The Future of Global Energy: Insights from the 2026 Statistical Review

July 21, 2026 • 12:00 – 12:45 pm EDT

Photo: JUNG YEON-JE/AFP via Getty Images

On March 11, 2020, Covid-19 was declared a pandemic by the World Health Organization. Uncertainty reigned. But soon thereafter, in perhaps the greatest intellectual explosion of futures thinking in human history, governments, businesses, institutions, and individuals asked what this shift would mean for them. How would the SARS-CoV-2 virus reshape our society and our lives in the days, weeks, months, years, and even decades to come?

In an especially prescient piece about the future course of the public health challenge, CSIS’s J. Stephen Morrison and Anna Carroll observed, “Pandemics change history by transforming populations, states, societies, economies, norms, and governing structures.”

With the benefit of four months of study and reflection, this analysis is an attempt to think systematically about how Covid-19 has fundamentally changed major global trendlines out to 2050. This research was conducted through the analytic framework of the Seven Revolutions initiative, a macrotrends assessment that is continually updated with a 30-year time horizon.

The net assessment is that Covid-19 is highly disruptive in the near term and highly unpredictable in the medium to long terms across every macrotrend area analyzed in this paper. It is at once an accelerant, an irritant, and a stress test. Its effects will ebb and flow and hit various nations and populations in different ways and on differing timescales. It is this unevenness and unpredictability that defines the challenges ahead, as explained in greater detail in this scenario analysis co-authored with CSIS’s Sarah Ladislaw. While there is high confidence in the assessment of first-order outcomes from this crisis, the second-order outcomes of events just now unfolding can only begin to be anticipated. For example, while the authors of this brief made predictions in early April that Covid-19 would likely accelerate global protest movements, it was never anticipated that by late May the United States would be the epicenter of a global protest movement and the focus of those protests would be police brutality and systemic racism. Many future such surprises should be expected, but the identifiable changes underway should still be cataloged to the best possible extent. Covid-19 marks the start of an era of continuous, rapid change.

