Trustee Chair in Chinese Business and Economics > Trustee China Hand

It’s been over two years since the launching of China's version of NASDAQ, the Shanghai Stock Exchange’s Science and Technology Innovation Board, known as the STAR market. In 2019, the Trustee Chair team analyzed the STAR market’s initial 25 listed companies. Since then, it has grown substantially, with now more than 350 listed companies. The Trustee Chair team analyzed the new data to evaluate the STAR market’s performance two years later. Here are five key takeaways.

1. The STAR market is still relatively small.

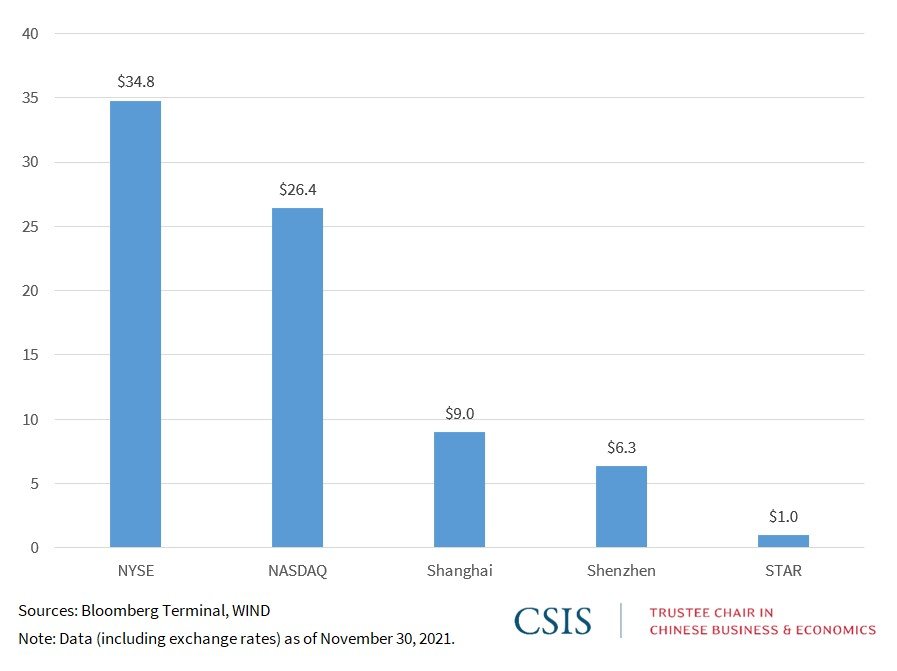

Although the STAR market has grown significantly over the past two years – from $113 billion to $976 billion in market cap – it is still puny compared to the Shanghai and Shenzhen exchanges, China’s corporate bond market, and credit generated through its banking system (see Figure 1). Nevertheless, the STAR market is a way for Beijing to signal its support for specific high-tech industries and a place for companies to raise a portion of their funds.

Figure 1: Total Market Cap ($ Trillions)