Sixteenth Annual South China Sea Conference

July 7, 2026 • 9:00 am – 4:00 pm EDT

Hosted by Southeast Asia Program

Photo: Getty Gallery/Adobe Stock

Diversified supply chains that cut across multiple geographies and generate significant economic benefits for the countries they connect are central to economic globalization. These complex networks of supply chains have contributed to increased stability and prosperity worldwide. They have opened new markets, transforming relationships between the developed and developing world and making supply chain resilience critical to sustained global economic growth. They have also become increasingly concentrated in a handful of geographic regions, such as China. In recent years, however, global supply chains have experienced a series of disruptions that call into question their resilience and have contributed to broader economic uncertainty.

Over the past 30 years, China has emerged as the preeminent global manufacturing hub, producing 14.7 percent of global exports of goods in 2020 and 28.7 percent of global manufacturing output in 2019. This is a remarkable three-fold jump from 2004 (just three years after its admission into the World Trade Organization, or WTO), when China’s manufacturing output stood at 8 percent of the global total. In addition to being the top exporter and manufacturer of goods, the world’s second-largest economy is also the leading trade partner for 128 countries, making any disruption to its manufacturing sector tremendously consequential to global supply chains. Across all sectors, China remains the largest source of imports for over a third of the world (65 countries) and is the world’s largest trading partner by volume of goods.

Covid-19 put the overreliance on China in stark relief, as countries found themselves unable to access critical supplies needed to respond to the pandemic. For instance, the United States imported over 97 percent of essential personal protective equipment (PPE)—including face shields, gloves, and other protective garments—from China. Other countries face similar risks, with 43 percent of global imports of PPE exported by China. More than 80 percent of the United States’ supply of active pharmaceutical ingredients (APIs) comes from just China and India. Up to 95 percent of ibuprofen (a common anti-inflammatory drug), 91 percent of hydrocortisone (a common dermatology medication), 70 percent of acetaminophen (used for pains and aches), and over 40 percent of heparin (used to treat blood clots) and penicillin (a critical but commonly used antibacterial drug) come from China. Valued at $74.6 billion in 2017, China’s supply of APIs constitutes over 40 percent of the global API market, giving Beijing enormous leverage in determining global access to critical and life-saving drugs.

The global economy’s overreliance on China was tested under the Trump administration, for whom adjusting the trade imbalance with China was a critical policy objective. The administration applied tariffs and other trade barriers on China, the United States’ top trading partner. In addition, after the Office of the U.S. Trade Representative (USTR) reported in June 2018 that U.S. intellectual property worth approximately $50 billion was being stolen by Chinese state action (or inaction) annually, the United States sought to counteract this economic damage by imposing 25 percent import tariffs on up to $370 billion in Chinese goods. While the Trump administration resorted to crude negotiating tactics (often disrupted by ill-timed tweets by the president), the overall objective of creating greater equity in the U.S.-China trade and economic relationship was—and continues to be—widely shared in Washington. Officials in the Biden administration sought to keep many of these tariffs in place when they entered office in January 2021.