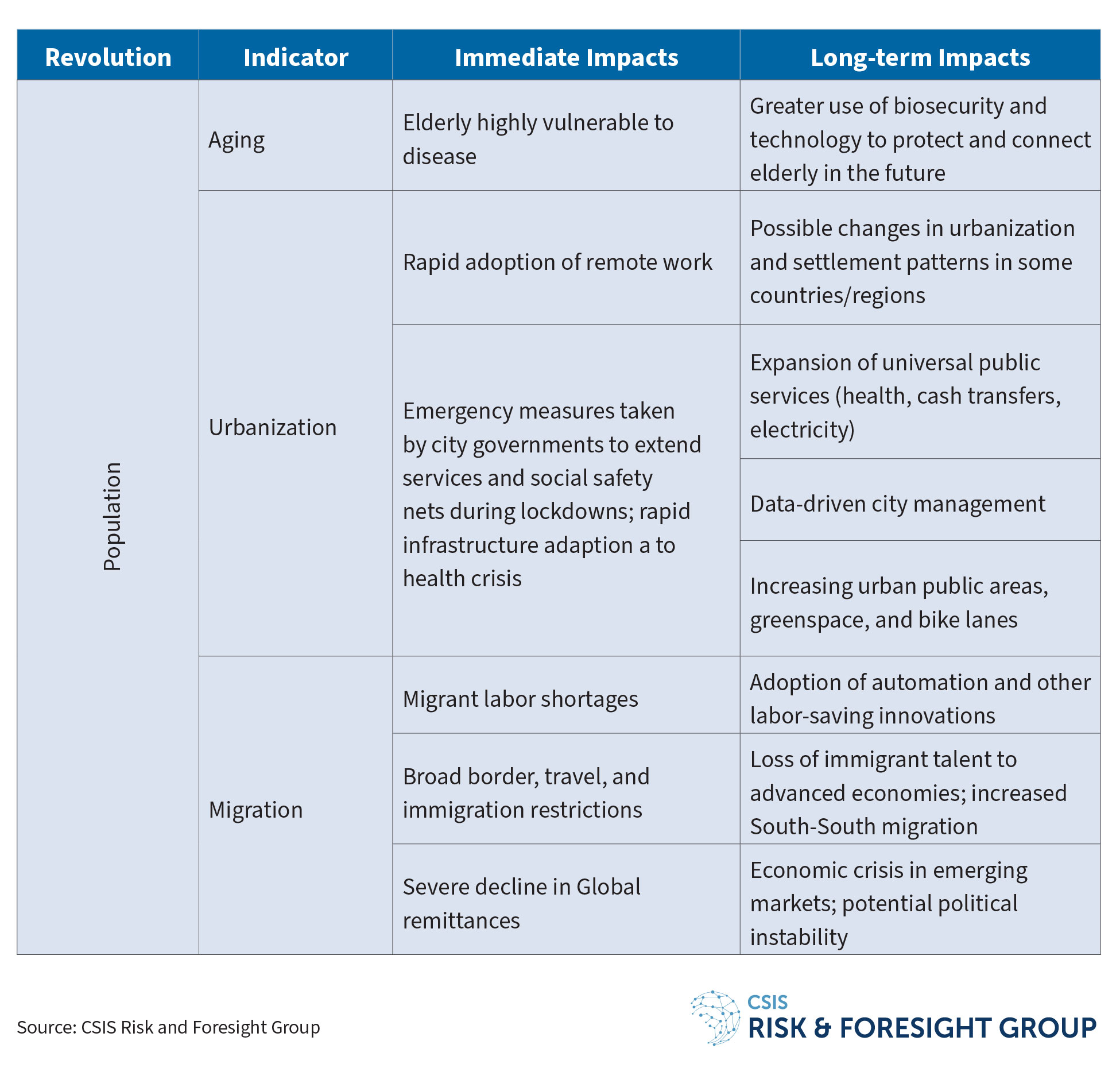

The virus infected the human population at a historic transition in its demographic structure. This year, for the first time ever, the number of people aged 60 years or older outnumbers people 5 years old or younger worldwide, with aging populations concentrated most heavily in high-income countries. Unfortunately, the virus is uniquely dangerous to this growing elderly cohort. For example, more than half of Covid-related deaths in the United States have been among those over the age of 65, and around 85 percent in Italy have been among people aged 70 years and over. Eldercare facilities have proven especially vulnerable to outbreak clusters and high mortality.

The higher risk posed to the elderly raises the question of what can be done to better ensure their health and safety not just in the course of this pandemic but in the event of likely future epidemics. The pandemic has also highlighted the degree to which older citizens remain important contributors in the workforce as caregivers and as social lynchpins within families and communities. Over time, the true costs of this loss of human life will be absorbed and likely change the approach to eldercare, including increased biosecurity and use of technology to help keep the elderly safer and more connected.

Pandemics have long changed cities. The advent of street cleaning, hospitals, water drainage systems, garbage disposal systems, and secular public health systems all arose from urban responses to past disease outbreaks.

Lasting changes to cities worldwide in the course of this pandemic are already underway. Urban planners are reorganizing public spaces to emphasize green spaces, outdoor recreation areas, and pedestrian zones. And while public transportation usage has broadly plummeted in partial favor of cars as a result of Covid-19—for example, New York City public transit is down 62 percent since January while driving is up 16 percent—cities from New York to Paris to Bogota to Vilnius have taken steps to increase bike lanes and minimize vehicle traffic. Urban communities are also increasing universal access to public services such as health care and electricity, without which some people could not comply with public health measures such as lockdown orders. Additionally, governments in places such as Kenya, Afghanistan, India, and South Africa are taking steps to authorize and upgrade informal settlements and slums and connecting new sanitation, electric, and health services to previously unserved areas in the process. Elsewhere, governments in countries such as Colombia, Spain, Togo, and South Africa have stepped up emergency cash transfers and universal basic income measures, creating a new social safety net overnight. In parallel, major technology firms such as Tencent and Qualcomm have announced plans to help cities improve access to services through “smart city” technologies.

The pandemic also has driven home just how vulnerable high-density populations are to the spread of disease. While 55 percent of the world’s population now lives in urban areas, that percentage is forecast to grow to 66 percent by 2050, with much of this growth in the developing world. The Covid-19 pandemic likely originated in Wuhan, China, a megacity of 11 million people. It then decimated the New York metropolitan area—another megacity. Public health and disease surveillance will be a critical consideration for cities of the future.

Moreover, the very future of cities has been thrown open to question in some regions. Take, for example, the acceleration of the adoption of remote work. In the month of March 2020, the number of Americans working remotely doubled to 62 percent. Emerging research indicates that remote work could lead to significant productivity gains, and major companies such as Twitter have already announced plans to make remote work options permanent. This has opened to question the importance of workplace proximity, which could in turn decrease the importance of cities as job hubs, allowing white-collar services workers in particular to abandon high-cost urban hubs for less expensive destinations—an especially important consideration given a potentially slow economic recovery disrupting wage growth. There are limited indications such a trend may already be underway, with 27 percent of home searchers looking to move to another metropolitan area in April and May according to Redfin, a real estate broker. Areas previously struggling with growth may also see new opportunity. For example, some smaller U.S. cities are incentivizing relocation of remote workers, with Topeka, Kansas, for example, offering $15,000.

Last year, the United Nations reported that the global migrant population had increased 32.6 percent to 272 million over the past decade—a population level previously forecasted to occur in 2050. As noted by CSIS’s Erol Yayboke, the pandemic has had an outsized impact on this demographic of global migrants. Most of the world’s population now faces obstructed movement, with over 220 countries, territories, or areas having implemented some type of travel or immigration restrictions. How, when, and if these new restrictions to global migration are reversed is unclear, but even their short-term imposition is reshaping the future in many ways.

Pandemic-induced labor shortages in countries dependent on migrant labor will likely accelerate automation and technological innovation. Lasting macroeconomic consequences are also intensifying by the day. Developed economies may lose out not only on labor but also in terms of entrepreneurship often brought by recent immigrants. Furthermore, developing economies and migrant communities are losing remittances at a massive scale. The World Bank already estimates a 20 percent decline in global remittances, which are vital to the economies of countries such as India and Nigeria. The loss of remittances will increase the risks of political instability and degradation of governance in many regions. Migration flows may also increase in the Global South as developed countries sustain border and immigration restrictions after the immediate health crisis passes.

