UNDP in this New Era of Development | The Futures Summit

April 14, 2026 • 8:30 – 9:00 am EDT

Hosted by Global Development

Photo: technotr/Getty Images

This is the first installment in a five-part series providing data-driven analysis and recommendations to strengthen U.S.-Africa collaboration in the critical minerals sector.

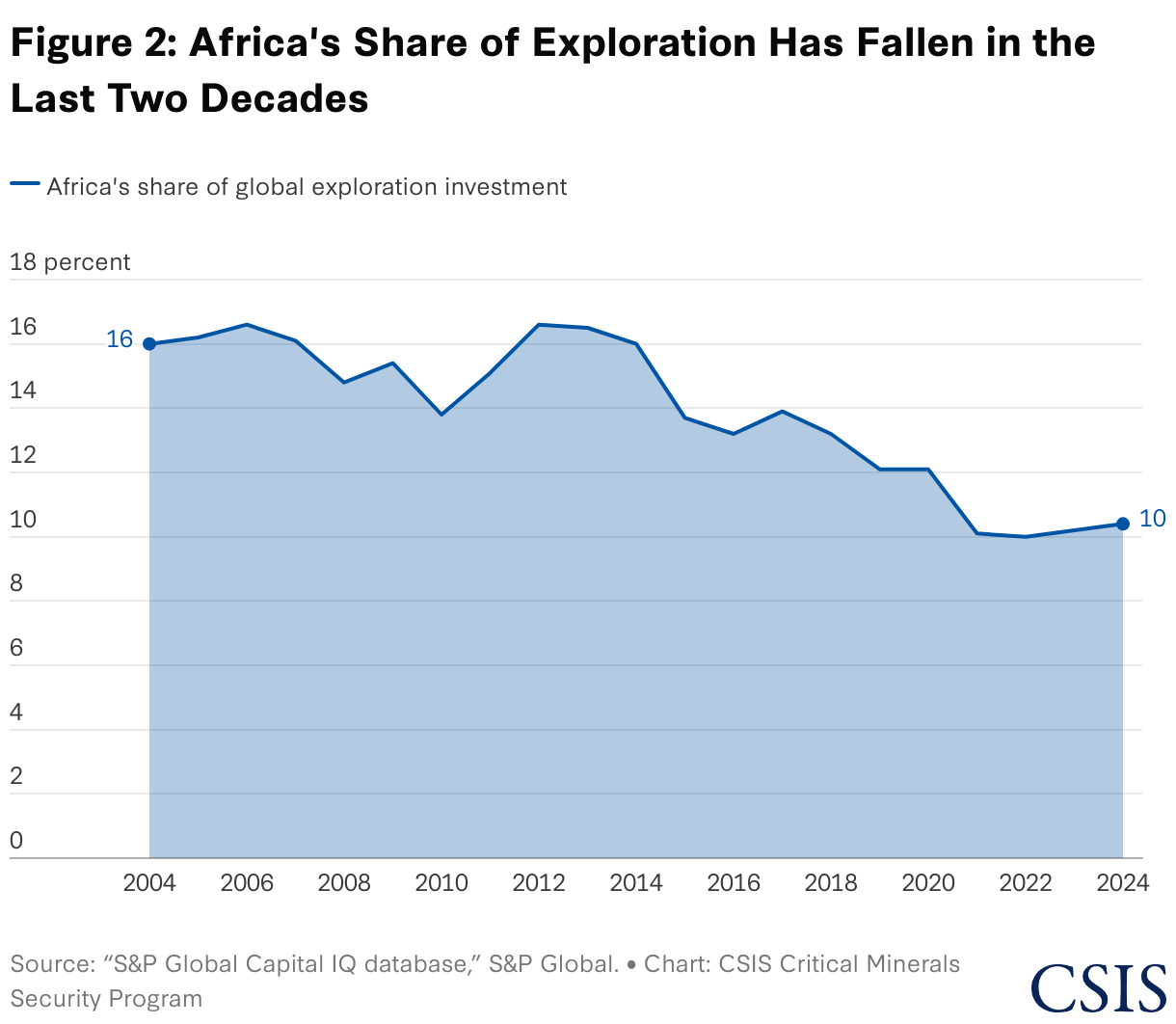

Africa has been consistently overlooked in global mineral exploration investment, despite offering some of the highest returns per dollar spent. Its share of global exploration spending has declined consistently, falling from 16 percent in 2004 to just 10.4 percent in 2024 (Figure 1). This drop is striking given that Sub-Saharan Africa is the most cost-effective region globally for mineral exploration, with the mineral value to exploration spending ratio of 0.8—far outperforming Australia (0.5), Canada (0.6), and Latin America (0.3). Yet, despite Africa’s vast geological potential and a landmass three times the size of Australia and Canada, those two countries received 15.9 percent and 19.8 percent of global exploration spending in 2024—significantly more than the entire African continent. This reveals a critical disconnect between Africa’s potential and actual investment, underscoring the need to rebalance exploration priorities.

Exploration is the oxygen of the mining industry—without it, future production cannot occur. Insufficient exploration investment limits the development of new mineral projects that could enhance supply chain resilience for the United States and its allies. As the United States expands its minerals diplomacy with African nations, incentivizing and de-risking exploration should be a priority.

This paper analyzed mineral exploration data across 14 mineral-rich African countries to distill five evidence-based insights, which serve as the foundation for the subsequent policy recommendations.