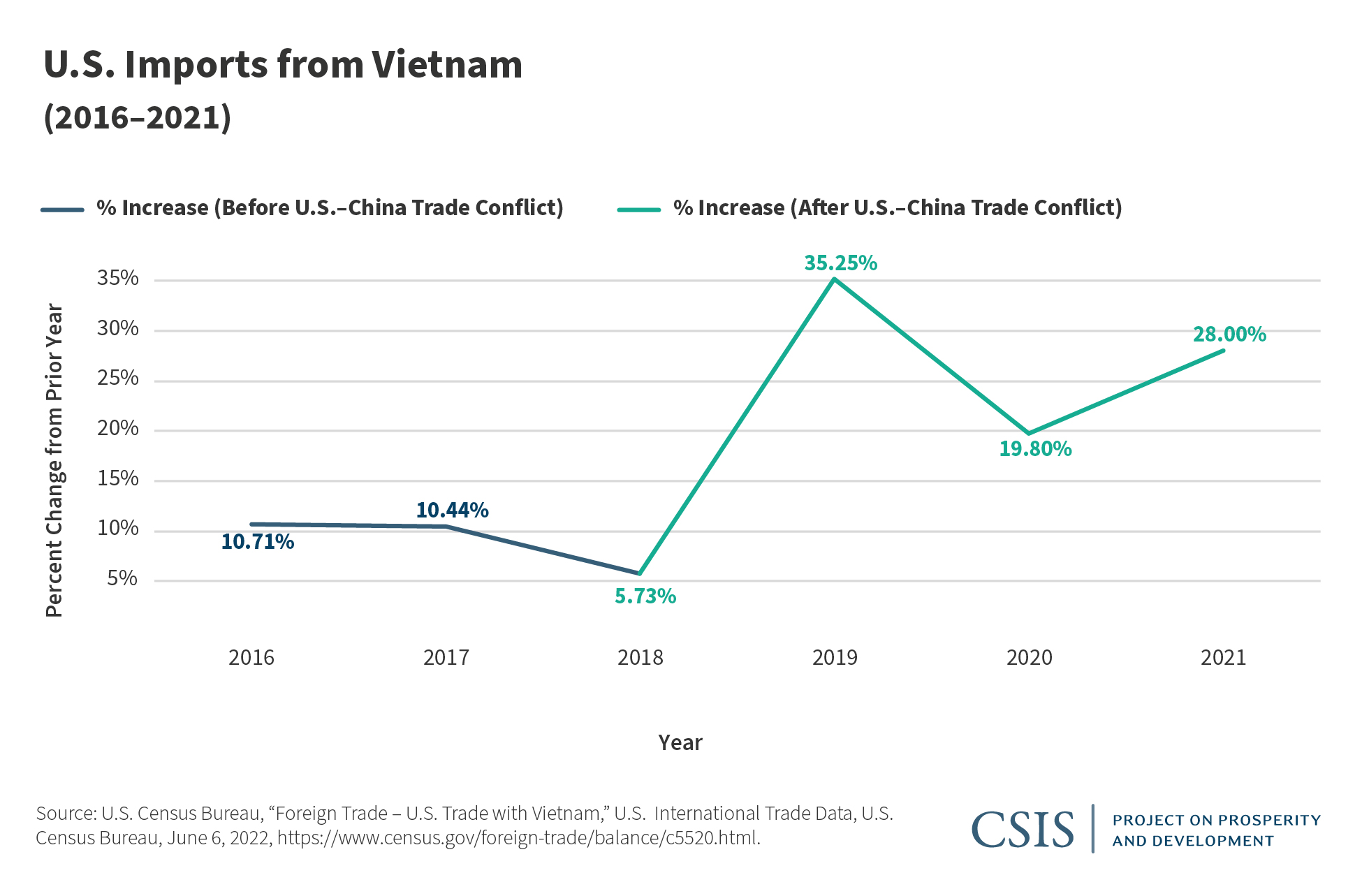

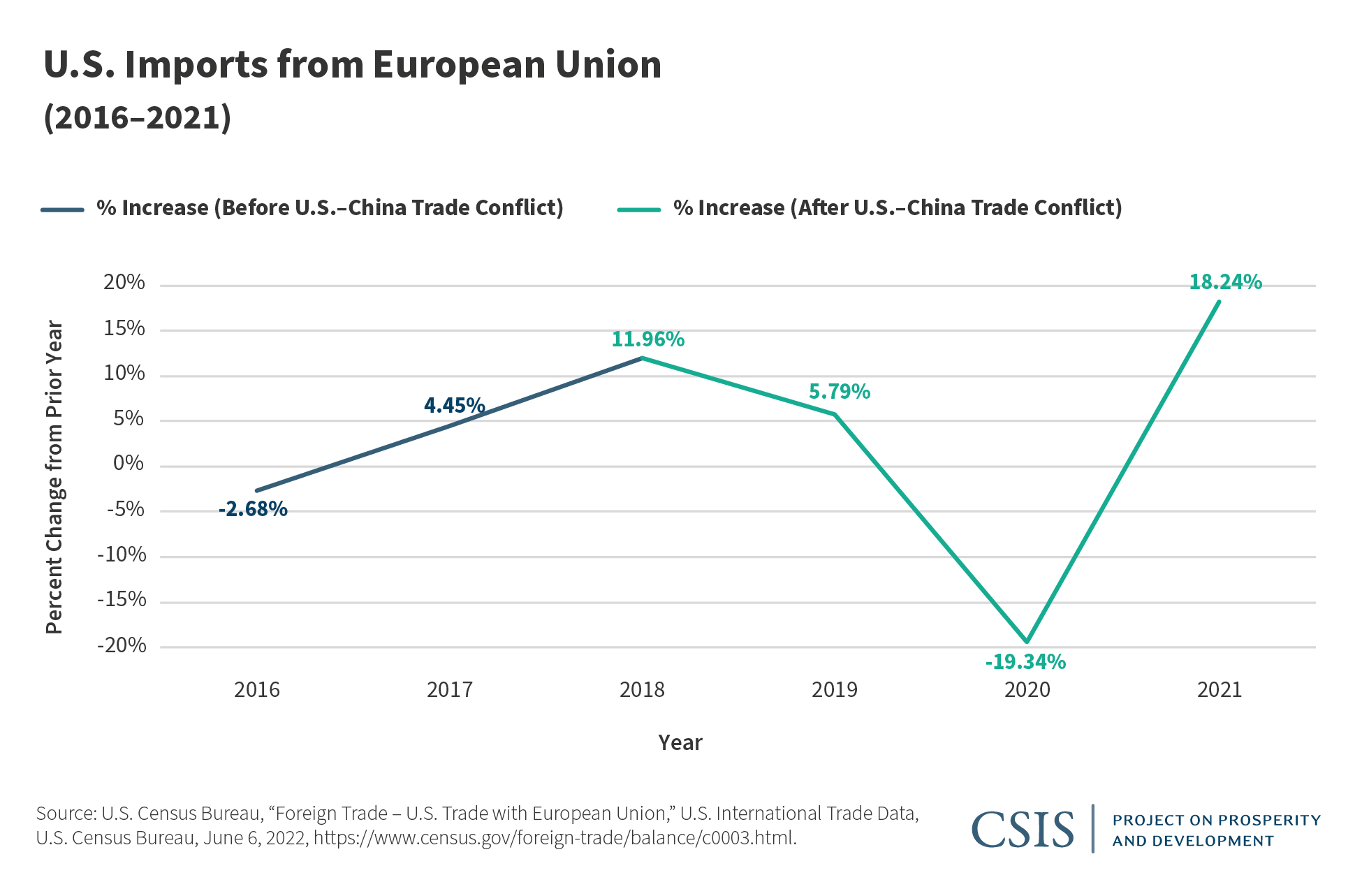

FIGURES 1-4

This economic overreliance, combined with the U.S.-China trade dispute, also disrupted global supply chains as it created new “winners” and “losers” in international commerce. The tariffs boosted U.S. imports of goods produced in Europe, Mexico, Taiwan, and Vietnam. This volatile global trading environment was further exacerbated by the Covid-19 pandemic, which emerged in late 2019 in China. The spread of the virus caused the World Health Organization (WHO) to declare a global public health emergency in January 2020. In response to the uncontrolled spread of Covid-19, governments around the world imposed stringent lockdowns that caused massive spikes in unemployment and crippling economic disruptions. Covid-19 restrictions made production levels drop, created massive bottlenecks at seaports, and precipitated other transportation delays. This caused the door-to-door movement of goods to slow dramatically—by 2022, the average freight container spent 20 percent more time in transit, leading to supply shortages around the world.

Since early 2021, as pandemic restrictions have eased, employment has recovered significantly and economic prospects have improved. Increased economic growth has created new problems as consumer demand has quickly outpaced supply, which in turn has triggered inflation at levels not seen in many advanced economies in decades. As of February 2022, around 44 percent of advanced economies and 71 percent of emerging markets and developing economies were experiencing consumer inflation of 5 percent or more. Compounding all of this are the crippling economic sanctions the United States imposed on Russia for its unprovoked invasion of Ukraine. While the sanctions are a necessary strategic response, they do carry costs for a global economy already reeling from continued supply chain disruptions and inflation by limiting access to critical energy supplies and minerals from Russia.