The pandemic brought immediate, seismic disruption to energy markets as broad swathes of the global economy shut down overnight. U.S. petroleum demand fell by over 25 percent, and gas sunk to its lowest level since the 1970s. Public transportation demand is down about 70 percent in San Francisco and Seattle and 62 percent in London. In Italy and France, demand declined by more than 80 percent across all major cities between mid-March and early May but then steadily increased over recent months as the countries started recovering from the pandemic. In Washington, D.C., for instance, driving only reached pre-pandemic levels in early July, while public transportation usage remains 64 percent lower than the baseline. Additionally, declining global goods trade—on track to decrease by 20 percent in 2020—has reduced energy-intensive shipping. Globally, energy demand saw its steepest decline in 70 years, and continued reduction in demand may prove durable if changes in overall energy usage driven by factors such as continued remote work persist. Depending on how lasting certain changes are, the pandemic may have made the “peak oil” demand arrive 15 years earlier than expected.

Energy market price fluctuations, exacerbated by global oversupply and a breakdown in OPEC-Russia relations, may also have long-term consequences. For instance, low petroleum prices incentivize fossil fuel use and could delay the deployment of electric vehicles. On the other hand, the pandemic has triggered a 20 percent decline in overall energy investment—equivalent to $400 billion—while utility-scale investment in renewables has proven resilient. Lower demand and investment provide space for renewable energy technologies and cost-efficiency to catch up and capture a greater share of returning investment. Additionally, a major wildcard is that governments and institutions are considering sustainable, green economic recovery policies that could dramatically reshape energy markets.

Climate change and pandemics are inherently linked, and as humanity encroaches further on wilderness areas, the United Nations expects a steady stream of animal-born “zoonotic” viruses to leap into human populations in the years ahead. Wildlife and livestock already serve as the source of 60 percent of viruses infecting humans, and of all emerging infectious diseases, 75 percent originate in animals. Key triggers for epidemic zoonoses include climate variability, flooding, and other extreme weather events linked to climate change. Climate change has also increased the geographic area in which a number of currently active zoonotic diseases regularly infect humans.

Despite the clear and present dangers highlighted by this pandemic, steps to combat climate change and implement more sustainable agricultural practices have stalled. The pandemic has absorbed international media and policymaker attention for months, distracting from the urgent need for climate action. In May, despite dramatic decreases in energy usage due to economic shutdowns, the world still saw its highest carbon dioxide levels in human history. In November, some 196 countries were to follow up their 2015 Paris Agreement commitments and release new individual plans to reduce carbon emissions. Instead, the COP26 global climate conference has been postponed. Meanwhile, the grassroots climate activism that rocked the world over the past few years has retreated to its digital roots during the pandemic, with climate activist Greta Thunberg encouraging activists to take up their work online.

However, the lasting outcomes from the pandemic on the future course of climate change are yet to be written. The speed and extent of the global economic and public health response to the virus has been taken by many activists to signify that global mobilization on policy issues is possible, even when it requires historic disruptions to economies and livelihoods. The European Union and South Korea have given special consideration in their economic recovery and stimulus plans around a “green recovery,” and it is conceivable that other countries will follow suit.

The global food system feeds four-fifths of the world’s population and has been severely disrupted by Covid-19. CSIS non-resident Senior Advisers Julie Howard and Emmy Simmons identify a series of shocks to the global food system: (1) transportation and economic restrictions have complicated the movement of agricultural goods; (2) export bans and border closures have exacerbated supply chain disruptions; (3) limitations on labor, services, and agricultural inputs have reduced overall production; and (4) job losses have reduced food purchasing power, especially among the poor. Collectively, these may leave lasting structural changes as consumer tastes adjust, including restaurant adaptation and increasing use of food delivery services.

Prior to the pandemic, the transition of agriculture to a data science was already accelerating, with the market for AI in agriculture expected to grow by over 25 percent a year between 2020 and 2026. New forms of automation were also underway, including significantly increased deployment of unmanned and autonomous systems in developed and emerging markets alike. Automated agricultural production is already seeing accelerated gains due to pandemic safety problems and labor shortages. While certain agricultural sectors are much easier to automate than others, adoption of robots and data-driven agricultural practices is accelerating.

Mounting food insecurity poses risks to political stability, and food prices are directly linked to institutional breakdowns and mass protests. Food-related protests have occurred in multiple regions over past months. Given the political stakes, governments have moved to secure food supplies through measures such as increasing domestic production, diversifying food supplies to additional countries, and securing agricultural labor. The UN Food and Agriculture Organization (FAO) already forecasts increasingly localized vegetable production and more interregional food markets to shorten food chains. Increasingly, food production could occur within cities themselves as urban farming increases, even down to the household level. Demand has increased dramatically for seeds, chickens, and hydroponic and other equipment for vertical and indoor farming. Increased scrutiny of the public health impacts of meat consumption in China and beyond also raises questions about whether the pandemic-linked increase in plant-based food consumption will last in the long term as consumers develop a taste for meat alternatives—currently a hot bet for venture capital.

Covid-19 is likely to accelerate the adoption of robotics, among other forms of automation. In a pre-Covid-19 study, Oxford Economics forecast that 20 million global manufacturing jobs could be replaced by robots by 2030. The National Bureau of Economic Research and the W.E. Upjohn Institute for Employment Research have found that labor-replacing automation spikes during economic recessions, with the largest effect on lower-skilled jobs.

