The Futures Summit: A New Era of Development Cooperation

April 10, 2026 • 8:30 am – 4:30 pm EDT

Hosted by Global Development

Photo: Fabio Murgia/CSIS; assets from Wikimedia Commons

Over the past few decades, China’s high-tech drive has made enormous yet uneven progress, both in general and within specific industries. These advances have directly translated into enhanced international power and influence for China. The United States and like-minded countries need to respond pragmatically to maximize the opportunities and minimize the risks resulting from these developments. This commentary draws on analysis first presented in my recent CSIS report, The Power of Innovation: The Strategic Value of China’s High-Tech Drive.

China’s ranking in the Global Innovation Index (GII), the gold standard for cross-national innovation metrics, has risen substantially over the last two decades. China now ranks tenth overall among 139 tracked countries and third in the Asia-Pacific, behind only Singapore and South Korea and just ahead of Japan. Over the last decade China has distanced itself from developing countries such as India and Brazil. The shift in China’s position is the result of both government actions and corporate behavior. The central government and localities have invested heavily to strengthen the various components of the country’s innovation ecosystem, implemented industrial policy targeted at specific sectors, and used China’s size to attract high-tech foreign investment and diffuse their products to large markets at home and abroad. But government policy does not deserve all the credit. Government initiatives occasionally do not pan out, and oftentimes Chinese businesses have been successful in spite of government policies and then only endorsed by authorities after the fact.

