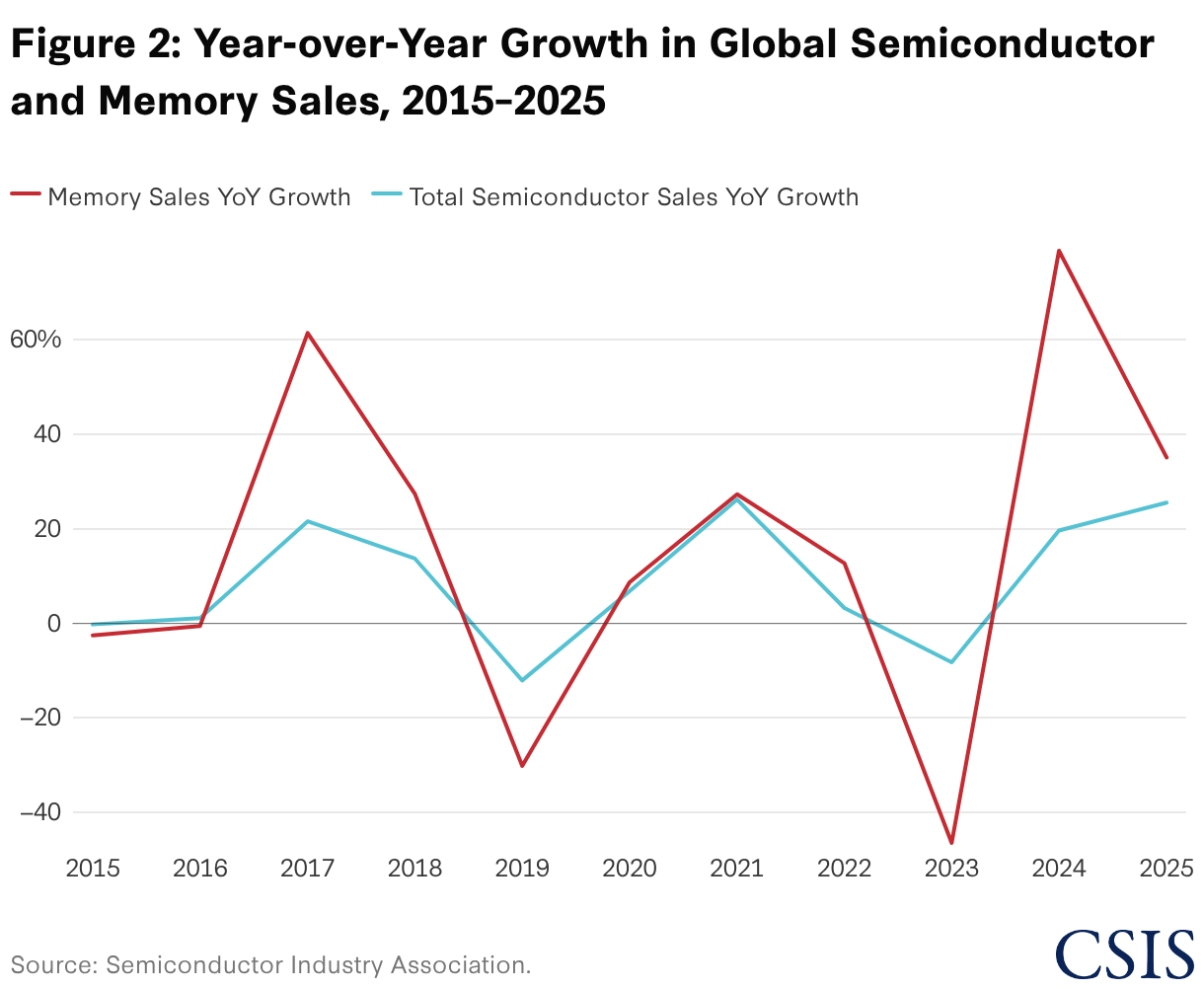

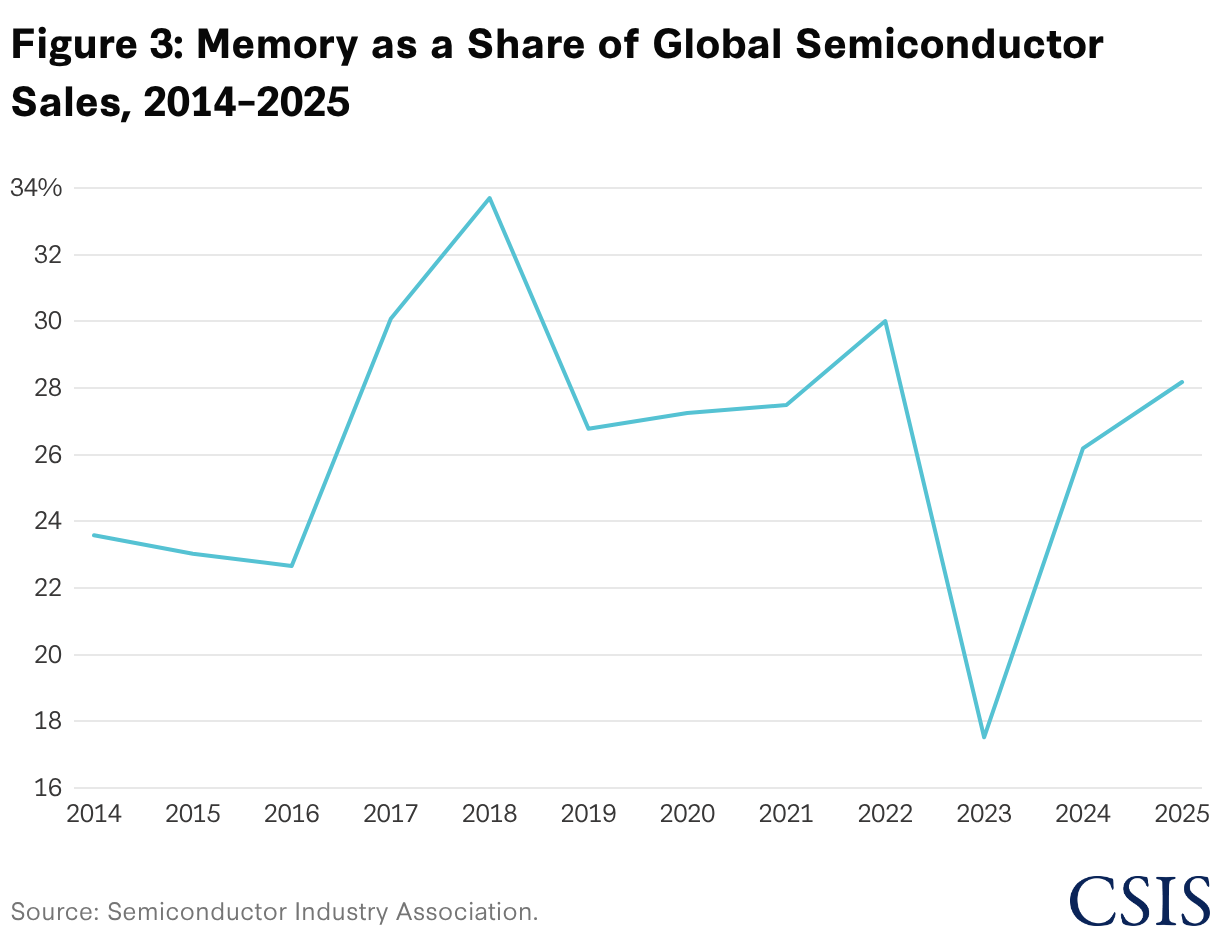

As demand for AI infrastructure has increased, memory manufacturers have adjusted production strategies to meet changing market requirements. Samsung, SK Hynix, and Micron—which account for more than 90 percent of global DRAM production—have expanded HBM output in response to growing demand from hyperscalers and AI firms. As a result, a larger share of global memory capacity is being directed toward data center applications, which are projected to consume roughly 70 percent of worldwide memory output in 2026.

What makes the current situation particularly significant is that it may not be resolved quickly. New memory fabrication facilities require investments of $15–20 billion and typically take several years to become operational. Although Samsung, SK Hynix, Micron, and emerging Chinese producers are investing heavily in new capacity, industry forecasts suggest shortages could persist through at least 2027 and potentially beyond.

The implications extend beyond near-term price increases. As demand for advanced memory continues to grow, access to memory components may become an increasingly important determinant of both industrial competitiveness and AI deployment. Industries that rely on memory-intensive technologies are facing higher costs and greater supply uncertainty, while firms developing AI infrastructure are likely to encounter longer lead times and increased competition for critical inputs. In this environment, memory capacity is becoming an increasingly strategic component of the broader semiconductor ecosystem.

As AI infrastructure expands, competition for memory is likely to intensify. Meeting future demand will require continued investment in both memory manufacturing and advanced packaging capacity, which is essential for producing HBM used in AI systems. Strengthening supply chain resilience, expanding domestic capacity, and working with trusted partners can help alleviate emerging bottlenecks and ensure that growth in AI infrastructure does not create constraints for other industries that rely on memory-intensive technologies.

Data visualization by Kharle Wu