During the pandemic, robots have been widely deployed in delivering services, disinfecting public spaces, and assisting health workers in order to mitigate virus spread. In the health care industry, the pandemic is accelerating the incorporation of robots in daily hospital operations and driving developments in applications that could help with more effective diagnosis, screening, and patient care. For example, Chinese researchers are designing new robots that remotely take blood samples and perform mouth swabs.

In the grocery industry, robots have been rapidly deployed to clean floors, stock shelves, and provide “contactless” alternatives by delivering groceries. In the retail industry, companies such as Walmart and Amazon are implementing robotic fulfillment facilities or microfulfillment centers at a higher rate than before the pandemic to respond to the surge in online orders. Ground and aerial robots are also playing a notable role in managing the crisis in 21 countries by providing thermal imagery to identify infected citizens, enforcing quarantine measures, and broadcasting public service messages.

Additive manufacturing (3-D printing) has shown promise in responding to urgent needs during the Covid-19 crisis, especially highlighting its value to the health care industry. As medical supply chains struggle with global disruptions and emerging needs, additive manufacturing has proven highly agile in producing necessary components such as anatomical structures, ventilators, prosthetics, and personal protective equipment. Researchers and companies in the United States and elsewhere turned to additive manufacturing to address shortages as the crisis intensified. Royal DSM launched the UNITE4COVID platform, highlighted on the World Economic Forum’s Covid Action Platform, to support a united effort by 3D-printer manufacturers and address shortages. The U.S. Food and Drug Administration, National Institutes of Health, and Department of Veterans Affairs formed a public-private partnership with additive manufacturing companies to address device shortages, including personal protective equipment. In another example, China is using additive manufacturing to mass produce safety googles to address a serious shortage in the country.

Despite a higher rate of digitalization during Covid-19, including through work-from-home infrastructures, VPN networks, and collaboration tools such as video conferencing, the Internet of Things (IoT) itself is largely unaffected by Covid-19. IoT includes 1 trillion or more connected devices in the world today, spanning sectors and industries and representing the convergence between the physical and digital worlds. Despite Covid-19 moving many social and commercial activities online, IoT devices are running and sending similar amounts of data as they had prior to the crisis (a sign, more than anything, of the already breakneck pace of use).

But the long-term impact of Covid-19 on IoT analytics is still notable, especially in the health sector. Businesses and governments who have increased their reliance on the internet, IoT analytics, and digital devices during the crisis will maintain higher levels of digitalization after the pandemic retreats. One example is the increasing demand for digital portals in interactive health care, with some online services currently reporting a 500 to 600 percent increase in telehealth usage. Unlikely to return to its low-technology past, medium-to-high consumer demand for telehealth and virtual consultations will increase reliance on IoT. Furthermore, similar to how IoT was used to detect emerging public health crises such as Zika and H1N1, IoT applications have been directly employed in the fight against Covid-19 to track virus spread and assist with contact tracing by analyzing and sharing real-time data with global medical systems and monitoring tools, including the booming area of consumer wearable devices.

By 2030, AI could comprise $15.7 trillion of the world economy, and there is evidence that Covid-19 is accelerating the overall pace of innovation in the field. The pandemic will accelerate the infusion of AI into health care perhaps more than any other sector. AI has been paired with robotics to create autonomous systems capable of interacting with the physical world and used to predict the spread of the virus, monitor infection rates, conduct contact tracing, and inform policy decisions on reopening. The pandemic has also accelerated the expanded use of digital assistance such as chatbots: in health care applications on the WHO and CDC websites; in banking and e-commerce to provide conversational banking with PayPal (e.g., to handle 65 percent of customer inquiries); and in the call center services industry. Researchers are also using machine learning to recognize virus patterns, allowing for early detection of disease.

Simultaneously, Covid-19 has highlighted the challenges inherent to AI and that society remains decades away from automated systems that could independently run themselves. Evidence suggests that inexplicable crisis-induced changes in human behavior, such as panic shopping of toilet paper and surges in purchases of garden equipment, are simply confusing for AI. This might prompt developers to train future AI on understanding past crisis events such as the Great Depression and the Global Financial Crisis in order to better predict future human behavior. The wild swings in the stock market, particularly in the March to April timeframe, may have been largely the result of AI algorithms overreacting and overreacting to a vastly different strategic environment beyond any previous data they could mine for context.

Covid-19 has likely accelerated what was already on course to be the biotechnology century. Biotechnology is at the cutting edge of the Covid-19 response, enabling rapid progress and new approaches in diagnostics, therapeutics, and vaccine developments. The global health crisis has put into context exactly what the stakes will be for achieving leadership in biotechnology and the related implications for economic competitiveness and national security. Convergent technologies such as AI and cloud computing are also further accelerating progress in this field. Even prior to the pandemic, global synthetic biology companies were expected to reach a market capitalization of almost $20 billion by 2022. Amid the pandemic, the market capitalization of some biotech companies working to develop vaccines is surpassing all expectations.

Synthetic biology companies are racing to find a Covid-19 vaccine as well as other vaccines and therapeutics effective against current and future pathogens. Bioengineering tools have already enabled several companies such as Moderna Therapeutics, CureVac, and Inovio Pharmaceuticals to rapidly develop vaccines and speed toward human testing faster than traditional approaches. Distributed Bio is attempting to develop a universal flu vaccine using computational immunology. GenScript is offering a high-tech test that uses DNA tools to detect and measure the amount of coronavirus in blood samples. SwiftScale Biologics is using cell-free biotechnology to accelerate Covid-19 therapeutics and produce antibodies up to 10 times faster than other current methods.

