Warfighting and War Winning in Space

May 26, 2026 • 1:00 – 1:45 pm EDT

Hosted by HTK Series

Photo: MANDEL NGAN/AFP via Getty Images

The visit by Saudi Crown Prince Mohammed bin Salman to Washington, D.C., marks a high-profile moment in the strategic partnership between the United States and Saudi Arabia. During meetings with U.S. President Donald Trump, the two sides are discussing a wide-ranging agenda: advancing arms and defense cooperation, expanding critical minerals cooperation, deepening economic and investment ties, and aligning on regional security challenges.

The visit represents a major step forward in the bilateral minerals relationship. The two countries established a Strategic Framework for Cooperation on securing uranium, metals, permanent magnets, and critical mineral supply chains, which is designed to facilitate two-way investment in this vital sector and serve as a "cornerstone" of the bilateral strategic partnership. Additionally, the U.S. Department of Defense (recently renamed the Department of War) also announced that it will finance a 49 percent equity stake in a new rare earths refinery in Saudi Arabia. Given the kingdom’s substantial reserves of heavy rare earth elements, this partnership between the Department of War, Maaden, and MP Materials will play a critical role in reducing dependence on China, particularly following a year of pronounced volatility in global access to heavy rare earths.

Q1: Why is U.S.-Saudi minerals cooperation important to reducing China’s leverage with heavy rare earths?

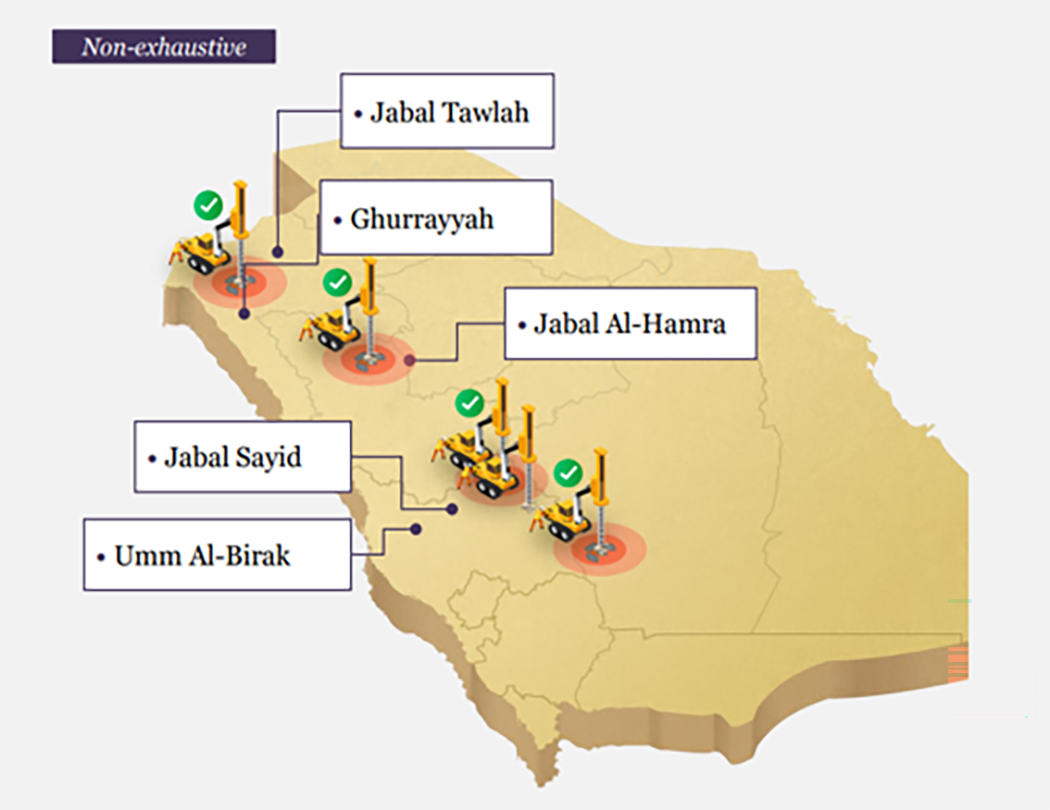

A1: Saudi Arabia is home to one of the world’s most valuable deposits of rare earth elements (REEs). According to estimates received from the country’s Ministry of Industry and Mineral Resources, the Jabal Sayid deposit—located approximately 350 kilometers northeast of Jeddah—is believed to hold the fourth most valuable reserves of REEs globally. It boasts an estimated 552,000 tons of heavy rare earths, including dysprosium and terbium, and an additional 355,000 tons of light rare earths such as neodymium and praseodymium. Moreover, unexplored adjacent deposits could yield even greater supplies, further strengthening Saudi Arabia’s strategic position in the global market for critical minerals.

Source: Maaden.

