instructions with the Chief of Naval Operations

March 31, 2026 • 1:00 – 2:00 pm EDT

Hosted by Defense and Security

Photo: Carsten Koall/Getty Images

1990: The Year That Was

The #1 box office movie was “Ghost.” The San Francisco 49ers won the Super Bowl that January, the Dallas Cowboys were about to win three of the next four, and the New England Patriots had yet to win any. Worries about CO 2 emissions and climate change were not yet mainstream. Yes, there were concerns about the environmental impacts of burning fossil fuels, but they generally related to “traditional” pollutants like SO 2, NOx, and particulate matter. In fact, much progress had been made in dealing with smog, the most visible form of fossil fuel pollution, and the United States began that year with a successful effort to address acid rain (which was largely caused by emissions from coal power plants and vehicles).

When it came to CO2, the world was emitting 2.331 million tonnes of CO2 (MtCO2) for every million tonnes of oil equivalent (Mtoe) that it used. Total global primary energy demand in 1990 was 8774 Mtoe (about four times current U.S. levels) and the world emitted 20.448 gigatonnes (Gt) of CO2 that year. At the time, however, few were managing these emissions. While scientists, governments, and others had begun to turn some attention to the potential harm of greenhouse gas emissions and climate change (President George H. W. Bush highlighted this concern in his 1990 Economic Report), concrete policy action in this area was still minimal. After all, the Earth Summit and adoption of the UN Framework Convention on Climate Change were still 2 years away, the Kyoto Protocol (the first major international emissions reduction agreement) was 7 years away, and the European Union’s emissions trading scheme (the archetypal carbon trading system) would take another 15 years to be launched. Renewables were a part of our energy mix, but not for climate change reasons. Hydropower, for example, was already a major provider of electricity, generating 18 percent of total global power production that year.

Climate Concerns and the Renewables Revolution

We have learned a great deal since 1990 about the damage that too much CO 2 can wreak and the perils of climate change, and we also know how to address it. The key is to replace fossil fuel use with renewables and to deploy energy efficiency, nuclear power, and carbon capture and storage (CCS). When it comes to renewables, there has been much good news. Year after year, we are installing more and more renewables power generation: in 2016, renewables capacity additions topped 160 gigawatts (GW) globally, while solar photovoltaics and wind alone (126 GW) exceeded coal and gas additions. Renewables prices have also been dropping dramatically, with the price of solar and on-shore wind now competitive and at times even cheaper than fossil fuel power generation. Renewables, the key to fighting climate change, have come to life.

Stuck in the Past

But where do we stand today as compared to 1990 with this increased awareness worldwide of the climate change threat and the progress we have seen in deploying renewables? Sadly, if we look at the carbon content of our energy mix, we have yet to see any improvement. This is illustrated by analyzing the carbon intensity of our energy use, namely how much CO 2 is being emitted per unit of energy that we use. Based on estimates of emissions and energy demand recently released by the International Energy Agency (IEA), the carbon intensity of our energy use was 2.331 MtCO2/Mtoe in 2016 (the most recent full year for which there is adequate available data), exactly the same carbon intensity level as in 1990. This equivalence between 1990 and 2016 has taken place in the face of major changes over the last 25 years in the energy sector, including not only an exponential increase in the use of solar and wind for electricity generation, but also a dramatically bigger energy system in developing countries where demand is now about twice as high as it was in 1990.

What Has Been Happening and Why Is This a Concern?

Today, global energy demand is nearly 60 percent larger than in 1990, and unsurprisingly given the constancy of the energy sector’s carbon intensity, global CO2 emissions are similarly 60 percent higher at 32.1 Gt. But if we want to limit global temperature increase to below 2oC (the key internationally accepted threshold to avoid the most detrimental global impacts of climate change), climate modeling points to the need to reduce dramatically the energy sector’s CO2 emissions by over 50 percent by 2050. This substantial reduction in emissions will need to be done while allowing national economies to grow. To achieve this, we need to push on two distinct energy-related levers: (1) increasing the productivity of energy so as to delink economic growth from energy use; and (2) reducing the carbon intensity of that energy use. These two levers are the building blocks of the “carbon intensity of gross domestic product (GDP)” metric that is often cited.

The IEA’s scenario to limit temperature increase to below 2oC (the “2DS”) reduces the carbon intensity of energy use by about 60 percent as the share of fossil fuels in the energy mix is cut nearly in half by 2050, mostly replaced by renewables. By 2050, the global carbon intensity of our energy mix needs to drop from today’s level of 2.331 MtCO2/Mtoe to less than 1.0 MtCO2/Mtoe to achieve our climate goal. Reducing this carbon intensity is all the more important because projections consistently point to an increase in global energy use over the next several decades of 10 percent, 20 percent, even 30 percent or more, driven by various factors including increasing global population and economic growth. The only way to reduce significantly emissions in a context of increasing energy use is to lower dramatically the carbon intensity of the energy mix.