Nearly half of the world’s population is now online, and by 2030 this number is likely to be close to 100 percent. Covid-19 has proven digital connectivity a vital link amid lockdowns and social distancing. And while internet connectivity has been a net social good, it has also enabled the expansion of security and surveillance measures by governments and companies, likely with lasting implications for privacy and civil liberties.

Authoritarian and democratic governments alike in at least 25 countries have expanded their use of surveillance technologies in response to the pandemic, including using GPS tracking to enforce compliance, collecting cell phone data from telecom companies to gauge adherence to public health guidelines, and publicly providing what in other times would have been considered confidential information regarding those infected with Covid-19. Private companies have rapidly expanded the development of health surveillance technologies. Apple and Google are collaborating on a contact-tracing app that uses Bluetooth to determine others’ past proximity to infected individuals days or weeks prior to their diagnosis. Alibaba, a Chinese e-commerce giant, designed a health tracing feature that tracks the health status of individuals and automatically shares their data with law enforcement authorities. Privacy International’s Tracking the Global Response to Covid-19 project catalogs a wide array of measures that are expanding surveillance to purposes beyond public health, including efforts to create immunity passports and attempts by law enforcement to use contact-tracing apps in investigations.

Similar to the persistence of security systems deployed after the September 11, 2001 attacks in the United States and elsewhere, surveillance measures to combat Covid-19 are likely to outlast the crisis. Surveys by Gallup and KPMG suggest that during the pandemic, people have unsurprisingly become more concerned about health security and less concerned about privacy than before the pandemic’s onset. Ron Deibert, a leading expert on mobile phone surveillance, said the pandemic is creating a “9/11 on steroids,” with grave abuses of power that could also become the new normal.

The digitalization of commercial and social activities, industries, and services under Covid-19 and the growing adoption of technologies such as IoT and AI will lead to global data growth. As the virus and lockdown measures push daily activities online, millions are turning to the internet and technology for entertainment and work, causing unprecedented spikes in data traffic and in-home data usage and showing just how vital digital infrastructure is to the future of societies and economies.

Compared to the same time in March 2019, in-home data usage increased by a total of 18 percent in 2020, and average daily usage rates increased by 38 percent to 16.6 gigabytes compared to 12 gigabytes in 2019. Total internet use and traffic have also spiked by as much as 70 percent. Telecommunication companies such as Vodafone are reporting a 50 percent rise in internet use as Covid-19 places greater demand for home networks. Several technology platforms are also seeing major increases in usage. The number of daily Zoom users more than quadrupled, up 378 percent from last year, while data usage itself has doubled. Communications apps including WhatsApp and Microsoft Teams are also seeing a 45 percent increase in traffic. All of the above suggests that while it is possible that data use of some technologies will decrease after Covid-19 retreats, this moment may nevertheless accelerate the growth of data globally.

As of January 2020, 49 percent of the planet’s population—3.8 billion—are active social media users, 9 percent (321 million new users) higher than in 2019. This suggests that the number of social media users will be significantly higher by 2050, regardless of Covid-19’s impact. But the pandemic is in the immediate term increasing time spent on social media and exposure to false news. Polling by Pew Research suggests that people who primarily get news through social media are more likely are more likely to report encountering misinformation about the pandemic. Furthermore, there is growing evidence that social media platforms are emerging as critical to authoritarian efforts to control the information sphere.

Since the onset of Covid-19, disinformation (intentionally false) and misinformation (inadvertently false) directly tied to the virus have proliferated. By no means a new phenomenon, fake information has already been supercharged in scale and speed by information technology, a next generation of “deepfakes” or synthetic media, and, sometimes, government actors seeking to distort the truth. Past disease outbreaks highlight the troubling nature of health misinformation. During the 2016 Zika outbreak, misinformation about the virus greatly outpaced credible sources of information. This was further complicated by the ability of false news to spread farther, faster, and more broadly than credible news.

This trend is likely to persist regardless of Covid-19 given the struggle of responsible states, civil society, multilateral organizations, and private industry to stay ahead of proliferating misinformation. However, what the World Health Organization has described as an “infodemic” has become yet another element of geopolitical competition. China, Russia, and other nations are using a range of platforms to spread disinformation, sow discord and spread fear in the United States and Europe, and deflect from their own struggles with the pandemic. In early February, Russia launched a coordinated campaign to spread Covid-19 misinformation, at times promoting conspiracies that the United States engineered the virus. China has been overtly aggressive and confrontational in using government-linked accounts to spread conspiracy theories and send disinformation messages directly to Americans’ cellphones, a tactic officials say is a new development. Senior U.S. administration officials and members of Congress have also propagated unsubstantiated theories about the intentional or inadvertent release of the virus from Chinese government laboratories.

Covid-19 has necessitated a hyper-acceleration in the adoption of online education. Many universities and schools around the world have already transitioned to online education in response to Covid-19. While the rapid changes have caused painful adjustments and highlighted shortcomings in unequal access to technology, a new hybrid model of education that synergizes the advantages of in-person education with online learning likely will be sustained.