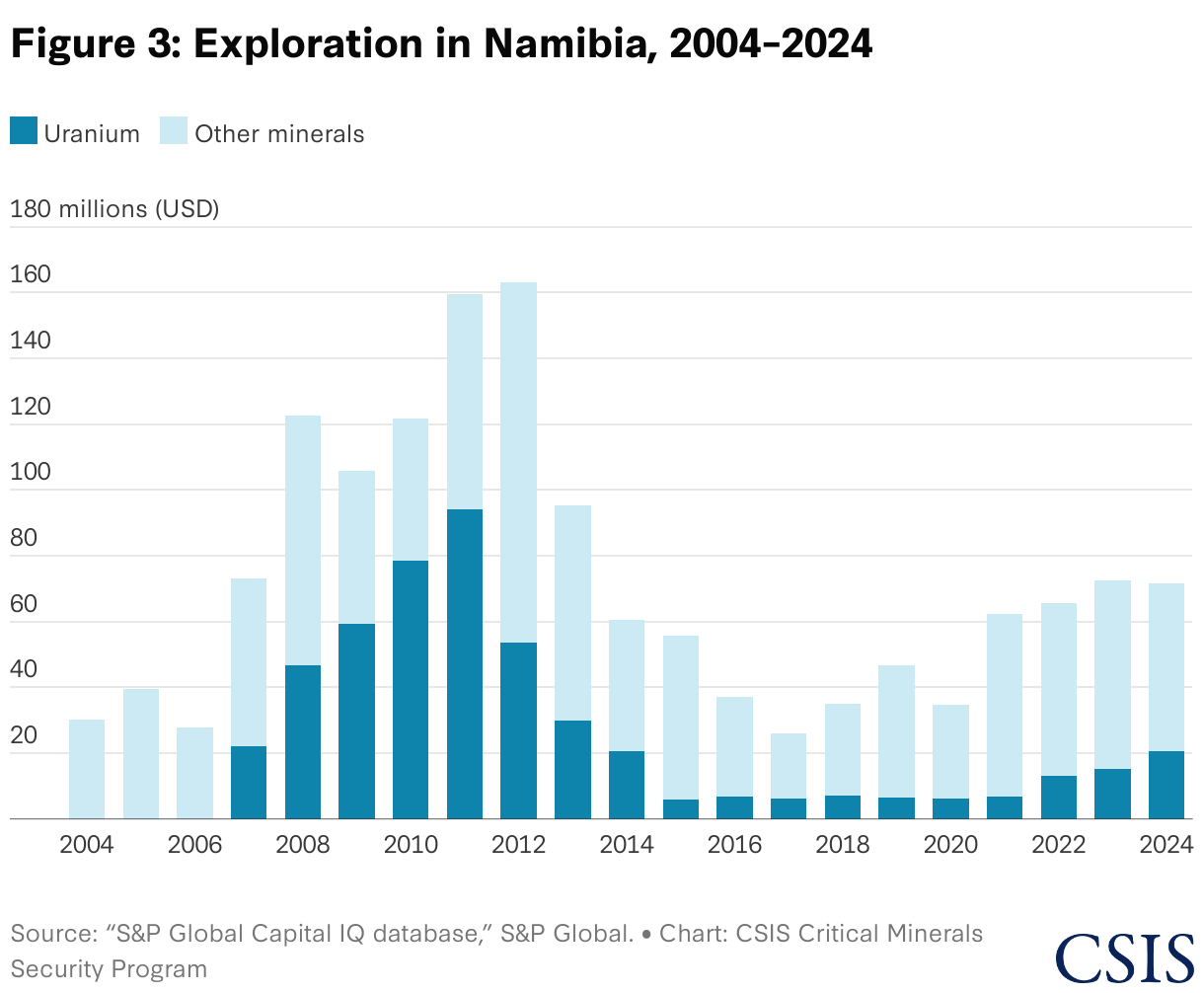

Namibia ranks as the world’s third-largest uranium producer—a position it achieved through substantial exploration investment. Between 2008 and 2012, the country averaged $66.5 million annually in uranium exploration alone. Today, Namibia hosts three active uranium mines—Rössing, Husab, and Langer Heinrich—all of which have significant Chinese ownership through entities such as the China National Uranium Corporation, China General Nuclear Power Group, and the China Africa Development Fund. Husab, the world’s second largest producing uranium mine, was discovered during the uranium exploration boom in 2008, began development in 2013, and is now 90 percent owned by Taurus Mineral Limited, a Hong Kong–based subsidiary of China Guandong Nuclear Power Corp (Figure 2). Rössing, originally discovered in 1928, saw a resurgence in exploration in the 2000s that led to a major expansion of its open pit operations. Uranium from both Rössing and Husab is shipped to China for enrichment.

The Democratic Republic of Congo (DRC) also stands out as a country where sustained exploration over the past two decades has led to significant mineral discoveries. Exploration activity accelerated shortly after the end of the civil war in 2003. Between 2005 and 2012, exploration spending surged by 582.8 percent—from $57 million to a peak of $389.2 million. Copper has consistently drawn the largest share of this investment, accounting for between 35 and 67 percent of total exploration spending from 2004 to 2024. These investments have paid off: the Kamoa-Kakula Complex in the DRC, which includes the Kamoa deposit (discovered in 2008) and the Kakula deposit (found in 2016), boasts the world’s highest copper ore grade at 2.52 percent. It’s likely that there will be new high-grade discoveries, given that the DRC remains Africa’s top destination for mineral exploration.

