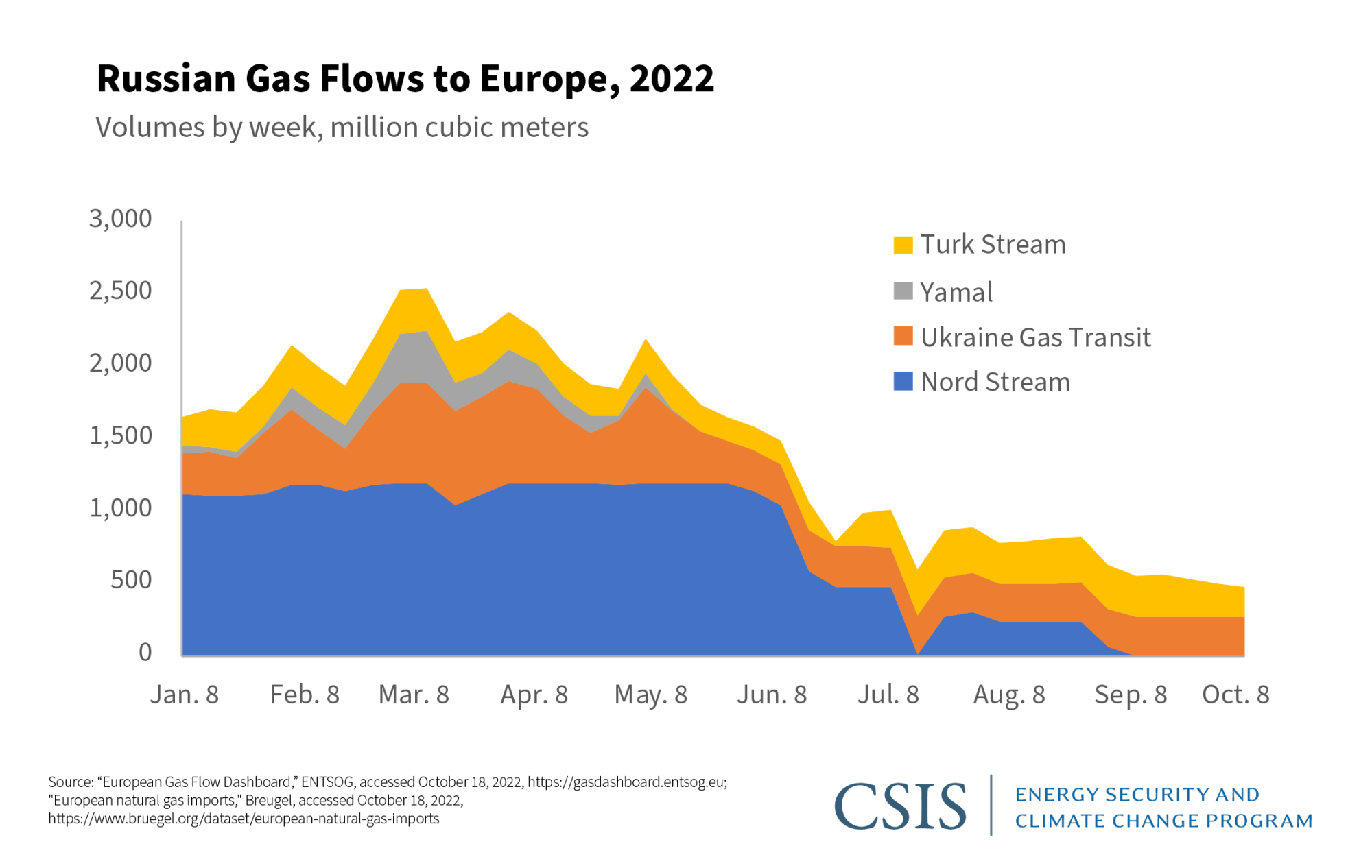

Worries about a supply shock this winter have eased somewhat as countries have replenished their natural gas inventories, reaching an EU-wide rate of 92 percent by October 17. Success in finding alternative gas supplies—albeit at a heavy cost—and declining demand has increased confidence that Europe will make it through the winter. Natural gas prices have dropped in recent weeks, but remained above 110 euros per megawatt hour (€110/MWh) as of October 18, curtailing industrial output and hindering economic growth.

