At the end of October 2017, the OPEC/non-OPEC agreement to cut oil production finally achieved its purported objective of raising oil prices to a level of $60 per barrel. The apparent success in steering the oil market toward a rebalance and bolstering prices is built largely on Saudi Arabia’s overcompliance and Russia’s recent compliance to agreed production cuts, while the rest of OPEC exceeds its combined quotas and negligible contributions come from other non-OPEC producers. Although historical precedents indicate that Russia has preferred to free ride on OPEC production cuts, there are several recent developments that suggest that they may be more committed to cooperating with the Saudis this time around.

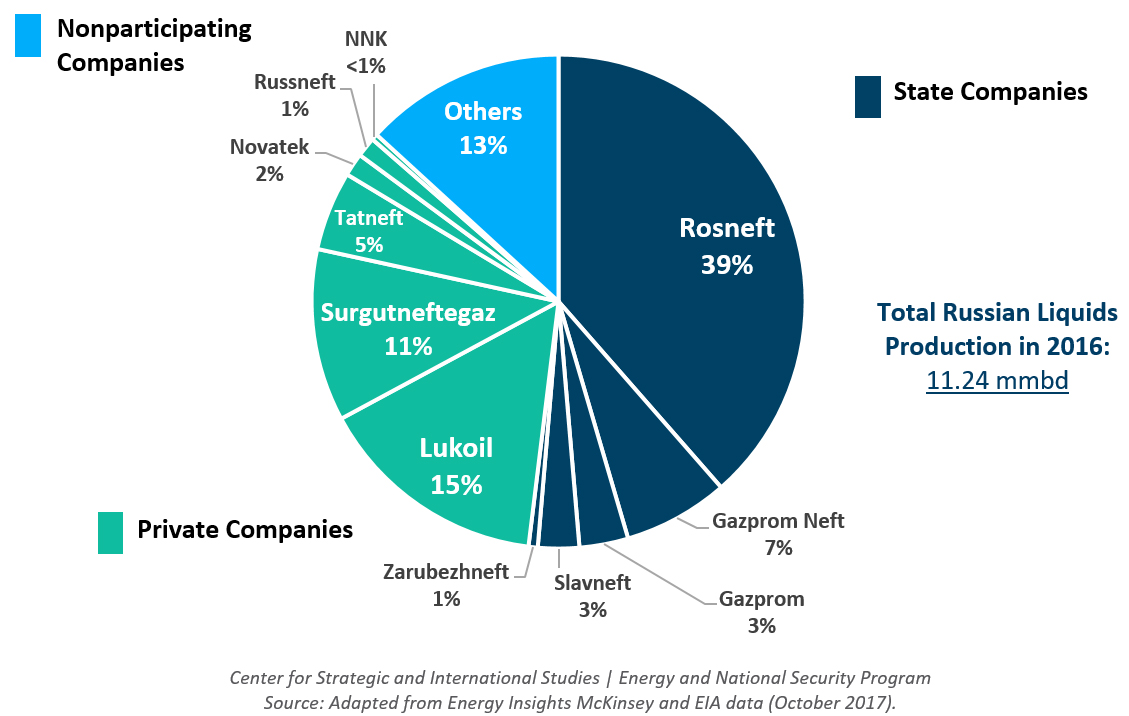

First, Russia has in fact reduced its output and achieved compliance, and regardless of operational difficulties, objections by Russian oil companies, and longstanding doubts concerning Russia’s commitment to the deal, if President Vladimir Putin and the Kremlin wish for the agreed cuts to be met, it is very likely that they will be. More than 50 percent of production is controlled by the state through its shareholdings in Rosneft and several other companies, and Putin arguably has a greater hold on the Russian oil sector than ever before.

Second, King Salman’s recent visit to Russia was the first ever by a Saudi monarch. With Russia facing a new set of sanctions from the United States on top of the 2014 coordinated sanctions with the European Union, Moscow appears to be exploring economic opportunities with an alternative group of partners, most notably China and India, but that group appears to be expanding to the Middle East and may include Saudi Arabia given the announcement of more than $3 billion in potential investment deals upon the king’s visit.