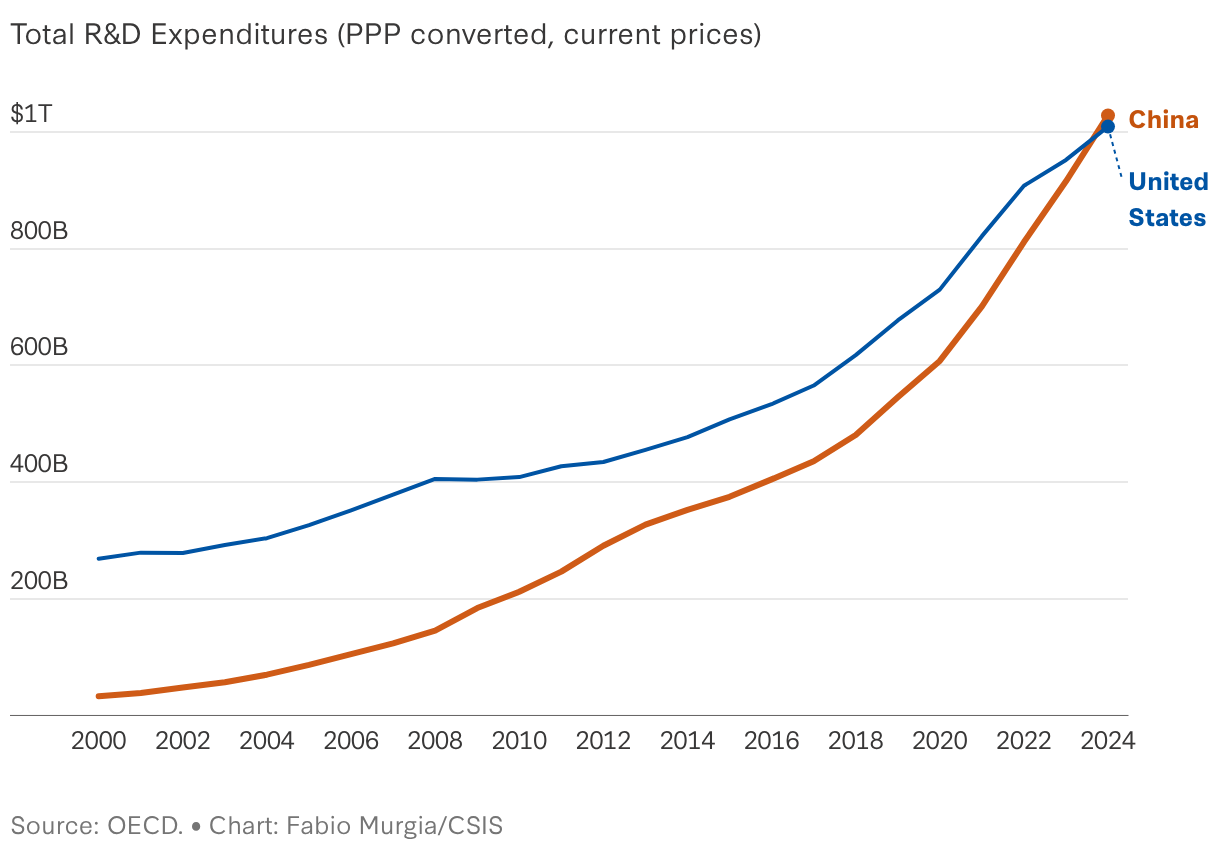

Chinese R&D spending has risen dramatically over the last quarter century in both absolute and relative terms. According to the Organisation for Economic Co-operation and Development (OECD), China’s spending rose from $32.90 billion (in purchasing power parity terms) in 2000 to $1.03 trillion in 2024, moving China slightly ahead of the U.S. total of $1.01 trillion. By 2025, China’s R&D spending reached 2.7 percent of GDP, which is identical to the overall average for OECD members. The United States and China still differ substantially in the sources of R&D funding, with China relying much more heavily on government outlays and the United States relying more on corporate spending.

The GII is composed of 78 individual measures grouped into five “input” and two “output” categories. China’s ranking varies widely across these various measures. China is ahead of the United States in infrastructure as well as knowledge and technology outputs; slightly behind in business sophistication, human capital and research, and creative outputs; and further behind in market sophistication and institutions. China’s weak institutional score is dragged down by low marks for regulatory quality and rule of law, and its mediocre market sophistication score is a reflection of limited microfinance, a small venture capital market, and high applied tariffs.

A long history of scandals and weak protection of intellectual property (IP) makes the pharmaceutical industry the biggest surprise among China’s sectoral successes. China has ramped up clinical trials, including for both domestically created novel drugs and for generic candidates first developed elsewhere. In addition, as others have shown, China is now the source of 30 percent of new innovative drugs produced globally. The core source of this sectoral success is human talent. Most of China’s pharma start-ups are led and staffed by experts who studied in the West and worked in leading pharmaceutical firms before returning home. These individuals carry with them strong research skills and deep familiarity with drug discovery and regulatory approval processes.

In contrast to pharma, EVs, and other successes, China’s efforts at making its own commercial aircraft should be counted so far as a failure. The Commercial Aircraft Corporation of China (COMAC) finally delivered its first narrow-body airliner, the C919, in late 2022, but it has been slow to ramp up production. COMAC did deliver 15 C919s in 2025, but that was far below its original target of 75 for the year and far fewer than comparable aircraft coming from Airbus or Boeing. Equally important, almost every critical system in the C919 is from the United States, Europe, or Japan; China’s efforts at localization have gone slowly. COMAC has begun planning for a wide-body plane, the C929, but it’s quite possible this plane will never reach markets. Why has it been so hard? Commercial aircraft are amazingly complicated, state-owned enterprises (SOEs) like COMAC are renowned for their lack of transparency and poor coordination skills, and certification of commercial planes and their components is led by regulators in the United States and Europe. The United States and Europe are likely to maintain, and even extend, their advantage going forward.