Since 2012, e-education has been making steady gains. In 2018, the proportion of U.S. students enrolled in at least one online class had risen to over 34 percent. Several large public universities have adopted a hybrid education model: Arizona State University nearly doubled its online enrollment from 2015 to 2018 while still controlling costs, and Florida International University increased online enrollment by 44 percent. More broadly, university enrollments in the United States have fallen by 11 percent over the past eight years and may possibly decline more without the affordability and accessibility of online education. E-education has the potential to reduce tuition because online and technology-enabled systems require fewer expenses for maintaining buildings and paying staff and faculty and allow for larger classes.

The pandemic may force a better understanding of institutional factors that limit the effectiveness and reach of online education, such as a lack of administrative and marketing support, a lack of understanding of online learning styles by instructors and faculty, and the negative perception of online degrees by employers. It may also drive universities to reconsider tuition rates due to dropping student demand as a result of an arguably less desirable education experience. This mass ongoing experiment may also reveal the limits of online education, including for K-12 students.

The pandemic represents the largest worldwide economic shock in memory—outstripping the Global Financial Crisis in its sweep and future uncertainty. The World Bank’s June 2020 Global Economic Prospects paints a bleak picture of the current and future world economy, forecasting a 5.2 percent contraction in the global economy in both emerging markets and developing and developed economies. It is the first time in at least 60 years that the two groups of countries have experienced a recession as a group, painting a picture of a wide, deep, and synchronized global economic crisis. Economists and central banks worldwide forecast a slow recovery as they enact extraordinary stimulus and stabilization measures, with IMF Economic Counsellor and Director of the Research Department Gita Gopinath stating that this was “the worst recession since the Great Depression, and far worse than the Global Financial Crisis.”

Even with such a dire outlook, the demise of globalization has been predicted for decades without coming to pass. Despite the massive blow to global connectivity and trade absorbed amid Covid-19, globalization is certain to endure and could bounce back sooner than expected. The more important questions are how globalization will change and what the path to recovery could look like. As countries hide behind their borders and raise tariffs to protect teetering markets, foreign trade flows have fallen precipitously. The World Trade Organization projects a volume of global goods exports commensurate with levels in the late-2000s.

The most consequential outcome of Covid-19 could be an intensification of national interests superseding free market incentives in guiding supply chain formation. Covid-19 was likely the largest international market shock in terms of restricting supply in the free flow of goods since the Arab Oil Embargo in 1973, in this case related to medical supplies such as ventilators and personal protective equipment. That shock intersected with existing supply chain tensions related to continued trade and export restrictions between the United States and China. Lasting national restrictions and government incentives to spark domestic growth of key industries could potentially fragment and regionalize supply chains, leading to reshoring or nearshoring of production in key markets and a growing fragmentation between Asian and non-Asian markets.

Emerging markets are also contending with economic disruptions that could cause deep, lasting damage. For example, oil, tourism, and remittances are three of the main economic drivers in numerous emerging markets, and all are being severely negatively affected by Covid-19. In Nigeria, Africa’s largest economy, oil accounts for 90 percent of exports and two-thirds of government revenue, two-thirds of which services debt. Nigeria is not alone in facing such mounting pressures. The IMF found public debt increased to over 122 percent of GDP in advanced economies, 62 percent in emerging markets, and 47 percent in developing countries. Fifteen African nations are expected to spend more servicing debt than on medical response to Covid-19, and countries such as Lebanon have already defaulted on Eurobond debt. Argentina is headed toward its ninth default. These economic crises could in coming years create greater political instability in countries or entire regions.

Other countries around the world will soon face similar debt challenges as credit markets dry up and refinancing capacity proves elusive. The crucial ingredient—foreign direct investment (FDI)—has all but dried up. The UN Conference on Trade and Development forecasts that FDI flows will decrease by up to 40 percent this year and a further 5 to 10 percent next year and are not likely to begin recovery until 2021.

Unsurprisingly, inequality is likely to increase both globally and within individual nations as the pandemic disproportionally impacts poorer economic strata. In an analysis of five twenty-first century epidemics, the IMF found evidence that low-skilled and low-wage workers are disproportionally impacted by outbreaks. Gini coefficients—a commonly-used measure of wealth distribution in society—has increased following past pandemics, indicating greater wealth disparity during recovery. Job losses have been unequally distributed as well. The employment of those with advanced education was not significantly impacted, but for those with little or no formal training, employment averages fell by more than 5 percent, even after five years of recovery.

As a result, global poverty, which had been trending down since 1998, will increase. Lost income among the world’s poorest individuals due to the pandemic is estimated to top $550 million per day. A recent report from the United Nations University suggests that the number of people living below the global poverty line could exceed 1 billion, up from an estimated 641 million in 2018.

Labor markets are in disarray around the globe. The IMF estimates that 300 million full-time jobs could be lost in the second quarter of 2020. In the retail, service, and hospitality industries, where the majority of low-income jobs are located, pandemic-induced job loss from economic dislocation will continue to be highest.

The pandemic’s economic effects have been felt hardest by those closest to the poverty line as jobs in the “real economy” (i.e., providing physical goods and essential services) disappear due to quarantines and lockdowns. Long term, these workers will experience significant difficulty recovering from the pandemic.