The supply chain crisis has tempted politicians to look to “onshore” industries by providing financial and other incentives to bring manufacturing back to a country that has lost industrial capacity. However, research by CSIS and other organizations suggests that such moves will lead to increased costs for consumers and an overall loss for the economy. It likely makes more sense to diversify supply chains through “nearshoring” or by exploring other countries that offer an economically viable alternative. By spreading sourcing, production, and shipping of goods and services across economically and geographically diverse nations, the risk of a single country shocking global supply chains due to natural or political factors is significantly lowered. To that end, bilateral and multilateral development institutions can use a range of tools and financial instruments to incentivize firms to join global efforts to diversify their production and distribution systems. The pandemic-induced supply chain crisis pushed major economies to publicly commit to diversifying the supply chains critical to domestic markets and protect the sectors most sensitive to their national interests.

The United States has been taking a few steps in this regard, using the U.S. International Development Finance Corporation (DFC) and the U.S. Export-Import (EXIM) Bank to support diversification efforts. In one prominent initiative in 2021, the DFC announced the award of a $500 million loan to finance the development of a thin-film solar-cell manufacturing facility in India. The deal, pegged as the largest single-debt transaction for the DFC, was one of the United States’ more direct efforts to diversify the supply chains of the critical renewable energy sector. The DFC also partnered with the French Development Agency’s Proparco, the German Investment Corporation, and the International Finance Corporation (IFC), jointly announcing €600 million (approximately $650 million) in financing to boost South Africa’s Covid-19 vaccine production and help countries in sub-Saharan Africa confront the pandemic. A similar partnership between the DFC, IFC, and the European Investment Bank provided $14 million in grants to Senegal, the first step of the $200 million project to expand vaccine production there.

To combat the threat of Chinese competition in strategic, “transformational” sectors such as biotechnology and semiconductors, the United States has also authorized the EXIM Bank to establish the China and Transformational Exports Program. Under this mandate, the EXIM Bank uses a range of financial instruments to help exporters in “transformational” sectors thrive despite competition from China, where state-owned financial institutions manipulate factors such as prices, land-acquisition policies, labor conditions, and industrial subsidies to promote Chinese-owned corporations. In November 2021, the EXIM Bank signed a bilateral agreement with Lithuania to deepen economic cooperation. The agreement provided for up to $600 million in loans and guarantees aimed at bolstering Lithuania’s capacity to produce and export lasers, semiconductors, biotechnology, and renewable energy products for U.S. markets, furthering supply chain diversification.

Since the early 2010s, Japan has pursued a policy of diversifying supply chains that support its domestic market activities. However, progress on these efforts has been slow. For example, when China cut off its exports of rare-earth minerals to Japan in 2010 (as part of their dispute over the Senkaku/Diaoyu Islands), the Japanese government invested in alternative sources of rare-earth minerals, including Kazakhstan, Malaysia, and Namibia, as well as other strategically aligned countries who met a share of Japan’s rare-earth mineral demands and reduced the country’s dependence on China. These efforts only intensified after the Covid-19 pandemic triggered an economic crisis. Starting in 2020, the Japanese government provided incentives—including $2.2 billion in 2020 and an additional $2.1 billion in 2021 in loans and subsidies—for its companies to move their production and distribution capabilities out of China. By April 2021, more than four out of five manufacturing companies in Japan had begun to diversify their supply chains to streamline their production processes and insulate them from exogenous shocks associated with overreliance on a single country. By the end of the year, more than 81 overseas projects operated by Japanese companies receiving this financial incentive decided to open plants and factories in Southeast Asian countries. These included facilities to manufacture Covid-19 test kits in Vietnam and medical rubber gloves in Malaysia.

In support of these efforts, the United States and Japan have committed to closer cooperation on supply chains in sensitive sectors such as semiconductors and digital infrastructure. In June 2021, the Japanese government operationalized this commitment with its Strategy for Semiconductors and the Digital Industry, which aims to promote the joint development of advanced foundries in countries around the world. In response to the economic crisis stemming from China’s manufacturing and supply disruptions, the Quadrilateral Security Dialogue (Quad)—consisting of Japan, the United States, Australia, and India—also launched the Supply Chain Resilience Initiative in April 2021, which seeks to de-risk global supply chains by enhancing digital technologies in supply chain management and diversifying trade and investment. Through this initiative, the Quad governments have sought to share best practices for building resilience in global supply chains. They have continued to convene on this issue, and in September 2021, the Quad also agreed to develop new supply chains to accelerate the development of the renewable energy and semiconductor sectors.