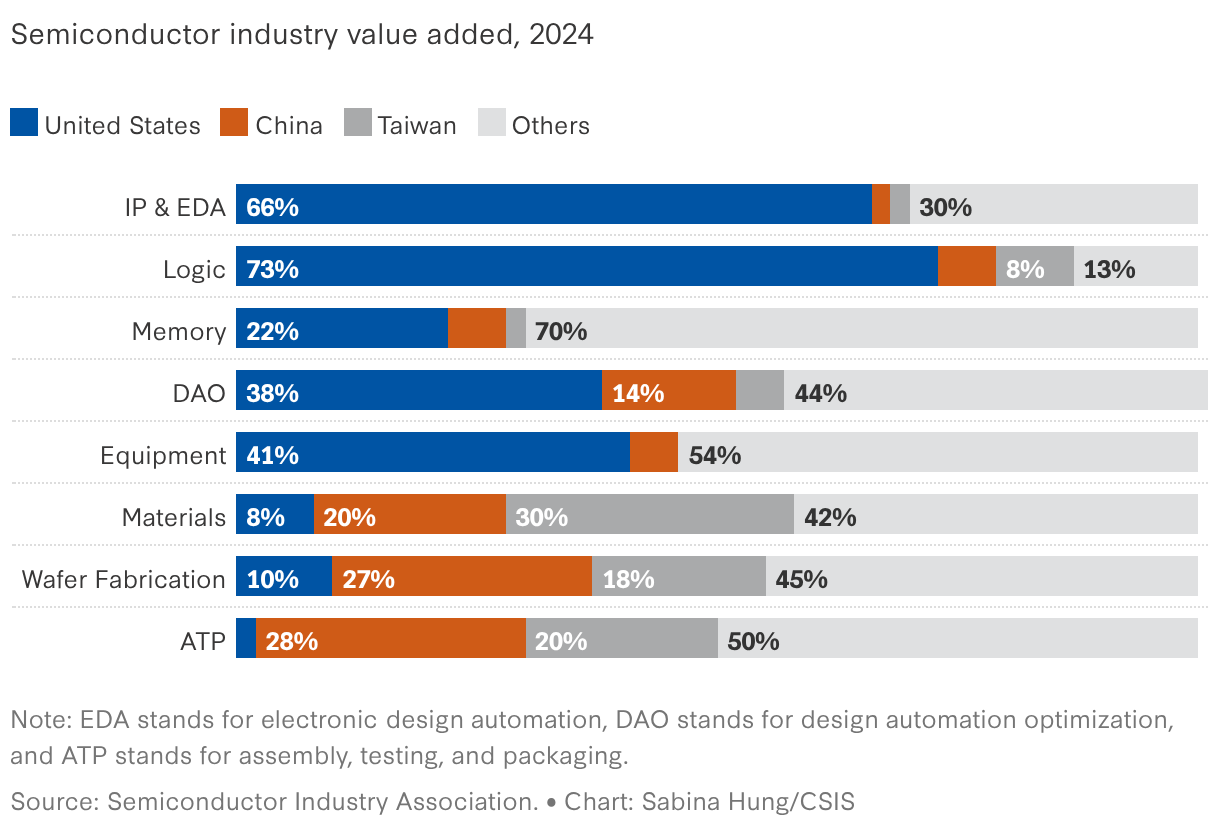

China’s efforts in semiconductors have yielded quite mixed results. For decades Chinese industrial policies for semiconductors generated little progress, with continued dependence on foreign suppliers for both chips and chip equipment. In the last five years, there has been a gradual shift, with China seeing progress in the development of materials, the fabrication of larger-node chips, and assembly, packaging, and testing (ATP). Less visible in the macro numbers is recent progress in memory and GPU chips used for AI. That said, firms from the United States, Taiwan, the Netherlands, Japan, and the United Kingdom still dominate the commanding heights of the semiconductor industry, with leads in chip design, advanced-node manufacturing, and semiconductor manufacturing equipment. China is likely to continue to make strides, at very high cost, but it is highly unlikely that China will become highly dominant in semiconductors, let alone entirely self-reliant.