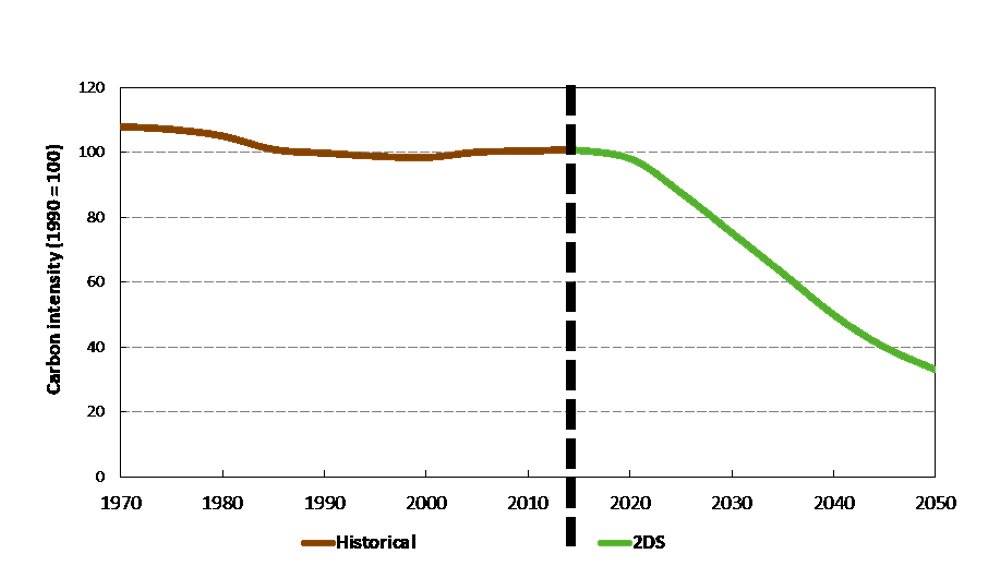

And that is why what has been happening—or more precisely what has not been happening—is a major cause for concern. The figure below shows how our energy sector’s carbon intensity has evolved over the past 50 years (indexed to 1990). Three periods emerge: (1) a slight drop from 1970 to 1990, driven in part by the substitution of nuclear power for oil-based generation (a shift that was partially motivated by the oil embargo of 1973); (2) virtually no change over the period stretching from 1990 to the present; and (3) the dramatic drop in carbon intensity that we will need to see to meet our 2oC climate goal under the 2DS.

Evolution of the energy sector’s carbon intensity, 1970–2050

Source: P. Benoit presentation at the Innovation for Cool Earth Forum, Tokyo, October 2016 (©OECD/IEA 2016).

A review of energy trends points to several key dynamics that have been driving the sector’s carbon intensity and its striking fixity over the past 25 years.

This analysis represents, of course, a simplification. There are various additional factors and nuances that affect the carbon intensity of our energy mix and merit a detailed analysis beyond the scope of this commentary. One involves the relative shares of the various fossil fuels, as coal, gas, and oil have different carbon intensities. For example, gas electricity production, which can be over 50 percent cleaner than coal generation from a CO2/kWh perspective, has seen its size increase from 46 percent of coal-generated TWhs in 2000 to 58 percent in 2015; this has put positive downward pressure on the sector’s carbon intensity. In fact, it is in part this shift from coal to gas power generation that has helped to produce the recent U.S. emissions reductions. Other factors that affect the carbon intensity of our energy mix include the share of nuclear power, the use of renewables for residential and industrial heat, and the deployment and capture rates of CCS in power and industry.

So, Will We Break with the Past?

Many reports and analyses point the way forward on how we can successfully reduce the carbon intensity of our energy mix. They are largely based on three key levers: (1) more renewables, as well as nuclear, in lieu of fossil fuel power generation; (2) greater use of electricity (as it decarbonizes) as an energy source for households, businesses, industry, etc. (shifting from gasoline to electric-powered vehicles illustrates this dynamic); and (3) increased use of renewables outside the power sector, notably for heat in the industry and residential sectors, as well as in transport. And we can get there…but will we?

There are a variety of positive and negative drivers at work, which have been commented upon extensively in other publications. For example, numerous countries have already successfully lowered the carbon intensity of their energy mix. This includes the United States whose carbon intensity dropped from 2.468 MtCO2/Mtoe in 2000 (which was above the global carbon intensity rate at the time) to 2.246 in 2016 (which is below the current global rate), an improvement driven in part by renewables whose share in electricity production increased from 8.6 percent to 15.2 percent over the same period. Moreover, while the renewables revolution may not yet have succeeded in reducing our energy sector’s carbon intensity at a global level, the increase in installed renewables power generation worldwide that we have witnessed over the last several years and that is projected to continue into the future will likely soon bear fruit in decarbonizing our energy mix. Technological improvements (e.g., in batteries) and fiscal support for CCS (included in recent U.S. tax legislation) are also positive factors. In contrast, the various pronouncements of the current U.S. administration questioning the impact of anthropogenic emissions on climate change and the corresponding shift in policy focus at a federal level from supporting renewables and energy efficiency to promoting fossil fuels have made the climate change mitigation effort more difficult. The impact of U.S. actions in this sphere are magnified by the fact that other countries still look to U.S. leadership in numerous related energy and economic areas, particularly since the United States is not only the largest economy in the world but also the second-largest emitter of energy sector CO2.

Beyond some of these broader dynamics, there are three points that flow from the striking fixity since 1990 of the energy sector’s carbon intensity.

Climate models are all clear on one point: going forward, we need to lower dramatically the carbon content of our energy use to address the climate change threat. While much has changed in the world since 1990, the carbon intensity of the energy mix unfortunately hasn’t. Analyzing its evolution provides useful insights into the dynamics of anthropogenic CO2 emissions, and closer monitoring of this metric can better inform us as to where we stand and where we are going in our efforts to combat climate change. Over the next several years, we will need to see a marked lowering of the carbon intensity of our energy use if we hope to have a real chance to avoid severe climate change.

Philippe Benoit is a senior associate with the Energy and National Security Program at the Center for Strategic and International Studies in Washington, D.C.

Commentary is produced by the Center for Strategic and International Studies (CSIS), a private, tax-exempt institution focusing on international public policy issues. Its research is nonpartisan and nonproprietary. CSIS does not take specific policy positions. Accordingly, all views, positions, and conclusions expressed in this publication should be understood to be solely those of the author(s).

© 2018 by the Center for Strategic and International Studies. All rights reserved.