The U.S. government and its allies, including Japan, recognize the need to support greater diversification of supply chains. Covid-19, growing competition with China, and other causes of economic disruptions underscore the need to shift strategic supply chains to friendlier countries. The United States and Japan, alongside their partners in the Quad, should work together to facilitate these shifts. Both countries can provide significant official finance to support these efforts. The two governments should increase cooperation between their development agencies, development finance institutions, and export credit agencies to incentivize private companies to shift their supply chains. Using these economic and political capabilities, Japan and the United States can effectively leverage the long-term strategic investments necessary to transform and de-risk global supply chains for the private sector.

By its nature, the use of public resources to alter prevailing market dynamics carries political risks, as it can create “winners” and “losers.” The use of foreign assistance to diversify global supply chains is no different—even when it serves U.S. strategic and national security interests. The Biden administration can minimize the impact of these risks by ensuring that interventions to alter the global supply chain system are strategic and designed to produce a “win-win” scenario: diversified supply chains for the United States and increased economic growth for developing countries. To that end, this brief makes the following six recommendations for the United States and Japan:

The total value of international trade in 2021 reached nearly $29 trillion, representing approximately 30 percent of the global economy. More than three-fourths of this value was generated through the trade of goods that rely on global supply chains. Given the size and volume of trade that the current system supports, policymakers will need to remain prudent about diversification efforts. Specifically, the U.S. and Japanese governments should spearhead the development of a framework that can be used to identify economic sectors that should be prioritized for supply chain diversification.

Developing trade capacity among new country partners is mission-critical for any supply chain diversification efforts, as its absence will repel private capital investments. “Trade capacity” refers to the institutional, physical, and human capabilities that allow countries to participate and benefit from international trade. Foreign aid—which can take the form of financial tools and technical assistance—will have a catalytic role in this development. For many, building trade capacity begins with reforming the regulatory system, including export controls and customs processing. Describing itself as the “largest single-country provider of trade capacity building,” the U.S. Agency for International Development (USAID) aims to help developing countries transition their economies, conform with WTO standards, and harmonize their economic and trade practices. In the past two decades, for example, the United States has provided over $8.9 billion in assistance to sub-Saharan Africa and more than $4.7 billion to Latin America in support of trade capacity building, making the two regions the largest and second-largest recipients of such investments. A 2010 evaluation of USAID’s strategy for trade capacity building estimated that for every dollar invested in a country to build its trade capacity, the country enjoyed $42 in additional exports just two years later. In partnership with the Japan International Cooperation Agency, USAID can continue to build on its investments and support countries in their efforts to:

The U.S. Trade and Development Agency (USTDA) likewise has a record of helping developing countries make their transportation sectors and port security systems more efficient. The USTDA does this through a twin-pronged strategy: invest in enhanced technological capabilities and share best practices from the United States. In a similar vein, the USTDA can lead in connecting U.S. states with key ports (such as California, Florida, Massachusetts, and New York) with potential trading partners in the developing world, helping equip these countries with advanced data management systems to improve their access to supply chain information.

Technological upgrades can also expedite and secure export capabilities in countries where antiquated customs controls add to the costs for many firms—especially those trading perishable goods, for which the risks of total loss on an investment due to shipping delays are high. By implementing the WTO Trade Facilitation Agreement, these countries can address this deadweight economic loss; one WTO study estimated that universal implementation of this agreement in good faith could add over $1 trillion to the global economy per year while boosting global exports by up to $3.6 trillion. In particular, USTR and USAID can facilitate trade with countries that can be strategically vital trading partners. Both agencies could invest in these countries’ digital technology capabilities to improve their governance, harmonize their import and export standards, reduce the risk of corruption and delays, and consolidate flow-and-control functions for goods into a single-window clearance system.

While donor institutions have the capacity to de-risk new investments made by private firms in developing countries, doing so without addressing governance and corruption issues will lead the investments to fail and even create perverse incentives for firms to adopt fraudulent practices. The Biden administration has recognized that efforts to combat corruption are critical to national security interests and that they make global markets fairer and more equitable. Strengthening governance also leads to market stability and regulatory transparency, both of which are necessary conditions for countries to attract capital, especially when setting up new production facilities.