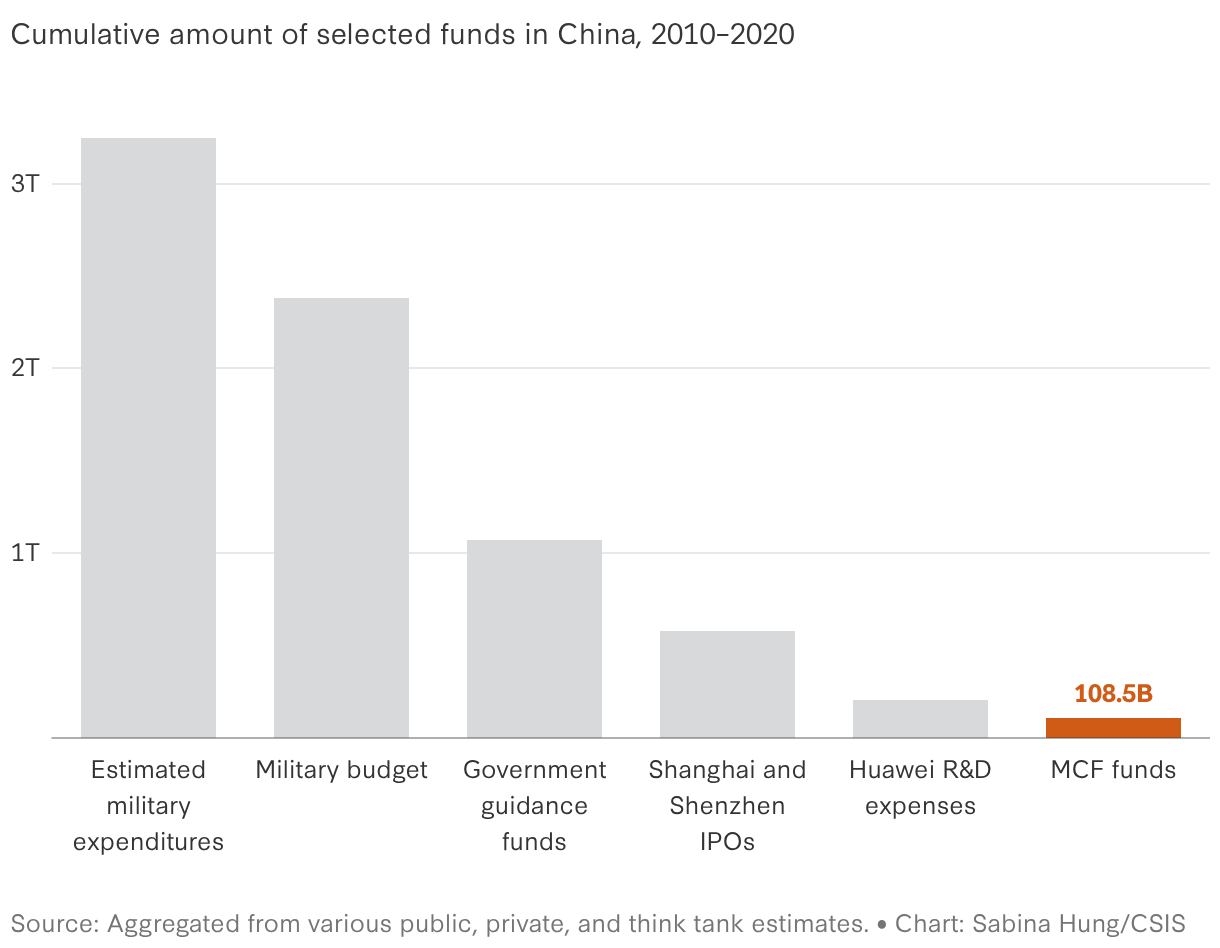

China’s military-civil fusion (MCF) initiative, which aims to direct civilian technologies and commercial firms to support China’s military modernization, has been trumpeted by China’s leadership and even written into the Chinese Communist Party’s constitution. MCF has also attracted enormous attention from the United States and other Western governments and is one reason for the expansion of Western export controls and other restrictions. Surprisingly, though, MCF’s actual budget is incredibly small. From 2012 to 2020, China’s central and regional governments created over 80 specialized MCF funds, but these funds cumulatively totaled only $108.5 billion over that period. This is far less than China spent over the same period on its overall military budget (either official or estimated), government guidance funds for other sectors, or the value of initial public offerings on China’s stock markets. Even the R&D budget of a single company, Huawei, was almost double the amount of all MCF funds during this period.