While the relationship between the pair may only be one of convenience, likely only lasting as long as both partners believe the benefits outweigh the costs, for the moment at least cooperation appears to be mutually beneficial. The Saudis need a large oil producing partner to effectively influence the market, and the potential for a greater geopolitical and economic role in the Middle East for Russia makes compliance to production cuts an expedient move for Moscow.

With the 173rd Ordinary OPEC Meeting quickly approaching at the end of November, now is an opportune time to reflect upon some of the key uncertainties, motivations, and implications regarding Russia’s involvement in the cuts and its evolving relationship with Saudi Arabia.

OPEC/Non-OPEC Agreement: Further Action Needed

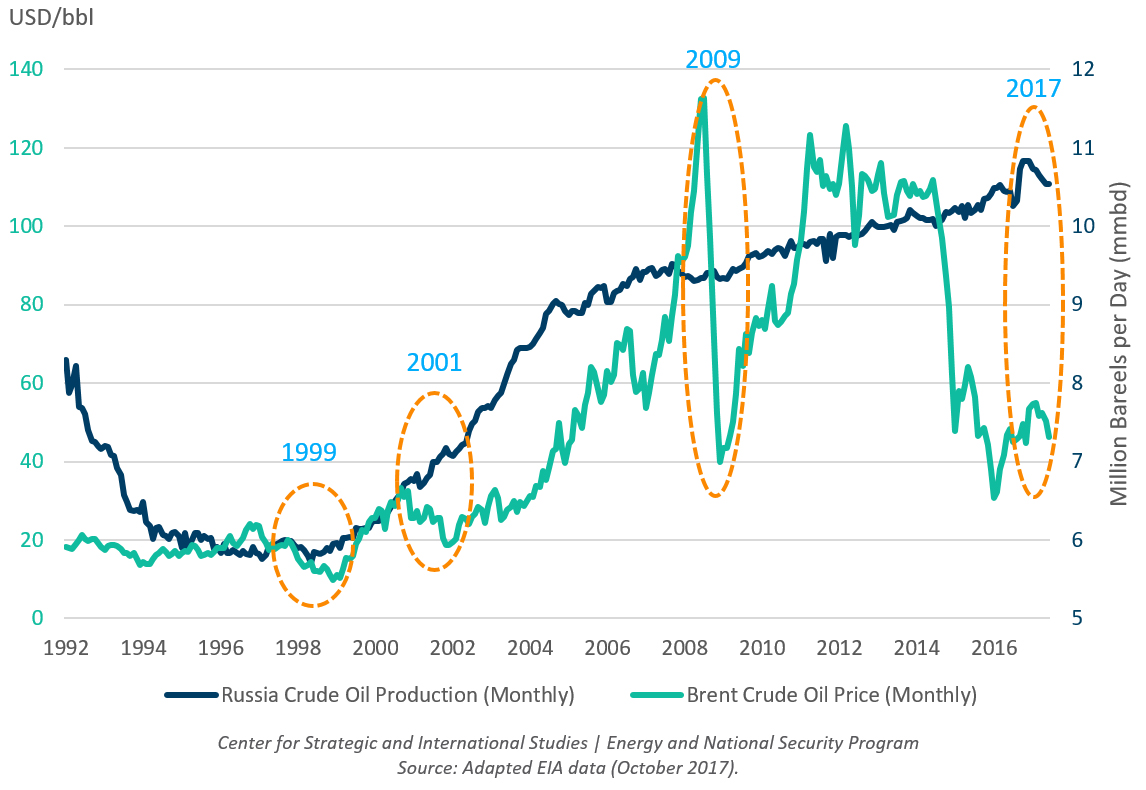

In December 2016, OPEC joined with a group of non-OPEC countries and set out to curtail crude oil output by 1.8 million barrels per day (mmbd) in a bid to rebalance the global oil market. The agreement marked a demonstrable change in tactics on the part of both Saudi Arabia and Russia, the leaders of the two groups. Saudi Arabia departed from its original plan to increase market share to reduce the impact of U.S. shale production. For its part, Russia agreed to join the production cuts even though just two years earlier it openly questioned the relevance of OPEC in the age of quick-cycle shale oil. While the agreement did not explicitly state an intended numerical price target upon its announcement (other than 1.8 mmbd curtailment), secretary general of OPEC Mohammad Barkindo offered some clarity at CSIS in December 2016 by stating that an unofficial quote of $60 oil had been used as an internal incentive within the group to garner supply restriction commitments. Additional clarity was offered in May 2017 upon the extension of the deal for another nine months, when Saudi oil minister Khalid Al-Falih stated that the intended target was to reduce global petroleum stocks to their five-year average.