These reserves of heavy rare earths are of critical importance to the United States, given that it primarily produces light rare earths and remains dependent on imports for heavy rare earths. Beijing has long recognized this dependency and leveraged it to its geopolitical advantage. Over the past year alone, China has repeatedly tightened export controls on heavy rare earths, triggering high-stakes negotiations with the United States in South Korea, the United Kingdom, and Switzerland. The stakes are profound: Heavy rare earths are core inputs for some of the United States’ most advanced defense capabilities, including F-35 fighter jets, Virginia- and Columbia-class submarines, Tomahawk missiles, radar systems, Predator drones, and the Joint Direct Attack Munition series of precision-guided weapons Their importance extends far beyond defense; they are also foundational to critical civilian technologies, from automotive semiconductors to MRI machines and cancer-treatment systems.

Q2: How does the new joint venture between the U.S. Department of War, MP Materials, and Saudi Arabia’s Maaden advance U.S.-Saudi strategic cooperation and reshape global rare earth refining?

A2: The U.S. Department of War, MP Materials, and Saudi Arabia’s Maaden have announced a new joint venture to construct a rare earth refinery in the kingdom. Maaden is 67 percent owned by the Public Investment Fund, the kingdom’s sovereign wealth fund. It has rapidly ascended the global mining ranks and is now one of the 10 largest companies in the world by market capitalization.

Under the agreement, the Department of War will fully finance the U.S. side’s 49 percent stake, while MP Materials supplies the technical expertise; Maaden will hold the remaining 51 percent equity. The new refining facility will leverage Saudi Arabia’s low-cost energy, robust infrastructure, and both domestic and international feedstock to produce separated light and heavy rare earth oxides for defense and industrial supply chains in the United States, Saudi Arabia, and allied nations. The partnership broadens and deepens U.S.-Saudi strategic cooperation, marking a significant move toward diversifying rare earth refining away from China.

Q3: How is Saudi Arabia positioning itself to become a more influential and dominant player in the global critical minerals landscape?

A3: Under Vision 2030, Saudi Arabia is rapidly transforming its mining sector into a central pillar of economic diversification. The kingdom has rapidly emerged as a top global destination for exploration, attracting more than $140 million in investment in 2024 alone. Exploration licensing has accelerated rapidly as well—rising nearly fourfold from 224 licenses in 2015 to 816 in 2023—underscoring Riyadh’s determination to unlock and commercialize its geological potential. The estimated value of the kingdom’s mineral reserves has surged from roughly $1.3 trillion in 2016 to about $2.5 trillion in 2024, reflecting the discovery and prioritization of high-value resources, including rare earths.

Saudi Arabia is also rapidly building out its midstream and downstream capabilities, with the goal of becoming one of the world’s top seven mineral processors by 2030—an outcome that would help reshape global supply chains by reducing China’s dominance in midstream processing. Saudi Arabia possesses several key advantages that position it to lead in developing commercially viable processing.

First, it benefits from abundant and cost-effective energy—a crucial factor given that separating rare earths consumes between 9 and 13 times more energy than their extraction. Saudi Arabia’s energy advantage extends beyond its vast fossil fuel resources: The country has made significant investments in renewable energy and boasts some of the world’s lowest energy costs. For example, the Al Ghat wind project holds the record for the world’s lowest levelized cost of electricity (LCOE) from wind power—just 1.6 cents per kilowatt-hour (kWh). Just behind it is the Wa’ad Al Shamal wind project, with the second-lowest LCOE globally, at 1.7 cents per kWh. Moreover, Saudi Arabia claims the lowest LCOE for solar photovoltaics worldwide.

Second, Saudi Arabia offers a highly favorable regulatory landscape. It has introduced a modern regulatory framework to accelerate the development of its mining sector and support its broader critical minerals ambitions outlined in Vision 2030. In 2021, Saudi Arabia enacted the Mining Investment Law—a sweeping set of reforms aimed at attracting investment and streamlining processes in the mining industry. According to Bandar Alkhorayef, minister of industry and mineral resources, mining licenses in Saudi Arabia can be secured within 180 days—in stark contrast to the United States, where it typically takes 7–10 years to obtain the necessary permits to bring a mine into operation.

And third, Saudi Arabia is well-positioned to develop a processing hub capable not only of handling its own domestically-sourced concentrates, but also to accept rare earth feedstocks from allied countries. This strategic role helps bridge the global processing gap while reinforcing reliable supply chains among friendly nations. Importantly, Saudi Arabia will be the closest processing hub for 5 of the 10 countries that received the highest share of rare earth exploration by investment value in 2024—Malawi, Namibia, South Africa, Uganda, and Saudi Arabia itself—positioning the kingdom as a vital link in the global rare earths supply network.