Exploration and project development already conducted have produced strong results for lithium in a short timeframe: Africa’s share of global lithium production is projected to rise fivefold from 2 percent in 2022 to 13 percent by 2027.

Even with strong geological fundamentals, conflict has driven out investment. Mozambique is a resource-rich country, with the third-largest graphite reserves in the world. However, Mozambique’s mineral exploration activity has sharply declined amid escalating violence in Cabo Delgado, the country’s northernmost province. The insurgency, led by Ahlu Sunna Waljama’a, began in October 2017 and remains one of Southern Africa’s most severe security challenges. In December 2024, Australian company Syrah Resources declared force majeure at its Balama graphite mine due to instability in the region, resulting in a default on its $150 million loan from the U.S. International Development Finance Corporation. The announcement caused Syrah’s share price to fall by 28 percent. Amidst the conflict, exploration spending, which totaled $25.5 million in 2014, fell to just $1.4 million in 2024 as a direct consequence of the conflict.

Similarly, political instability and coups in the Sahel region have deterred exploration investment. In Niger—where coups have been a recurring feature since independence—exploration spending dropped by 89.8 percent, from $66.4 million in 2012 (with uranium accounting for 87.8 percent of that total) to just $6.8 million in 2024. Mali experienced a sharp downturn more recently, with investment decreasing by half over the last two years, from $153.9 million in 2022 to $72 million in 2024. Similarly, Burkina Faso—following a January 2022 coup—witnessed a parallel 68.7 percent drop in exploration, from $121 million in 2021 to $37.9 million in 2024. Due to the complex political and social landscapes in many African countries, political risk insurance will be essential to catalyze investment in mineral exploration.