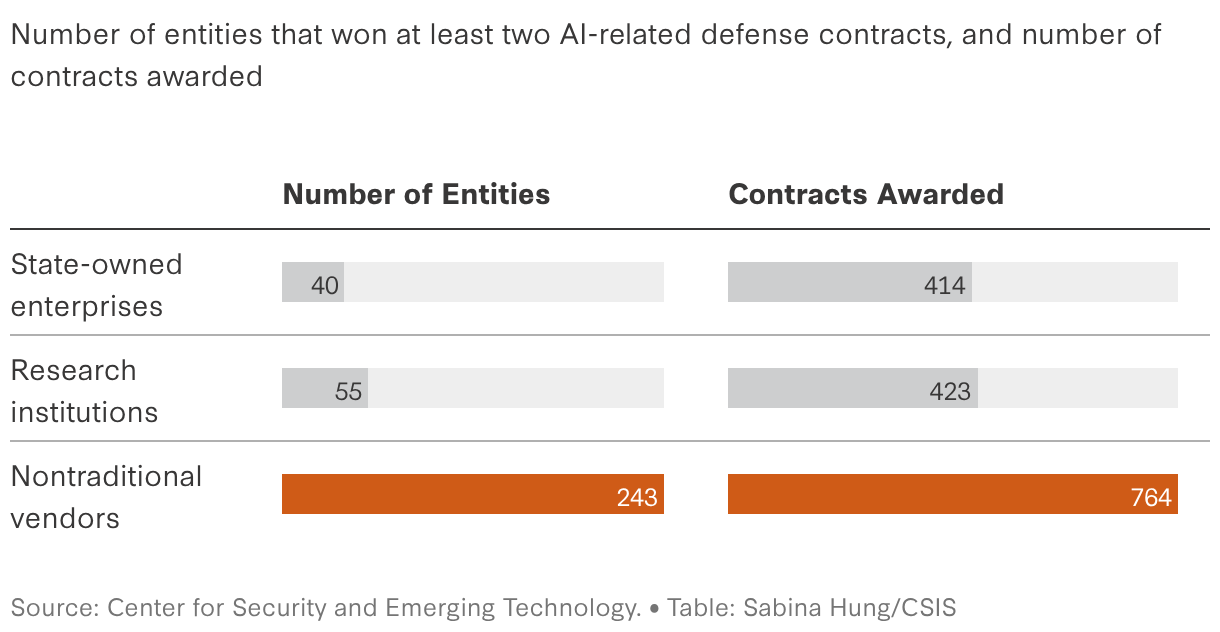

A critical role of MCF is to act as a bridge that connects companies that produce standard commercial products and dual-use technologies with the various parts of the People’s Liberation Army (PLA). The PLA uses platforms such as the Military Procurement Network (jundui caigouwang, 军队采购网) to issue bids and announce results. Georgetown University’s Center for Security and Emerging Technology (CSET) created a database of almost 3,000 AI-related contracts awarded by the PLA in 2023 and 2024. They found that over 70 percent of companies that won two or more AI-related contacts were “nontraditional vendors”—typically commercial AI companies such as iFlyTek Digital, PIESAT, NovaSky, JOUAV, and Nanjing Huage Information Technology. They also found that 11 of the top 15 successful bidders were SOEs and other organizations that regularly engage with the PLA.