Ultimately, Saudi Arabia’s mineral-processing ambitions are poised to extend well beyond rare earths. The kingdom is positioning itself to become a global hub for refining and midstream capacity across a broader suite of critical minerals—from nickel, aluminum, gallium, copper, lithium, and phosphates.

Q4: What civil nuclear cooperation agreement has the United States and Saudi Arabia struck—and why does it tie directly into rare earth security?

A4: The United States and Saudi Arabia announced a joint declaration finalizing negotiations on civil nuclear energy cooperation. This agreement establishes the groundwork for a long-term, multibillion-dollar nuclear partnership with the kingdom; affirms that the United States and U.S. firms will be Saudi Arabia’s preferred partners for its civilian nuclear program; and guarantees that all collaboration will follow rigorous nonproliferation standards.

The nuclear cooperation agreement is significant given that Saudi Arabia’s rare earth deposits occur in tandem with its uranium resources. Jabal Sayid alone has approximately 31,000 tons of uranium. Those uranium reserves uniquely position the kingdom to develop the nuclear fuel cycle, supporting its domestic energy strategy while opening the door to potential exports to the United States. At present, Russia and China control over half of global uranium enrichment capacity, a sectoral dominance that poses a serious risk to U.S. energy security. The United States imports most of its uranium, with nearly 30 percent coming from Russia as of 2022. In May 2024, then-President Biden signed the Prohibiting Russian Uranium Imports Act to lessen dependence on Russian nuclear fuel and support domestic uranium production. This law bans imports of Russian low-enriched uranium from August 11, 2024, through December 31, 2040, though it permits waivers until the end of 2027 if there are no viable alternative sources or if imports are deemed in the national interest. Saudi Arabia could serve as a critical supplier of uranium to the U.S. nuclear industry.

Discussions on nuclear cooperation between the United States and Saudi Arabia have been ongoing for years. In 2008, they signed a memorandum of understanding (MOU) to collaborate on peaceful nuclear applications, including medicine, industry, and electricity generation. Subsequent U.S. administrations continued exploring a formal bilateral nuclear cooperation agreement. Talks in 2012 and 2018 focused on a potential “123 agreement,” which would specify the terms, scope, and duration of peaceful nuclear collaboration while incorporating nonproliferation measures. These agreements require the president to certify that they enhance U.S. defense and security interests and are subject to a 90-day continuous session review by Congress. Unless Congress passes a resolution of disapproval, the agreement automatically enters into force at the end of the review period. As of August 2020, the U.S. Department of State reaffirmed its commitment to negotiating an agreement with robust nonproliferation safeguards to enable cooperation between the U.S. and Saudi nuclear sectors. Nuclear cooperation was also expected to be part of the broader normalization talks among the United States, Israel, and Saudi Arabia, but was put on pause after the October 7, 2023, Hamas attack on Israel.

In April 2025, U.S. Secretary of Energy Chris Wright spoke at a press conference in Riyadh, announcing that the United States and Saudi Arabia plan to sign an MOU in the future to promote collaboration across crucial energy sectors. Wright noted, “For a U.S. partnership and involvement in nuclear here, there will definitely be a 123 agreement. . . . There’s lots of ways to structure a deal that will accomplish both the Saudi objectives and the American objectives.”

Now that the United States and Saudi Arabia have reached a deal on civil nuclear cooperation, the next step is to formally transmit a Section 123 Agreement to Congress.

Q5: How has the U.S.-Saudi relationship evolved from its historic oil-for-security foundation to a new phase centered on critical minerals and future strategic industries?

A5: Natural resources have long underpinned the U.S.-Saudi bilateral relationship. Born in the aftermath of World War II, the alliance was built on the essential nexus between oil and security. In 1945, President Franklin D. Roosevelt and King Abdulaziz Ibn Saud met aboard the USS Quincy, forging the landmark “oil-for-security” partnership: The United States would provide military protection in exchange for reliable access to Saudi oil reserves. Through the 1970s and 1980s, U.S. companies invested heavily in Saudi Arabia’s oil sector, solidifying deep commercial ties. In the 1990s and 2000s, the United States maintained its role as Saudi Arabia’s principal military and economic partner, and Saudi Arabia consistently ranked among its top oil suppliers. Even as the United States has increased its domestic energy production and reduced dependence on imported oil, Saudi Arabia remains an essential global swing producer. Today, the U.S.-Saudi alliance is entering a new phase, expanding beyond oil to embrace critical minerals as the backbone of future national, energy, and economic security alignment with the United States.

Gracelin Baskaran is director of the Critical Minerals Security Program at the Center for Strategic and International Studies in Washington, D.C.

If you are interested in learning more about this topic, explore CSIS’s Executive Education course Building Critical Mineral Security for a Sustainable Future.

Report by Gracelin Baskaran and Meredith Schwartz — July 28, 2025

Video — July 30, 2025

Commentary by Gracelin Baskaran — December 5, 2023