When deciding whether to invest in a country, manufacturing firms consider ease of land acquisition, flexibility within a country’s labor laws, taxation policies, entry and exit requirements, and other national and local laws. These factors carry significant risks to doing business in countries that either lack state capacity or have poor governance practices that contribute to weak rule of law. USAID can play a pivotal role in driving the U.S. efforts to fight corruption and build institutional stability in partner countries. To that end, the agency should:

The lack of resilient infrastructure in low- and middle-income countries robs the global economy of $4.2 trillion each year. Investors expecting a smooth and well-functioning trading system rely on the availability of durable infrastructure, encompassing a network of roads, railways, ports, airports, round-the-clock electricity access, and digital communication systems that can handle heavy data traffic. Therefore, investments in infrastructure are the most direct way governments can intervene to lower financial costs, mitigate business risks, attract private investment, and boost economic growth and net exports. To support developing countries in mobilizing new infrastructure investments, the development community should use a wide range of bilateral and multilateral financial instruments to:

Additionally, the USTDA can play a crucial role in partnering with developing countries and reforming their public procurement processes such that infrastructure projects are assessed holistically through a life-cycle cost analysis. To do this, the USTDA need only scale up its acclaimed Global Procurement Initiative from its current roster of 15 partner countries. Moreover, it can partner with the Japanese Ministry of Economy, Trade, and Industry to provide officials in developing countries training on best practices for quality infrastructure procurement, as they did in 2018 to train Association of Southeast Asian Nations officials in how to develop energy infrastructure.

Foreign assistance and public sector interventions can be used to attract investment and finance production facilities in new countries outside of China. By spreading out production facilities, firms help diversify supply chains and reduce the global overreliance on one country. Development finance institutions (DFIs) are useful in this regard, bringing a range of tools that can be used to:

Firms establishing production facilities in new countries are bound to experience challenges in mobilizing investment capital, as the lack of a robust manufacturing sector in a country raises the firm’s risk profile. DFIs such as the Japan Bank for International Cooperation (JBIC) and DFC—and their counterparts in the United Kingdom, Canada, and European Union—can lower these risks and boost confidence among direct and institutional investors by creating a blended concessional-finance facility and helping them overcome the early-stage risks of investment.

DFIs and export credit agencies—such as the Nippon Export and Investment Insurance (NEXI)—can also deploy credit guarantees, which can help firms improve financing terms (both debt and equity), hedge currency volatility, and increase the viability and profitability of new investments. Similarly, NEXI provides loan insurance up to 1.5 trillion yen (approximately $11.5 billion) for overseas Japanese subsidiaries to ensure they can access working capital. NEXI also offers overseas investment insurance (which indemnifies an overseas Japanese company or joint venture from losses incurred by war or terrorism), which can be used to protect investors supporting new facilities in countries facing fragility, conflict, and violence. These guarantees and insurance programs are critical to managing and mitigating the early-stage risks for new facilities and help attract firms to countries that are willing to host them but have historically lacked a robust manufacturing economy.

Finally, partial guarantees can help commercial lenders and banks in partner countries with challenging markets support trade and develop an export-import capacity. Guarantees can also help better performing lenders in partner countries securitize their more viable assets, allowing them to recycle capital quickly.

Micro, small, and medium-sized enterprises (MSMEs) constitute more than 90 percent of the global private sector, providing 70 percent of all jobs and driving half the global economy. According to a 2020 survey conducted by the International Trade Center, 55 percent of 4,467 MSMEs surveyed in 132 countries had sourcing challenges related to the supply shock caused by global lockdowns, with one-fifth of the MSMEs saying they were at risk of permanent closure within three months. In partnership with multilateral development banks, DFIs such as the DFC and JBIC can help this essential sector transition toward more diversified supply chains by offering them flexible and blended finance support that includes: (1) conventional, direct development assistance tools such as concessional loans and grants; (2) enterprise funds for making equity investments in the private sectors of developing countries; and (3) syndicated loans (or other structured financing vehicles) to limit the exposure of financial institutions when considering credit for MSMEs.