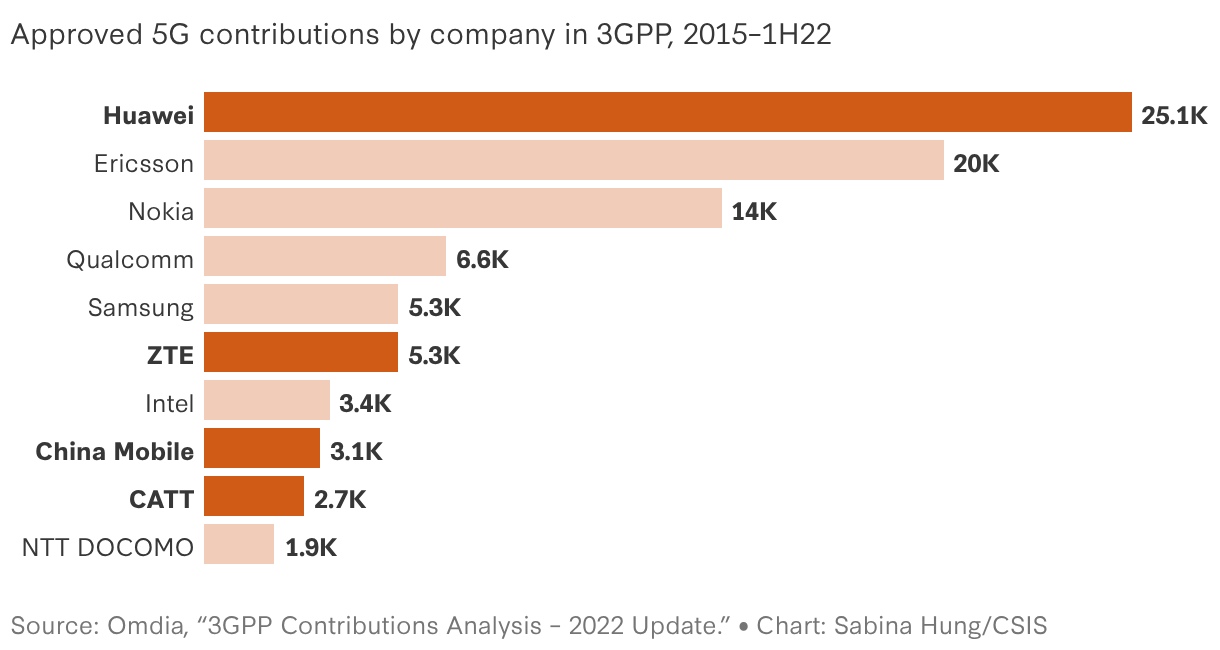

The growing technological capabilities of Chinese companies and research organizations has been the foundation for the country becoming more influential in the setting of international technical standards. One of the key standards bodies for mobile broadband is 3GPP, a multi-stakeholder consortium that has played a central role in setting the detailed technical specifications for cellular communications since the organization’s establishment in the late 1990s, when third-generation (3G) standards were being developed. Chinese experts have gone from being passive observers to active leaders, heading more of 3GPP’s working groups than representatives from any other country. Serving as chair or vice chair does not afford enormous power, but it reflects the growing consensus that China is a core player in many technical fields.

Representatives from Chinese firms not only show up to standards meetings in large numbers, increasingly hold leadership positions, and put forward many proposals, but the number of accepted contributions from Chinese sources has also risen dramatically. There may be some politics at play, but standards organizations such as 3GPP are highly technical—proposals that are highly deficient or technically inferior generally do not get accepted. Figure 10 shows how significant Chinese contributors have become, with Huawei having become the top single contributor in terms of number of contributions and three other Chinese organizations appearing among the top 10. At the same time, experts also note that this data may somewhat overstate Chinese contributions, as traditional telecommunications organizations in the United States and Europe still have enormous influence over the core elements of 5G-related technologies, a situation not captured in the raw figures.

China’s technological progress is unmistakable, in general and in specific industries, but it is also uneven. There have been tremendous strides, but also great waste and failures, such that China’s economic growth is likely to continue to stagnate and decline. This record points to three policy takeaways for the United States. First, to the extent the United States utilizes industrial policy, it should target areas where China has been most disruptive, such as EVs and semiconductors, and focus on innovating new leapfrog technologies, not replicating Chinese innovations or simply expanding manufacturing capacity. Second, a policy of consistent decoupling will not serve the United States well. Instead, it should pursue a strategy of “calibrated coupling,” alternatively reducing connectivity where necessary and maintaining vigilant connectivity where appropriate, thereby maximizing the economic and national security benefits and minimizing the risks from the relationship. And third, the United States will need to strengthen coordination and cooperation with other like-minded countries that are technology leaders as well as with developing countries in the Global South. Unilateral efforts, by contrast, are highly likely to slow American innovation and leave the United States isolated.

This commentary is made possible by the generous support from the Smith Richardson Foundation.

Report by Scott Kennedy — March 2, 2026

Report by CSIS Scholars — January 20, 2026