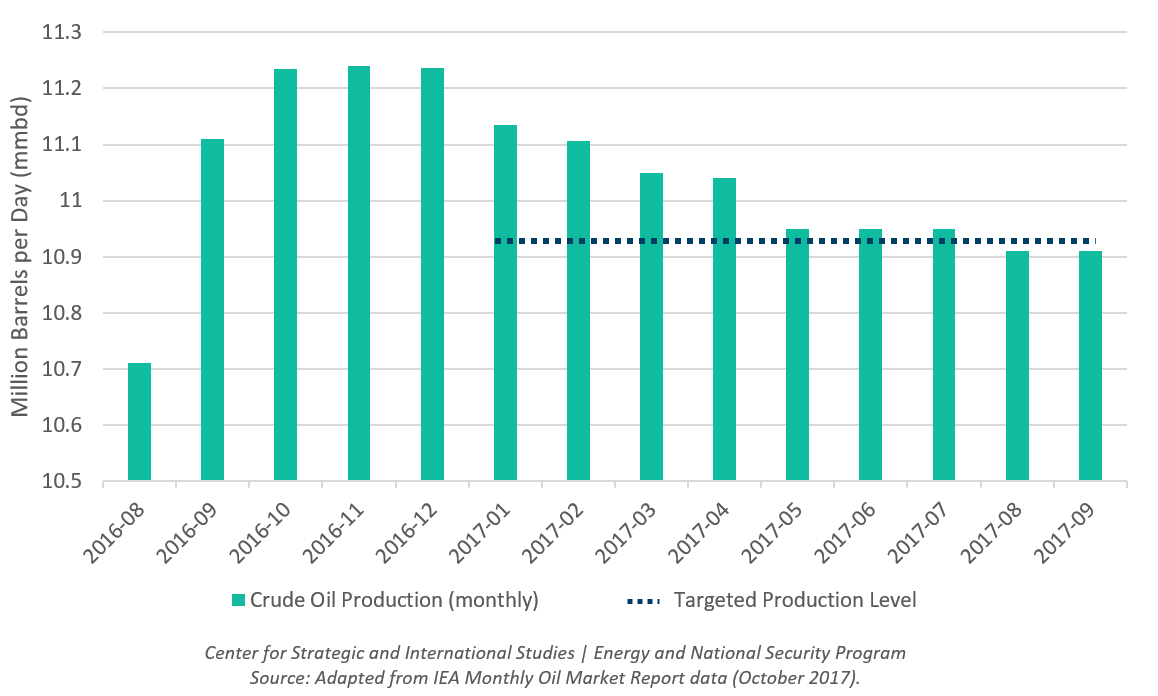

Russia, in becoming party to the agreement, made the commitment to cut 300 thousand barrels per day (mbd) of its crude oil production on a phased basis. At approximately 11 million barrels per day, this amounts to less than 3 percent of total Russian oil output. According to the International Energy Agency (IEA), Russia achieved full compliance in August and cut production by 318 mbd in September. However, it is worth noting that Russia (along with the majority of other participants to the deal) ramped up production to historical highs in the preceding months to the agreement. Consequently, Russia actually exceeded 2016 crude oil production by 160 mbd for the first six months of 2017. Though monthly production volumes fell below 2016 levels for the first time in September 2017, on an annual basis, Russia has not made a market-share sacrifice while still enjoying the economic benefits of the price increase and the political advantages of being party to the OPEC/non-OPEC agreement.

Current IEA data indicates that the production cuts are successfully reducing global petroleum stocks. However, even if the cuts are realized through the end of their expiration in March of 2018, global stocks would remain elevated above the five-year average. With the 22-member party to the deal still cumulatively producing in excess of its commitment to the cut in September, doubts linger as to whether the agreement can ultimately survive or succeed in fully rebalancing the market. That said, Saudi Arabia and Russia appear to be doubling down on their commitment to see the task through, with King Salman recently visiting Moscow and announcing that the two countries will continue to work toward stabilizing the market.

Russian Crude Oil Production and Compliance