Tanzania has successfully turned around a downward exploration spiral that resulted from poor policies. In 2011, Tanzania attracted $212.7 million in exploration investment—8.2 percent of Africa’s total. However, when former Tanzanian President John Magufuli took office, he declared economic warfare on foreign mining companies and introduced resource nationalist policies, including export bans, contract renegotiations, and uncompetitive fiscal regulations. This led to a sharp decline in exploration investment—from $212.7 million in 2012 to an average of $55.6 million annually during his presidency (2016–2021). The election of President Samia Hassan marked a policy shift—she set out to make the mining sector a pillar of growth. Under her policies, exploration investment more than doubled from $47.2 million in the last year of Magufuli’s presidency in 2021 to $103.4 million in 2022, her first full year in office. The sector has also diversified: While gold previously dominated exploration, since 2023, most investment has shifted toward nickel and copper.

Zambia offers another turnaround story. Between 2010 and 2014, the country averaged $170.2 million annually in exploration spending, with the vast majority of investment concentrated in copper. However, the election of President Edgar Lungu in 2015 marked a shift toward resource nationalism, characterized by double taxation, withheld tax refunds, and repeated royalty hikes—including the country’s tenth royalty increase in 16 years in 2018. These measures led to a sharp decline in exploration, which fell to an average of just $32.7 million per year between 2016 and 2021—an 80.8 percent drop from the preceding four years. The election of President Hakainde Hichilema in 2021 signaled a policy reversal. He dismantled many of the restrictive measures imposed by his predecessor, and exploration investment began to rebound—rising 89 percent year-on-year in 2022, from $42.1 million to $79.6 million.

Rising interest in rare earth elements is driving a surge in exploration activity across several African countries that have had insignificant mining sectors historically. Though Uganda and Malawi have relatively small mining sectors, rare earths have brought both into sharper focus for investors. In Uganda, exploration spending climbed nearly tenfold—from $1.1 million in 2017 to $9.5 million in 2024—with 81 percent directed toward rare earths. Malawi saw a similar trend, with exploration rising from $2.2 million to $19.4 million over the same period, and over half (51.5 percent) focused on rare earths. In 2024, the U.S. International Development Finance Corporation also backed a feasibility study for rare earths processing in Angola, signaling broader strategic interest in African rare earths.

Across the continent, gold exploration has declined significantly over the last 15 years—and many of these economies did not diversify their exploration, impeding future growth of the mining industry. Between 2012 and 2024, gold exploration fell by 73.7 percent in Ghana, 89.7 percent in Burkina Faso, 58.9 percent in Mali, 74.8 percent in Tanzania, and 66.7 percent in South Africa—all Africa’s top gold exploration destinations.

In several countries, diamond exploration has seen a similar decline. In South Africa, for instance, diamond exploration averaged $126.2 million annually between 2006 and 2008. However, by 2022–2024, that figure had dropped sharply to an average of $8.3 million per year. This downturn has had a significant impact on South Africa’s broader exploration landscape, contributing to one of the steepest declines on the continent in absolute terms—from $403.6 million in total exploration investment in 2007 to just $121.3 million in 2024.

Botswana presents a strong example of successful diversification in mineral exploration. In 2006, diamonds received $76.5 million in exploration investment—or 67.5 percent of mineral exploration—while copper and nickel received $7.9 million (10.3 percent) and 10.9 million (13.8 percent). By 2024, diamond exploration had significantly dropped off, accounting for just $6.9 million in mineral exploration (amounting to 13.9 percent); in comparison, copper and nickel had increased to $23.5 million (42.3 percent) and $13.4 million (27 percent). While nickel prices remain depressed, copper prices have bullish forecasts, offering Botswana’s economy a layer of protection. Still, Africa received just 6.5 percent of the $3.2 billion spent on global copper exploration in 2024.

Speeding up Western-led exploration in Africa is crucial for three key reasons. First, it can identify new mineral assets that offer long-term, strategic supply. Second, it creates an opportunity to build supply chains that are independent of China. To safeguard these efforts, any U.S. exploration financing should include measures to keep ownership within allied nations. Third, such exploration can stimulate economic growth in African countries by attracting investment, expanding trade, and generating employment. For example, in South Africa, the Johannesburg-Pretoria metropolitan area emerged as the continent’s economic and financial center largely as a result of gold mining.

Gracelin Baskaran is director of the Critical Minerals Security Program at the Center for Strategic and International Studies in Washington, D.C.

Commentary by Gracelin Baskaran — August 29, 2023

Brief by Gracelin Baskaran — March 25, 2025