The pandemic will eliminate many of the jobs that these workers had come to rely on as the economic downturn continues to overwhelm small businesses, while big businesses will be able to weather the storm and in some cases expand market share and seize the opportunity to acquire distressed assets. Long-term structural shifts in the economy have included a steady decline in the share of employment by microbusinesses (companies with nine or fewer employees) in the United States. If the Global Financial Crisis serves as any indication, these trends will accelerate. Small businesses accounted for 47.1 percent of national employment but accounted for 64 percent of job loss. The downturn may be even more dramatic during a Covid-19 recession, with the Small Business Administration reporting that “early signs indicate that small businesses have been disproportionally affected across industries [by the Covid-19 pandemic], especially those in the accommodation and food services industry.”

Perhaps the most dramatic economic restructuring will come in the rapid move to online commerce. Compared to May 2019, online spending is up 77.8 percent. Physical currency has been an unintended victim as people rely more and more on cashless transactions. In the United Kingdom during the early stages of the outbreak, 54 percent of consumers stated they were avoiding cash altogether. In the United States, coins are now in short supply for many merchants as customers have stopped putting them back into circulation. Meanwhile, interest in cryptocurrencies is surging. Facebook has intensified efforts to roll out its Libra currency, and China announced trials for its state backed “digital yuan” currency in April, premiering in four cities around the country. Bitcoin’s value has surged since March 15, increasing in price by 75 percent as of July 8.

Digital wallets are already proliferating thanks to apps such as WeChat, but the shift away from currency will likely see increased development and adoption. Bain and Company adjusted their projections, estimating that by 2025 67 percent of all transaction values would be digital, an increase of 10 percent over pre-Covid-19 targets. Shadow banks are another beneficiary of this move away from physical banking, as their flexibility and remote access becomes more and more attractive in a cashless world.

Covid-19 has underscored the reality that health security is national security. The need to broaden the definition of what is meant by national defense is clear. This could in turn give impetus to include other global trends such as migration and climate change in the conceptual bounds of national security as governments seek to renew trust with citizens shaken by the flat-footedness or even incompetence of many countries’ national responses to the pandemic. At the same time, there is a danger, as a report of the CSIS Commission on Strengthening America’s Health Security indicates, that the United States could fall once more into a “cycle of complacency and crisis” that has characterized America’s response to past disease threats. While health security will demand greater investments, growing debt and budget pressures will increase in the slow-growth economic environment that follows.

A recent interview of multiple CSIS scholars concludes that a long-term impact of Covid-19 is likely to be the acceleration of a transition to a more fragmented world order led by neither the United States nor China. This will not necessarily be a multipolar order, because its organizing principles remain unclear. Recent polling has affirmed that both the United States and China are viewed less favorably in light of their responses to Covid-19. Countries across the world are openly questioning the roles of the United States and China in a new world order. It will be increasingly difficult in this global environment for any single country to lead, as nations are poised to pursue their interests on a more ad hoc basis and as multiple powers gain sufficient capacity to influence events. The U.S. system of alliances is likely to remain the most important structure of influence in the world, but other axes and interests will also determine global events.

Gray zone activities—activities below the threshold of armed conflict but outside the usual practice of statecraft—have increased sharply over the past several decades. CSIS’s Gray Zone Project explores the notable uptick in cyberattacks from China, Russia, Iran, and North Korea as well as other tactics such as financial support for proxy conflicts, political and economic coercion, and information influence operations.

As discussed above, Covid-19 has clearly accelerated state competition in misinformation and disinformation. The WHO has described an “infodemic” that has raced ahead of the pandemic, complicating response efforts by promoting false cures, erroneous information, and conspiracy theories. Multiple national country governments have mishandled their own responses to Covid-19 and failed to exercise global leadership on the subject, so they seek to distract by blaming others for elements of that failure. Russia and China have played especially damaging roles, with both launching coordinated campaigns to spread misinformation and alarm globally while promoting conspiracy theories that the U.S. engineered the virus. This has created a vicious cycle of public accusations and counter-accusations—some verifiably false—by U.S. and other country officials.

Further, as CSIS’s Todd Harrison has noted, the extraordinary fiscal impacts of Covid-19 will result in defense cuts around the globe. This could push more countries to lower cost, gray zone approaches to international competition. Budgetary constraints could also create military surprise, as it incents militaries to jettison legacy forces and innovate in new capabilities, including the broader adoption of emerging technologies such as autonomous systems.

A note about non-state actors: their numbers and operations are likely to surge amid the pandemic and economic fallout. Non-state and terrorist groups have used the widespread disruption to retool, retrain, and reorganize, moving into the void left by retreating state capability and a near-singular focus by governments on pandemic and economic security. In the Middle East, for example, Iraq has seen a dramatic increase in terror attacks. During Q1 2019, Iraq experienced just under 300 attacks; in Q1 of 2020, it experienced just over 550.

Right-wing terror is also on the rise globally, with these groups having viewed the pandemic as a growth opportunity. As CSIS’s Seth Jones, Catrina Doxsee, and Nicholas Harrington found in a recent report, right-wing terror has risen rapidly since 2013. In the United States, right-wing terrorists perpetrated 57 percent of terrorist attacks and plots since 1994, more than twice the number perpetrated by left-wing extremists and three times as many as Salafi-jihadists. Moreover, two-thirds of the attacks in 2019 and 90 percent between January 1 and May 8, 2020 were conducted by far-right extremists. The specter of right-wing terror has been accelerated by conspiracy theories and disinformation spread through social media channels. Armed paramilitaries and far-right extremists have mobilized against Black Lives Matter protestors in 42 states and agitated against pandemic lockdown restrictions in over 30 states. In February, the FBI listed right-wing domestic terror alongside ISIS as the greatest threat facing the United States, with 1.4 million online adherents. As conditions worsen in many countries, radical ideologies and groups could further increase their ability to attract followers.