As the focus shifts beyond this winter, EU policymakers are intervening in markets to shape prices and protect consumers, but disagreements are surfacing. A key sticking point is the debate over gas price caps. Several distinct ideas have been proposed. The European Commission has proposed a “dynamic price limit” for transactions in the Title Transfer Facility (TTF), Europe’s principal gas exchange. The idea is to create a range for spot market transactions and to bar TTF transactions at any price above that range. A “price corridor” would index the new TTF price to other EU gas trading hubs, to ensure a competitive rate that would attract supply, but without the wild fluctuations in TTF prices seen this year. The approach appears to have support from EU states including Belgium, Greece, Italy, and Poland. The commission is also proposing a “circuit breaker” mechanism to halt trading of gas and electricity derivatives in periods of extreme volatility. The European Commission claims that these are essentially temporary measures as it works to create a new benchmark for liquefied natural gas (LNG) by March 2023. These proposals may not be accepted by all EU states, and energy ministers will also consider other ideas when they meet next week.

Efforts to Cut Demand, Protect Consumers, and Support Renewables

The latest proposals follow earlier efforts to cut gas demand and shield consumers from high gas and power prices. On September 30, EU energy ministers approved a package of emergency measures including mandatory reductions in power consumption, a revenue cap for electricity generators who do not use gas, and a levy on fossil fuel company profits. A combination of market forces and policy interventions has already led to significant demand reductions, but new EU regulations introduce a mandatory target of at least a 5 percent reduction in gross electricity consumption during peak price hours. The European Council estimates that the reduction could save around 1.2 billion cubic meters of natural gas over a four-month period. Several countries have already taken steps to cut demand. Germany has banned certain lighting installations for monuments and public buildings, and capped heating levels for public buildings. As colder weather approaches, steeper demand reductions could require more effective public messaging.

The European Union also introduced a revenue cap for electricity generators such as renewable and nuclear energy providers, whose revenues have increased substantially over the past few months without a corresponding increase in operating costs. The cap looks to redistribute revenues over €180/MWh to end consumers who are most exposed to high electricity prices. The emergency package also introduced a “solidarity contribution” on fossil fuel companies, allowing a 33 percent levy on their “excess profits” in 2022.

In the short term, Europe’s climate ambitions seem to be taking a back seat to energy security concerns, and its coal imports soared by 36 percent in January to August 2022 over the same period last year. But the crisis has also led many EU countries to accelerate their renewable energy targets and timelines. The RePowerEU plan included measures to accelerate renewable energy development, including a more ambitious target of 45 percent renewable generation in the power sector by 2030. The plan also targets an additional €210 billion ($204 billion) in renewable energy investment by 2027, with a significant share directed towards solar and wind generation. The European Union aims to generate 320 gigawatts (GW) of solar photovoltaic capacity by 2025, and almost 600 GW by 2030. Belgium will increase renewable energy investments by around €1 billion ($978 million), and relief packages in France, Italy, and Spain include increased funding for renewables.

Despite these commitments, new projects and expansions will have little impact in the short to medium term. In 2021, when natural gas prices started to rise, mild wind speeds led to lower electricity generation across the bloc, pushing prices higher. Over the next two winters, strong production from installed renewable projects will be important, while for the medium-term rollout, it will be critical to ensure funding for supporting infrastructure and for expanding grid capacity. Buildout and integration of renewable energy will require improved permitting processes across member states, as well as increased transparency around grid regulations. Renewables may not save the European Union from the immediate energy crunch, but the crisis will accelerate the energy transition.

Heading for a More Challenging Phase

Unless there is an unusually cold winter in Europe, the continent is likely to make it through the coming months without major shortages. High prices are exacting a heavy toll, but they have curtailed gas demand and probably attracted sufficient supplies for the winter. The policy challenges to come are arguably greater.