Donor institutions should remain cognizant of ecological risks, especially in the medical equipment sector, where the dramatic increase in the use of PPE because of Covid-19 has impacted existing waste-management systems. To address this, both the DFC and JBIC can prioritize investing in firms that have sustainable manufacturing practices. Donors should also promote the IFC’s four approaches to a circular economy: (1) use renewable, bio-based, or completely recyclable materials as input; (2) recover the latent resources and energy from disposed products; (3) prolong the lifespan of PPE products by using durable and repairable parts; and (4) promote the use of the “product-as-service” model, whereby equipment is leased for definite periods of time.

For the better part of the twentieth century, Western countries have been the champions of free trade. The United States should draw renewed attention to its long-standing commitment to increasing free trade worldwide and consider using economic incentives to create new free trade agreements with potential trading partners in strategically significant regions. These incentives will look different for each region or country.

Countries in ASEAN, for example, may seek preferential access to U.S. markets via a free trade agreement. This stems from the model adopted by the 2004 U.S.-Singapore Free Trade Agreement. The United States remains the only major economic power in the Pacific without a free trade agreement with ASEAN—though it does have agreements with each member country through the Comprehensive and Progressive Agreement for Trans-Pacific Partnership or the Regional Comprehensive Economic Partnership. This is to the United States’ detriment, as it leaves free trade with one of the most geostrategically significant parts of the world on the table. However, considering the political reality and the challenges surrounding forging a new free trade agreement, a more practical approach to ensure a stronger U.S. presence in the region would be to employ the Indo-Pacific Economic Framework for Prosperity (IPEF) that President Joe Biden launched on May 23, 2022. Unlike a conventional trade agreement, IPEF creates an institutional framework to govern a wide range of trade issues, including standards on data usage and privacy, carbon emissions and clean energy, and labor conditions. It also allows countries to selectively opt out of parts of the framework that are incongruent with their existing economic dynamics.

India is another economically and geostrategically significant partner for Japan and the United States. Despite past attempts to strike a bilateral free trade agreement, diverging interests on critical issues have kept such a deal out of reach. Yet there are areas for the two countries to boost trade (even absent a formal agreement), with signs of cooperation emerging in the digital economy, health care technology, renewable energy, and semiconductor sectors. These efforts can help meet medium-term goals and create the trust needed for the two countries to address concerns over unfair and protectionist trade practices, resolve the unpredictability around H-1B visas in the United States, and develop a framework to enable cross-border data flows.

Geographically proximate to the United States, countries in Latin America can be vital partners in building supply chain resilience, as they allow for nearshoring for U.S. markets. However, to ensure that the United States can trade freely in the region, it should consider re-examining and renewing the Dominican Republic-Central America Free Trade Agreement (CAFTA-DR) to reflect changes to the global economic landscape. The Biden administration can look to the United States-Mexico-Canada Agreement as a template, particularly regarding the global digital economy (which creates digital governance issues around privacy and cross-border data flows). Moreover, the United States can build on CAFTA-DR to pursue the hemisphere-wide trade deal that has thus far been evasive.

Over the past three years, the global economy has experienced enormous disruptions, during which the dependence of the United States and the rest of the world on China for critical products—including vaccine precursors, medical devices, semiconductors, and other electronics—came into stark relief. The economic consequences of the Covid-19 pandemic and the U.S.-China trade war will continue to impact the world economy for years to come, so finding ways to diversify supply chains is vital for the United States and its partners, both for economic and national security reasons. No one should underestimate how enormously complex this undertaking will be or how long it will take to achieve the desired results. The time to begin is now; it will take the full weight of the U.S. government, partners such as Japan, and the private sector to work together to bring about greater diversity in global supply chains. Done right, this could provide an economic “win-win” for both developed economies such as the United States and the developing countries that will be the beneficiaries of new industry.

Conor M. Savoy is a senior fellow with the Project on Prosperity and Development at the Center for Strategic and International Studies (CSIS) in Washington, D.C. Sundar R. Ramanujam is a research associate with the Project on Prosperity and Development.

This brief is made possible by support from the Ministry of Foreign Affairs of Japan and their cooperation with the CSIS Project on Prosperity and Development.

CSIS Briefs are produced by the Center for Strategic and International Studies (CSIS), a private, tax-exempt institution focusing on international public policy issues. Its research is nonpartisan and nonproprietary. CSIS does not take specific policy positions. Accordingly, all views, positions, and conclusions expressed in this publication should be understood to be solely those of the author(s).

© 2022 by the Center for Strategic and International Studies. All rights reserved.