The pandemic has intensified nearly all the underlying factors that make mass protest more likely as laid out in our March report, The Age of Mass Protests. These range from use of social media and digital technologies to unemployment and inequality. The pandemic has also laid bare problems in governance and exacerbated ongoing economic crises in many countries.

Far from quieting the streets, the pandemic has already sparked sustained mass protests in over a dozen countries, including the United States, South Africa, Kenya, Brazil, and France. Protests in the United States related to systemic racism and police brutality may have been the largest ever in the nation’s history. Beyond recent societal upheavals, the pandemic is sowing the seeds for long-term unrest. The dual economic and public health crises have and will further exacerbate inequality, empowering far-left and far-right political movements, while governments are further stressed by economic decline. Similar to the aftermath of the Global Financial Crisis, which set the stage for many of 2019’s mass protests across 119 countries, a continued global political awakening appears inevitable in the years ahead. The only real question is how and if governments and institutions are capable of and willing to adapt to changing popular attitudes and whether these movements can convert people power into political outcomes.

With 2020 marking the fourteenth consecutive year of declining democracy worldwide according to Freedom House, the pandemic risks further authoritarian gains. This problem has become more acute as authoritarian-minded leaders across multiple countries with a range of political systems use the pandemic to justify power grabs and further abrogation of citizen rights. For example, national governments in Lebanon, Iraq, Hong Kong, and Chile have used the public health emergency to ban public protests in an effort to erase gains made in 2019. The government of the Philippines has used “fake news” laws to silence journalists critical of the government response but not to actively diminish public health misinformation.

On the other hand, the pandemic could prove a restorative moment for democracy, most notably by exposing the ineffectiveness of political populism. Populist governments currently represent about a third of global democracies, and virtually all of these governments have been caught flat-footed as they at times disregard medical advice, downplay the severity of the crisis, and are at war with their own administrative states and expert advice. The United States, United Kingdom, Brazil, India, and Mexico—all with populists leading their governments—have suffered more cases and deaths than peer democracies such as Germany and South Korea. These failed populist responses to the pandemic could discredit their political style in the future; for example, polling for populist leaders in the United States, Brazil, and United Kingdom has trended sharply down in recent months. Meanwhile, support for democratic government has actually increased among established Western European democracies as societies coalesce to fight the pandemic together.

At its outset, the pandemic created a notable rebound in trust in countries around the world, disrupting long-term declines in trust in governments and institutions across many countries. Overall, trust in experts and scientists improved as people increasingly relied on information and opinions from medical experts and civil servants attempting to contain the pandemic. Polling tracked a sharp upward trend in trust in scientists, government leaders, and the local community across democratic societies. In a mid-April survey, Edelman found that trust had reached an-all-time-high in the history of their “Trust Barometer,” with 65 percent of people around the world affirming trust in their national government institutions, up 11 points from January 2020, including in the United States where trust rose from 39 to 48 percent.

However, that “rally around the flag” effect quickly faded. Across the G7, public approval of government responses to the pandemic has continually declined, and the portion of those who trust government to manage the pandemic dipped to 50 percent across the G7 between April and June. In the United States, the percentage of those who with little or no confidence in information they receive from the federal government rose from 38 percent in March to 49 percent in May. As rally effects fade, public confidence in political institutions may decrease as well.

Collapsing trust may have significant long-term impacts, including as it relates to informing the lasting beliefs of Generation Z (born between 1995 and 2010). Research on past pandemics indicates that Covid-19 will permanently decrease the confidence of younger generations in political institutions and leaders and their governments’ health care policies. Emerging from the pandemic, governments may suffer not only from fiscal deficits but from deficits of trust. This will carry potentially significant ramifications, as trust is core to democratic governance and vital to societal resilience in times of crisis. It is worth noting that, to date, high-trust societies such as South Korea have been much more successful in combatting the virus than low-trust ones such as the United States, Russia, and Italy.

Those governments, businesses, institutions, and individuals that are most disciplined, rigorous, and honest in their assessment of the challenges now facing our world will emerge strongest from this crisis. The future does not just happen to us. We shape it actively by our actions and inactions, especially during times of massive upheaval, which this moment certainly represents. Rather than resigning to the trends outlined here, we should think how to actively design and mold the kind of world we want—one that avoids a repeat of the type of crisis that is now consuming us.

Sam Brannen leads the Risk and Foresight Group and is a senior fellow in the International Security Program at the Center for Strategic and International Studies in Washington, D.C. Stirling Haig is a former research assistant and Habiba Ahmed is a former intern for the Risk and Foresight Group. Henry Newton is an intern for the Risk and Foresight Group.

This report is produced by the Center for Strategic and International Studies (CSIS), a private, tax-exempt institution focusing on international public policy issues. Its research is nonpartisan and nonproprietary. CSIS does not take specific policy positions. Accordingly, all views, positions, and conclusions expressed in this publication should be understood to be solely those of the author(s).

© 2020 by the Center for Strategic and International Studies. All rights reserved.